올해 초 2020년 3월에 의회는 개인, 기업, 의료 기관, 주 및 지방 정부에 자금을 제공하여 단기 현금 흐름 요구 사항을 충족할 수 있도록 지원하는 코로나바이러스 구호, 구호 및 경제 안보법(CARES)을 통과시켰습니다. CARES 법의 한 조항은 급여 보호 프로그램(Paycheck Protection Program, PPP)으로, 소기업 소유자가 직원을 유지하고 급여 삭감을 완화할 수 있도록 중소기업청이 보증하는 잠재적으로 탕감 가능한 대출로 총 6,490억 달러를 승인했습니다.

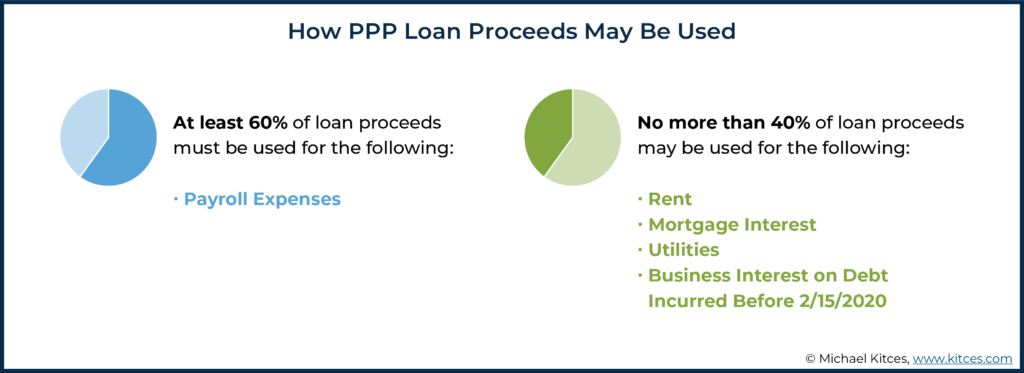

PPP 대출을 탕감받으려면 받은 자금을 미리 정의된 적격 비용으로 사용해야 합니다. 탕감된 PPP 대출 금액의 최소 60%는 급여 비용(사업자에게 적용되는 특정 제한 사항에 따라 급여 및 급여뿐만 아니라 휴가, 가족 및 의료 휴가 포함 , 그룹 건강 보험, 퇴직 수당, 주 및 지방세), 임대료, 모기지 이자, 유틸리티 및 2020년 2월 15일 이전에 발생한 부채에 대한 사업 이자에 대한 나머지 자금(40% 이하)

일부 면제 한도는 사업주 자신의 급여 비용에 적용되며 그룹 건강 보험, 퇴직 수당 및/또는 자신의 고용으로 인해 지불되는 주 및 지방 세금 금액에 영향을 미칠 수 있습니다. 또한, 대출 탕감 금액은 대출의 "해당 기간" 동안 지불했거나 발생한 비용에만 적용됩니다.

대출이 2020년 6월 5일 또는 그 이후에 자금이 조달된 경우 보장 기간은 대출 자금이 조달된 날짜부터 시작하여 24주입니다. 2020년 6월 5일 이전에 자금이 조달된 대출의 경우, 차용인은 24주 또는 8주의 적용 기간을 선택할 수 있는 재량권이 있습니다. 격주로(또는 더 자주) 급여를 실행하는 사업주는 PPP 자금이 수령된 후 시작되는 급여 기간의 첫 번째 날부터 "대체 급여 적용 기간"을 사용할 수 있습니다. PPP 자금을 수령할 때), PPP 대출 면제를 받기 위해 더 많은 급여 지출을 허용할 수 있습니다.

PPP 대출은 사업주가 직원을 유지하고 재정적 어려움이 있을 때 급여 삭감을 완화할 수 있도록 돕기 위한 것이었습니다. 따라서 특정 대출(예:$50,000 이상)에 대해 탕감받을 수 있는 금액은 고용주의 FTE(Full-Time Equivalent) 직원 수가 일정 금액만큼 감소하거나 보수가 높지 않은 직원( 즉, 연봉이 $100,000 미만인 직원)은 25% 이상 삭감됩니다(의회는 직원을 재고용하거나 임금을 회복하기 위해 노력한 차용인에 대한 예외를 통해 약간의 유연성을 제공했지만).

FTE 직원 수의 변경이 적격 PPP 대출 탕감 금액에 영향을 미치는지 여부를 결정하기 위해 고용주는 해당 기간 동안의 평균 주간 FTE를 2019년 2월 15일부터 6월 30일 또는 1월 1일 사이의 기간 동안의 평균 주간 FTE와 비교해야 합니다. – 2020년 2월 29일(고용주는 FTE 수가 적은 기간을 선택할 수 있음), 여기서 FTE 1명은 해당 시간에 기여하는 개인에 관계없이 주당 40시간 근무에 해당합니다(단, 단일 근로자는 주당 40시간 이상 근무하는 경우 주당 1명 이상의 FTE). FTE가 감소하면 PPP 대출 면제도 비례적으로 감소합니다. 예를 들어 FTE가 20% 감소하면 적격 대출 탕감이 20% 감소합니다. 또는 고용주가 더 유리한 결과를 제공하는 경우 '안전한 항구' FTE 계산을 사용할 수 있습니다. 세이프 하버 방식은 주당 40시간 이상 근무하는 직원을 1명의 FTE로, 주당 40시간 미만 근무하는 직원을 0.5명의 FTE로 계산합니다. 한편, (이전) 급여가 $100,000 미만인 근로자의 보상을 25% 이상 삭감하면 PPP 대출의 탕감 금액이 25%를 초과하는 범위에서 1달러로 감소합니다. 임계값).

