LIC는 2018년 9월에 새로운 연금 계획을 시작했습니다. LIC Jeevan Shanti .

LIC Jeevan Shanti는 즉시 연금으로 제공됩니다. 및 이연 연금 변형 .

주의할 점은 LIC가 이미 즉시 연금 분야에서 매우 인기 있는 상품을 보유하고 있다는 것입니다(LIC Jeevan Akshay VI). LIC Jeevan Shanti는 LIC Jeevan Akshay와 매우 유사합니다. 유일한 주요 차이점은 LIC Jeevan Shanti에도 이연 연금 변형이 있다는 것입니다.

LIC Jeevan Shanti 플랜에 대해 자세히 알아보겠습니다.

계속 진행하기 전에 즉시 연금 플랜과 연기 연금 플랜의 차이점을 살펴보겠습니다.

즉각적인 연금 계획 중 , 일시금을 1회 지급하면 보험사에서 평생 연금을 지급합니다. 연금 지급은 구매 즉시 시작됩니다. 얼마나 오래 사는지는 중요하지 않습니다. 보험 회사에서 평생 연금을 지급합니다.

그 뿐만 아니라 보험 회사는 (향후 이자율이 어떻게 변동하는지에 관계없이) 귀하에게 평생 약정 이자율을 지불합니다. 따라서 보험사는 장수위험 뿐만 아니라 이자율위험도 함께 부담하게 됩니다.

연금 계획은 장수 위험을 커버하는 좋은 방법입니다. 연금 플랜을 구매하면 평생 수입원을 보장받을 수 있습니다.

LIC Jeevan Akshay VI는 즉각적인 연금 플랜입니다.

연기된 연금 계획에 따라 , 보험 회사에 지불합니다(단일 보험료 또는 일반 보험료의 형태로). 돈은 계획의 투자 위임에 따라 투자됩니다. 연기(연기) 기간이 끝나면 누적된 말뭉치가 즉시 연금 계획을 구매하는 데 사용됩니다.

따라서 연금은 유예 기간이 끝날 때 시작됩니다. . 정기 소득의 양은 투자 수익, 연령, 연기 기간, 연금 변형 및 일반적인 연금 비율