궁극적으로 핵심은 PPP 대출이 있는 소상공인 고객이 탕감 받을 수 있는 금액을 최대화할 수 있도록 어드바이저가 다양한 고려 사항을 가지고 있다는 것입니다. 특히, 차용인이 자격이 될 수 있는 특정 적용 기간을 선택하는 것은 용서를 위해 고려할 비용 구성에 상당한 영향을 미칠 수 있습니다. FTE 계산 방법, FTE 감소 발생 여부를 결정하는 데 사용된 FTE 비교 기간, (높은 보상을 받지 않은) 직원 임금의 변경도 적격 용서 금액 감소 여부에 영향을 미칠 수 있습니다. 그리고 고문은 하는 고객을 준비해야 합니다. 탕감된 금액과 관련된 잠재적 납세 의무를 검토하여 PPP 대출을 탕감받을 수 있습니다!

Jeffrey Levine, CPA/PFS, CFP, AIF, CWS, MSA는 재무 계획 전문가를 위한 최고의 온라인 리소스인 Kitces.com의 Lead Financial Planning Nerd이며 Buckingham Wealth Partners의 최고 계획 책임자이기도 합니다. 2020년에 Jeffrey는 불확실한 시기에 의지해야 할 상위 25명의 목소리 중 하나로 Investment Advisor Magazine의 IA25에 선정되었습니다. 또한 2020년에 Jeffrey는 Financial Advisor Magazine에서 주목해야 할 젊은 고문으로 선정되었습니다. Jeffrey는 AICPA 재무 계획 부서에서 "개인 재무 계획 서비스의 모범적인 전문적 성취"에 대해 수여하는 기립 박수를 받았습니다. 그는 또한 "성취, 금융 자문 산업에 대한 기여, 리더십 및 미래에 대한 약속"을 인정하는 InvestmentNews의 2017년 40세 미만 40세 클래스에 선정되었습니다. Jeffrey는 Savvy IRA Planning®의 생성자 및 프로그램 리더이자 Horsesmouth, LLC를 통해 제공되는 Savvy Tax Planning®의 공동 생성자 및 공동 프로그램 리더입니다. 그는 Forbes.com과 수많은 업계 간행물에 정기적으로 기고하고 있으며 일반적으로 그의 통찰력으로 언론인들의 사랑을 받고 있습니다. Twitter @CPAPlanner에서 Jeff를 팔로우할 수 있습니다.

여기에서 Jeff의 기사를 더 읽어보세요.

2020년 1월 22일 질병통제예방센터(CDC)는 미국에서 실험실에서 확인된 COVID-19의 첫 번째 사례에 대한 알림을 받았습니다. 그 후 며칠, 몇 주, 몇 달 동안 바이러스는 미국 전역에 계속 퍼졌고, 현재까지 거의 25만 명의 미국인이 목숨을 잃는 건강 위기를 초래했습니다.

불행히도 이것은 미국 역사상 최악의 전염병 중 하나가 미국인에게 어떤 영향을 미쳤는지에 대한 이야기를 시작했을 뿐입니다. 코로나19 팬데믹(세계적 대유행)은 비극적인 인명 피해와 함께 미국 경제에도 큰 타격을 입혔다. 계절 조정 실업률은 2020년 4월에만 2천만 명 이상의 미국인이 실업 수당을 신청하면서 거의 하룻밤 사이에 4% 미만에서 거의 15%로 증가했습니다.

그 2000만이라는 숫자가 믿기지 않지만, 더 나쁠 수도 있습니다. 특히 2020년 3월 27일 트럼프 대통령은 2020년 코로나바이러스 원조, 구호 및 경제 안보(CARES) 법안에 서명했습니다. CARES 법은 2조 달러 이상의 구호 패키지였으며 급여 보호 프로그램(PPP)을 위한 3,490억 달러(이는 결국 급여 보호 프로그램 및 건강 관리 강화법에 의해 총 6,590억 달러로 증액됨) 할당을 포함했습니다. 중소기업청에서 전액 보증하는 어려운 중소기업을 위한 새로운 유형의 대출입니다.

이 PPP 대출은 많은 소기업 소유자가 COVID-19 전염병의 시작에서 살아남을 뿐만 아니라 직원의 일자리를 보존하는 데 도움이 되었습니다. 대출은 최소 인수, 이자율 1%, 만기 2~5년(2020년 6월 5일 이후에 자금을 조달한 대출은 만기가 5년이고 2020년 6월 5일 이전에 자금이 조달된 대출)으로 이루어졌습니다. , 대출자와 대출자가 연장에 대해 상호 합의하지 않는 한 만기는 2년입니다.

그러나 대출 조건이 매력적이기는 했지만 가장 중요한 것은 사업주에게 대출을 받도록 충분히 유인할 수 있는 큰 이점이었습니다. 우선 – 의심할 여지 없이 대출의 일부(또는 잠재적으로 전체)를 탕감할 수 있는 능력이었습니다. , 대신 대출을 '무료' 자금으로 효과적으로 전환할 수 있습니다.

그러나 PPP 대출의 면제는 자동으로 이루어지지 않습니다. 대신, 많은 경우에, 대출을 받은 지 몇 달이 지난 후에도 사업주가 지금 내리는 선택과 결정이 대출을 얼마나 탕감받을 수 있는지에 중요한 역할을 할 수 있습니다. 따라서 고문은 PPP 대출 탕감 규정을 이해하고 있어야 소상공인이 절차를 진행하는 데 도움이 될 수 있습니다.

PPP는 엄청난 속도로 소상공인의 손에 돈을 넘기기 위한 전례 없는 노력이었습니다. 이는 전국에 엄청나게 많은 소기업이 존재하는 것을 감안할 때 결코 작은 일이 아닙니다. 그렇게 하기 위해 PPP는 은행, 신용 조합 및 기타 승인된 대출 기관에 의존하여 대출을 승인하고 처리하며, 이는 SBA의 전폭적인 지원을 받습니다. 사업 차용자). 이를 위해 4월 초부터 2020년 8월 8일에 프로그램이 종료될 때까지(최소한 새로운 PPP 대출을 발행하기 위한 목적으로) 약 5,460개의 다른 대출 기관이 무려 5,212,128건의 대출을 지원했습니다!

놀랍게도 CARES 법의 첫 번째 PPP 자금 지원(3,490억 달러)은 SBA가 법으로 서명된 지 3주가 채 되지 않은 2020년 4월 16일에 PPP 신청 수락을 중단하면서 단 몇 주 만에 사라졌습니다. 프로그램에 3,100억 달러를 추가한 두 번째 기금은 급여 보호 프로그램 및 건강 관리 강화법의 일환으로 2020년 4월 24일에 제공되었습니다.

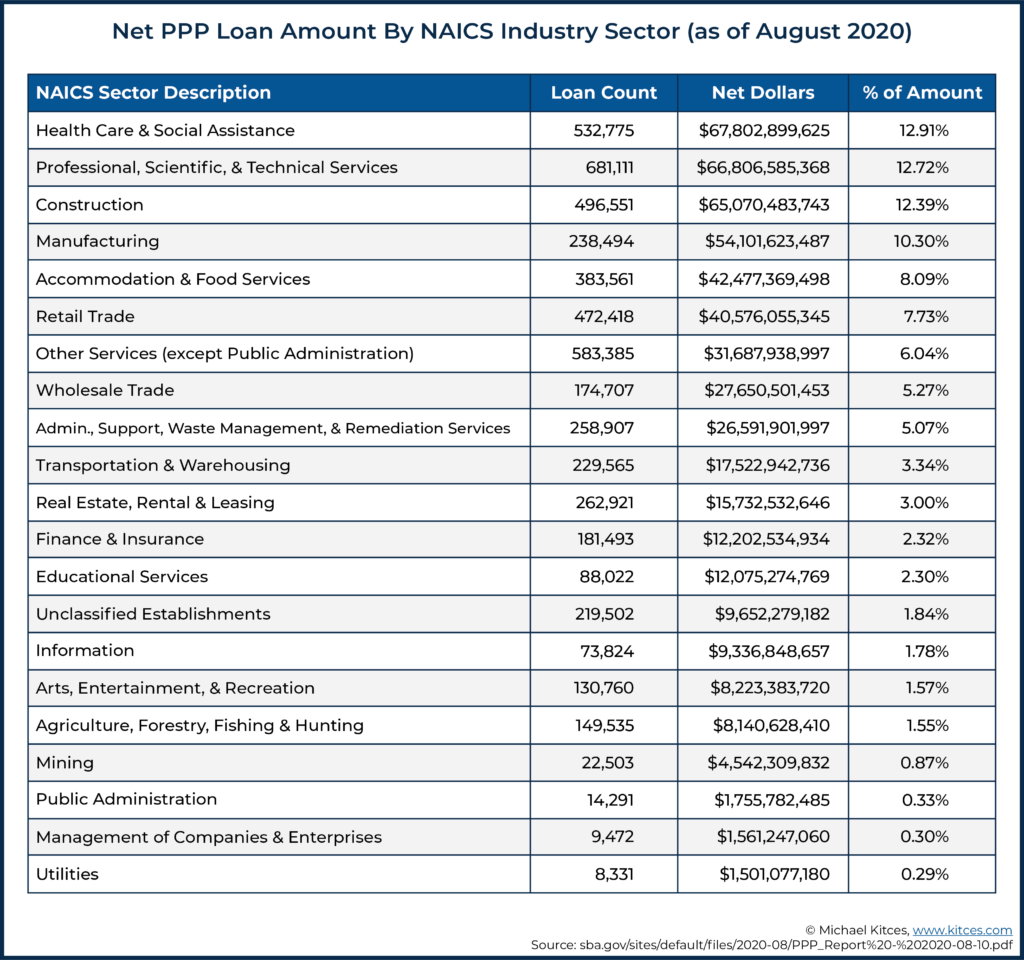

결국 추가 자금이 충분하다는 것이 판명되었습니다. 2020년 8월 8일 프로그램이 종료된 날짜를 기준으로 PPP 프로그램을 통해 거의 모든 종류의 비즈니스(아래 차트 참조)에 약 5,250억 달러의 대출이 승인되었습니다(즉, $349 + $310 =프로그램에 할당된 6,590억 달러는 사용되지 않았습니다.

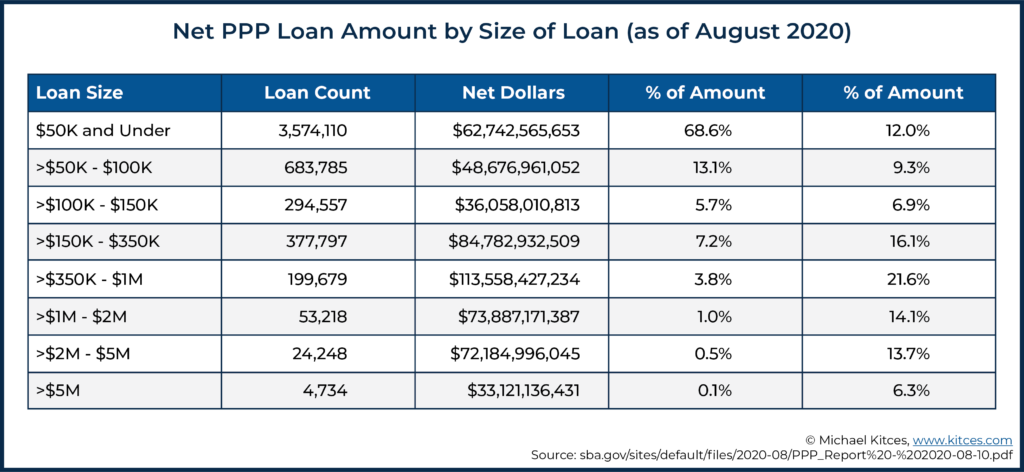

PPP 하에서 발행된 대출의 대다수는 상대적으로 작았습니다. 실제로 아래 차트에서 볼 수 있듯이 발행된 약 520만 건의 대출 중 거의 70%가 5만 달러 이하의 대출이었습니다. 그러나 이러한 대출이 널리 퍼져 있음에도 불구하고 이러한 대출은 발행된 모든 대출의 총 가치의 12%만을 차지했다는 점에 주목할 가치가 있습니다. 대조적으로, $5백만에서 $1천만(PPP에서 사용 가능한 최대 금액) 사이의 대출은 발행된 모든 대출의 0.1%에 불과했지만 전체 PPP 기금의 6.3%를 차지했습니다.

기업이 두 가지 요구 사항을 충족하는 경우 PPP 대출이 기업에 제공되었습니다. 첫째, 일반적으로 직원이 500명 미만인 기업으로 정의되는 "소기업"으로 간주되어야 했습니다(NAICS 코드가 더 높은 직원 규모 기준을 제공하는 산업의 특정 기업이 자격을 얻을 수 있음). 둘째, 해당 기업은 대출 요청이 "필요하다는 선의의 증명서를 제출해야 했습니다. COVID-19로 인한 현재 경제 상황의 불확실성으로 인해."

기업이 이 두 가지 조건을 충족한다면 평균 "적격 월 급여" 비용의 2.5배 또는 1천만 달러 중 작은 금액에 해당하는 PPP 대출을 받을 수 있습니다.

적격한 월 급여 비용에는 직원의 급여와 임금, 개인 사업자 및 파트너의 이익(각각 고려될 수 있는 급여/임금/소득의 최대 연간 금액 $100,000이 적용됨) 및 직원의 그룹 의료 혜택, 퇴직 기여금, 주 및 지방 세금.

사업체의 평균 월 급여를 결정하기 위해 사업체는 일반적으로 2019년의 평균 월간 급여를 사용했습니다. 그러나 계절 사업체는 2019년 2월 15일부터 2019년 6월 30일 사이 또는 임의의 12주 동안의 평균 월간 급여를 사용할 수 있었습니다. 반면 신규 사업(2019년 아직 운영하지 않아 급여 기록이 없는 사업)은 평균을 사용할 수 있었다. 2020년 1월 1일부터 2020년 2월 29일까지의 월간 급여

많은 소기업 소유자에게 급여 보호 프로그램은 직원 수 또는 보상을 더 이상 줄이거 나 어떤 경우에는 사업을 완전히 폐쇄하지 못하도록 막는 생명선이었습니다. 그러나 PPP 대출은 사업주에게 절실히 필요한 유동성을 제공했지만 일부 조건이 붙었습니다.

보다 구체적으로, CARES 법은 PPP 수익금의 사용을 제한하여 수익금의 60% 이상을 급여 비용으로 사용하고 나머지 수익금(40% 이하)을 임대료, 모기지 이자, 2020년 2월 15일 이전에 발생한 부채에 대한 유틸리티 및 기타 사업 이자

앞서 언급했듯이 PPP 대출은 1% 금리와 2년 또는 5년 만기로 발행되었습니다. 어려움을 겪고 있는 기업에게는 상당히 유리한 조건입니다. 젠장, 모든 비즈니스, 꽤 유리한 조건입니다!

그러나 일부 기업은 PPP 대출을 상환(또는 이미 상환)하려고 하는 반면, PPP 대출을 요청한 대다수의 비즈니스 소유자는 대출을 최대한 많이 탕감받을 의도로 그렇게 했습니다.

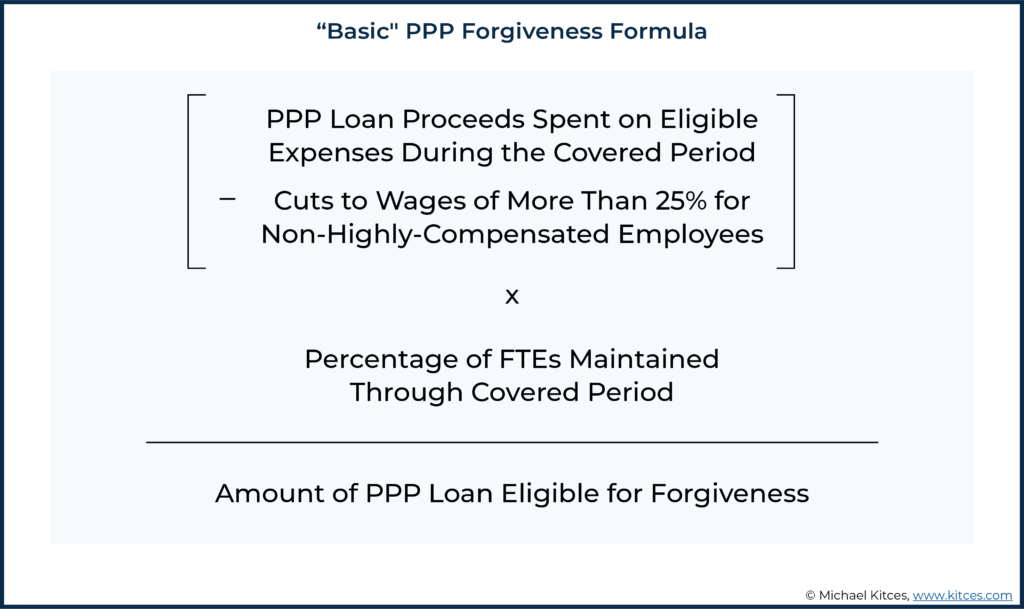

표면적으로는 PPP 대출이 얼마나 탕감될 것인지를 결정하는 공식은 아래 그림과 같이 상당히 간단합니다. 그러나 많은 규칙 및 규정과 마찬가지로 '악마는 세부 사항에 있습니다', 보고할 적용 기간, 청구할 적격 비용, 적용된 임금 감소, 유지되는 FTE의 수.

PPP 대출의 적용 기간은 탕감 계산에 포함될 수 있는 탕감 대상 비용이 "발생"하거나 "납부"된 기간(잠시 후에 자세히 설명)입니다.

2020년 6월 5일 또는 그 이후에 자금이 지원되는 대출의 경우, 적용 기간은 대출 수익금을 받은 후 24주입니다(즉, 대출을 받은 후 24주 동안 적격 비용에 '사용'해야 했습니다/사용해야 했습니다). , 용서받을 수 있는 자격을 갖추기 위해). 대조적으로, 2020년 6월 5일 이전에 자금이 조달된 대출은 원래 적용 기간이 8주에 불과했지만 차용인에게 둘 중 하나를 선택할 수 있는 재량권을 주기 위해 수정되었습니다. 8주 또는 24주.

그러나 다행히도 PPP 대출의 압도적 다수가 2020년 6월 5일 이전에 자금이 조달되었으므로 대다수의 차용인은 8주 또는 더 긴 24주(필요한 경우) 적용 기간을 선택할 수 있는 유연성을 갖습니다.

표준 "적용 기간" 외에도 SBA 및 재무부 규정은 고용주가 "대체 급여 적용 기간"을 사용할 수 있는 옵션도 제공했습니다. 대체 급여 적용 기간은 높은 수준에서 정확히 들리는 것과 같습니다. 다른 만 일부 사업주가 선택할 수 있는 적용 기간 급여 비용에 적용됩니다(기타 비용은 여전히 '정규' 적용 기간이 적용됨).

대체 급여 적용 기간은 다음이 시작되는 첫날에 시작됩니다. 급여 기간, PPP 자금이 조달된 후(차용자가 PPP 자금 지원을 받은 시점 대신), 8주 또는 24주 동안 실행 마침표).

하지만 모두 기업은 이 추가 보장 기간을 활용할 수 있습니다. 오히려 그렇게 하기 위해 기업은 격주로(또는 더 자주) 급여를 실행해야 합니다.

대체 급여 적용 기간(해당되는 경우)을 사용할 때의 주요 이점은 더 많은 급여 비용을 용서받을 수 있다는 것입니다. 많은 기업이 실제로 대체 적용 급여 기간을 사용하여 급여 기간이 끝난 후 일정 시점에 직원에게 급여를 지급하면 해당 기업이 대체 적용 급여 기간에 포함된 이전 급여 일정의 비용 총액을 얻을 수 있습니다.

대체 적용 급여 기간을 사용하면 두 개의 개별 적용 기간을 추적해야 하는 복잡성이 추가됩니다(만 급여 비용은 대체 적용 급여 기간에 적용됩니다. 다른 모든 비용에 사용되는 PPP 자금은 표준 적용 기간으로 추적해야 합니다. 그러나 일부 기업의 경우 면제 계산에 포함될 수 있는 추가 유연성 및 추가 급여 비용은 그만한 가치가 있는 복잡성을 추가했습니다.

그러나 '정규' 적용 기간 동안 급여 비용을 충분히 지출하여 최대의 잠재적 용서를 받는 다른 기업의 경우 대체 적용 급여 기간을 선택하면 불필요한 복잡성이 추가되므로 사용해서는 안 됩니다.

대체 적용 급여 기간은 24주 적용 기간이 사용되는 시나리오에서 사용되지 않을 것입니다. 그러한 보장 기간은 그 자체로 대부분의 기업이 최대 탕감을 얻기 위해 급여 비용에 대해 충분히 많은 비용을 지출할 수 있도록 해야 합니다(그러나 고용주는 아래에서 자세히 설명하는 탕감 감소를 피하기 위해 더 오랜 기간 동안 직원 수와 급여를 유지해야 합니다. ).

CARES 법 섹션 1106(b)는 탕감받을 수 있는 PPP 대출 금액을 결정할 때 고려되는 사업 비용을 설명합니다. 구체적으로 1106(b)항은 다음과 같이 명시합니다.

특히, SBA와 재무부가 제공한 후속 지침에서 PPP 대출 수익금이 일반적으로 사용될 수 있는 방법에 대해 채택된 규정과 유사한 탕감 계산 규정이 채택되었습니다. 따라서 탕감된 PPP 대출 금액의 최소 60%는 급여 비용으로 지출되어야 합니다. , 임대료, 모기지 이자 또는 공과금에 지출된 탕감 금액을 40%로 제한합니다.

물론 수익금의 100%를 급여 비용으로 사용하는 기업의 경우 이것은 논점이지만 적용 기간 동안 급여 비용만으로 수익금을 완전히 사용할 수 없는 차용인의 경우에는 다음과 같은 경우가 더 많습니다. 대출 금액이 2.5개월 또는 대략 10주의 급여 비용을 기준으로 했기 때문에 8주 적용 기간이 사용되었습니다. PPP 대출 수익금의 최소 요건은 반드시 급여 비용 지출이 중요해집니다.

위의 예에서 비급여 비용의 $80,000은 $80,000 ÷ $200,000 =발행된 총 PPP 대출의 40%를 나타냅니다. 그리고 앞서 언급했듯이 40%는 급여 외 비용(탕감 여부에 관계없이)에 사용할 수 있는 PPP 대출 금액의 최대 금액입니다. 따라서 나머지 $200,000 – $80,000(급여가 이미 지출됨) – $80,000(비급여) =$40,000 PPP 자금은 추가 급여 비용에 사용해야 합니다(이 경우 $80,000 + $40,000 =$120,000이 되기 때문에). 급여에 지출해야 하는 총 PPP 자금의 60% 필요) .

PPP 대출의 탕감 금액을 결정할 때 의회가 사용하기로 선택한 다소 특이한 언어에 주목하는 것도 중요합니다. "발생한 다음 비용의 합계 및 결제 완료." 특히 "발생 또는 지불" 회계 방법이 없습니다. 일반적으로 비용은 달러가 실제로 사용된 시점을 보는 현금주의 회계 방법이나 비용을 발생시킨 행동이 실제로 발생한 시점을 보는 발생주의 회계 방법을 사용하여 계산됩니다. 따라서 처음에는 규칙이 무엇인지 명확하지 않았습니다! 사업주가 둘 중 하나를 선택할 수 있었습니까?

결국, SBA와 재무부는 본질적으로 둘 다 허용하는 슈퍼 비즈니스 소유자 친화적인 구조를 채택했습니다. 사용되는 회계 방법... 동시에! 달리 말하면 적격 비용을 지불하는 데 사용된 PPP 자금은 둘 중 하나인 한 탕감받을 수 있습니다. 적용 기간 동안 실제로 지불된 또는 해당 기간 동안 발생했습니다!

비즈니스 소유자가 이 (믿을 수 없을 정도로 유리한) 비용 처리를 활용하기 위해 인식해야 하는 작지만 중요한 문제가 하나 있습니다. 발생 비용을 위해 적용 기간 동안 용서 공식에 포함되기 위해서는 반드시 다음 예정된 지불 날짜/청구 날짜 또는 그 이전에 지불되어야 합니다. 해당 기간 동안 비용이 지불되지 않거나 비용이 발생했지만 그 이후 첫 번째 정기 청구일까지 지불되지 않은 경우 비용이 아닙니다. 유료 또는 발생한 비용.

급여 보호 프로그램은 주로 근로자의 고용을 유지하는 데 도움이 되는 방법으로 설계되었습니다. 이에 따라 의회에서 할당한 PPP 자금의 상당 부분이 직접 엠> 근로자를 "급여"로 간주합니다.

그러나 "급여"라는 단어가 "임금" 또는 "급여"라는 개념을 불러일으키는 반면, PPP 대출의 경우 "급여 비용"이라는 용어는 확실히 더 광범위합니다. 예를 들어, 자영업으로 인한 순이익을 포함하는 것 외에도(자신을 비즈니스 소유자로서!) 급여, 커미션, 급여 및 기타 현금 보상(직원당 연간 $100,000 한도)과 함께 급여 비용에는 일반적으로 다음이 포함됩니다.

However, while these expenses can generally be included in the amount of a PPP loan eligible for forgiveness, and self-employed individuals can even include some of their own earnings from the business as payroll (even if not actually received as a W-2 salary, in the case of partnerships or sole proprietorships), the SBA and Treasury rules limit the ability to include some of these other ‘employee benefits’ payroll-related expenditures if they are made on behalf of business owners themselves (who work at/for the company).

More specifically, the following expenses are not considered Payroll Costs:

As noted earlier, the primary purpose of the Paycheck Protection Program was to safeguard the employment status of small business workers. Accordingly, some businesses that received PPP loans, but that failed to adequately protect worker’s compensation, may be ‘punished’ via a reduction in the amount of their PPP loan that is eligible to be forgiven.

Or at least some of them are…

As while the Paycheck Protection Program did originally include requirements for businesses to maintain certain employee headcount requirements to be eligible for forgiveness on their PPP loans, on October 8, 2020, the SBA and Treasury announced that borrowers who received loans of $50,000 or less would not be subject to such reductions in forgiveness. Which, notably, ‘covers’ more than two-thirds of PPP borrowers (but only about 10% of loan dollars). However, borrowers who took larger loans must still deal with a variety of rules that can result in a reduction of the forgivable amount of their loan.

More specifically, reductions in the forgiveness of PPP loan proceeds spent on eligible expenses during the Covered Period are generally applied for both reductions in the number of Full-Time Equivalent (FTE) employees (the number of cumulative 40-hour workweeks a business’ employees perform) during the Covered Period (as compared to a reference period) and reductions in (non-highly-compensated) workers’ compensation in excess of 25% (to prevent businesses from claiming they maintained headcount but then drastically cutting compensation for all the employees they kept on payroll). In other words, businesses had to maintain at least the same number of full-time equivalent employees at the start and end of the Covered Period, and those (non-highly-compensated) employees had to maintain at least 75% of their compensation (i.e., a not-more-than-25% reduction in compensation) to remain fully eligible for PPP forgiveness.

There are, however, a variety of exceptions to the required thresholds of which business owners should be made aware.

Some businesses that received PPP loans were able to maintain their employee headcounts and hours throughout their Covered Periods. In such instances, the reward that those businesses receive is the ability to completely ignore this part of the forgiveness process!

Of course, not all businesses – even with a boost from the Paycheck Protection Program – were able to maintain employee headcount. The penalty for not doing so is a reduction in the amount of the business’ PPP loan that would otherwise be forgiven (with some exceptions, discussed later).

More specifically, a business must compare its average weekly Full-Time Equivalent (FTE) Employees during the Covered Period (or, if elected, the Alternative Payroll Covered Period) to its FTEs during either the period from January 1, 2020 – February 29, 2020, or during the period from February 15, 2019 – June 30, 2019. Notably, businesses can pick the more favorable of these periods (the period in which there were fewer FTEs) for the comparison.

In general, to compare the number of average weekly FTEs during the Covered Period and the comparison period, it is necessary to determine the average weekly FTEs during both periods. A standard FTE is equivalent to one 40-hour workweek, regardless of the number of individuals it takes to get to the 40-hour mark. Thus, a single worker who works 40 hours in a single week is equivalent to one FTE for that week. Similarly, if two workers each work 20 hours in a week, they would also constitute, together, a single FTE, as would 8 workers each working 5 hours per week, and so on.

One caveat to this rule, however, is that a single worker cannot comprise more than 1 FTE per week, even if that individual works for more than 40 hours during the week. Thus, while two workers who each work 30 hours per week will constitute (30 x 2) ÷ 40 =1.5 FTEs, a single individual working 60 hours in a week will be equal to just 1 FTE!

Once the numbers of average weekly FTEs during the Covered Period and the comparison period are known, the two amounts must be compared. And, in general, any decrease in the number of average weekly FTEs from the comparison period to the Covered Period will result in a reduction of the forgivable amount of the PPP loan.

For borrowers that do fail to maintain their FTE headcount, the adjustment to their PPP forgiveness is relatively straightforward:the otherwise forgivable amount of the PPP loan will be reduced by the same percentage as the percentage drop in FTEs from the comparison period to the Covered Period. So, for instance, a 20% drop in average weekly FTEs from the comparison period to the Covered Period will typically result in a 20% decrease in the amount of the PPP loan a business received that would otherwise be forgiven.

Incredibly enough, there is yet another election that business owners can choose to make when calculating whether they maintained employee headcount and/or the amount by which their headcount (and thus their forgivable PPP loan) was/is reduced.

Instead of using actual hours worked to calculate FTEs, the business can opt to use a safe harbor method, where all employees who work 40 hours or more during a week are counted as 1 FTE, while all employees who work less than 40 hours during a week are counted as one-half of an FTE.

Perhaps not surprisingly, this is an all-or-nothing decision. A business can’t, for instance, use the safe harbor in some weeks, but not others. Or for some employees, but not others. It’s either used for all the employees for every week of the Covered Period or for none of the employees in any week of the Covered Period.

Using the safe harbor method to calculate FTEs will usually alter the number of FTEs for comparison purposes.

It’s important to note, though, that while using the safe harbor method of calculating FTEs would have resulted in a negative outcome in the example above, its use can actually result in either a positive or a negative effect on forgiveness, depending on the specific set of facts and circumstances.

Although Congress was intent on making sure that PPP loan proceeds were used to keep workers employed through at least the end of the Covered Period, it recognized that there would be some situations where doing so would not be possible, for reasons largely (if not entirely) outside of an employer’s control. In particular, some business owners with lower-wage employees raised concerns that the enhanced unemployment benefits made available as a part of the CARES Act were actually resulting in employees not wanting to return to work until the increased unemployment benefits ended (potentially rendering the employer unable to meet the ‘maintain headcount’ requirement for its own PPP forgiveness).

Accordingly, Congress, the SBA, and Treasury, collectively crafted a series of exceptions to the general rule for reductions in forgiveness. Thus, a business will not have its forgiveness amount decreased for any of the following situations occurring during the Covered Period or Alternative Covered Period:

A careful reading of the above exceptions reveals that they are not blanket exemptions for an employer that covers every 직원. Rather, they are acceptable ‘excuses’ to ignore a drop in FTE count specific to an individual employee.

By contrast, there are two additional exceptions to a drop in FTEs that can be used broadly, across a business, for all employees. They are when either:

For certain businesses, these two exceptions to the ‘normal’ FTE reduction rules can be huge. They are effectively ‘get-out-of-jail-free cards’ that will eliminate any and all FTE reductions that would otherwise apply (though PPP funds will still need to be spent on eligible expenses during the Covered Period to be eligible for forgiveness).

For businesses that are unable to return to the same level of business activity as before February 15, 2020, due to compliance requirements, it’s as simple as documenting the public health requirement and the corresponding drop in business activity (read “gross revenue”).

Meanwhile, for businesses that reduced employee headcount or hours at some point between February 15, 2020, and April 26, 2020, it just needs to reverse those decisions by the end of the year. Thus, now may be a critical time for such businesses to consider bringing back employees, as the difference between rehiring staff on December 15, 2020, for example, and January 15, 2021, could be the difference in thousands (or even tens or hundreds of thousands) of additional forgiveness!

If not for an additional restriction, shrewd business owners may have looked to avoid drops in headcount by simply cutting employees’ compensation but keeping them employed. However, while certain cuts in compensation are allowed, the CARES Act does limit such actions.

More specifically, to the extent that an employee with annualized salary/wages of less than $100,000 during 2019 has their compensation slashed by more than 25%, the excess (beyond 25%) will result in a dollar-for-dollar drop in the amount of the business’ PPP loan that is forgivable (unlike the reduction due to employee headcount, which is calculated on a percentage basis). This dollar-for-dollar reduction in the PPP forgivable amount due to a reduction in employee compensation is made by comparing the drop in wages/salary during the Covered Period to the average salary/wages paid to the employee from January 1, 2020 – March 31, 2020.

However, cuts in compensation of less than 25% to the same employees have no impact on forgiveness. Similarly, cuts to compensation of those earning $100,000 or more in 2019 have no impact.

Two final points are worth mentioning here. First, similar to the ‘exception’ that allows an employer to rehire a terminated individual by December 31, 2020, to avoid a reduction in forgiveness due to a drop in headcount, so too can an employer avoid a reduction in loan forgiveness for cutting a non-highly-compensated employee’s compensation in excess of 25% if the salary is restored by the same December 31, 2020 deadline.

However, per the instructions for forgiveness published by the SBA and Treasury, this exception only appears to be available if the decision to slash wages/salary was made between February 15, 2020, and April 26, 2020. (Whereas subsequent reductions in compensation or headcount that were implemented after April 26 th can’t be ignored, even if the employees are subsequently re-hired or restored to their prior compensation level.)

Second, a business that both reduced its FTEs and cut non-highly compensated employees’ wages by more than 25% will have two reductions in the amount of its PPP loan that would otherwise be forgivable.

There is, however, an “order of operations” that must be followed. More specifically, the dollar-for-dollar reduction for salary cuts (to non-highly-compensated employees) is applied first, followed by applying the percentage reduction in forgiveness due to a drop in FTEs to the already reduced amount.

As is plainly evident, the rules for determining the amount of a business’ PPP loan that can be forgiven by the SBA are complicated (one might even say “obnoxiously” complicated!). That complexity will inevitably lead to some business owners failing to get the maximum possible amount of their PPP loan forgiven or lead to other planning complications.

Advisors can, and should, help clients avoid this fate by taking steps that include the following:

Where the borrower maintains their employee headcount and wages through the ‘regular’ 8-week Covered Period (or qualifies for an exception to forgiveness reductions) and expends enough on payroll (and, if necessary, on other expenses) to have the full PPP loan forgiven (which is pretty likely, if full employment was maintained), the 8-week Covered Period is the logical option.

If this isn’t enough to get full forgiveness, but the business is otherwise relatively close to the required expenditures to obtain full PPP forgiveness, the next step is to see if the Alternative Payroll Covered Period is enough to do the trick.

If the Alternative Covered Period allows the business to spend enough on eligible expenses to get maximum forgiveness, then using it is a ‘simple’ solution.

If it doesn’t, it’s necessary to explore the 24-week Covered Period option instead. If the borrower maintains headcount and wages through the ‘extended’ 24-week Covered Period (or qualifies for an exception to forgiveness reductions), then this becomes the logical option.

However, if FTEs are not maintained and/or there are significant (<25%) cuts to the wages of employees with annualized compensation of less than $100,000, further analysis is warranted.

At the heart of the matter lie two questions…

If the answer to question 1 is “yes” and the answer to question 2 is “no”, then extending to the 24-week Covered Period likely makes the most sense. Otherwise, keeping the ‘original’ 8-week Covered Period will probably be more beneficial for the borrower.

Unfortunately, there is no easy way to figure this out. Someone must ‘run the numbers’ using each method and see what the best result is!

More specifically, while Section 1106(i) of the CARES Act stipulates that “any amount which (but for this subsection) would be includible in gross income of the eligible recipient by reason of forgiveness described in subsection (b) shall be excluded from gross income,” the IRS has effectively negated this position by disallowing any expenses paid with forgiven funds from being deductible by a business on its return.

Without such deductions, the profit of some businesses may be ‘artificially’ inflated, leading to higher-than-normal tax bills for business owners.

The last thing anyone wants is an unexpectedly large tax bill. But given the pandemic and the struggles many business owners are already dealing with, that may never be truer than today. Advisors, therefore, must help such clients plan ahead and avoid surprises.

<시간 />The CARES Act provided a massive stimulus to the American economy in response to the worst pandemic in more than 100 years that gripped the nation. Included in the stimulus was the creation of the much-hyped Paycheck Protection Program, which ultimately provided more than half a trillion dollars in loans to business owners in an effort to help them maintain their employee headcount and payroll.

But while the PPP loans, themselves, have been valuable for business owners, the real cherry on top has been the ability to have some, if not all, of the loan forgiven by the SBA. To benefit from this, though, business owners need to navigate a complex web of rules, from understanding various Covered Periods to knowing what expenses count towards forgiveness – a particularly cumbersome issue for business owners themselves – to dealing with reductions that can apply when employee headcount and/or wages are not maintained throughout the Covered Period.

The good news for advisors is that this complexity provides ample opportunity to educate clients and to provide invaluable guidance in a time of great need. Doing so not only helps business owners to maximize the amount of PPP forgiveness they receive, but can also create the kind of goodwill that can lead to clients for life!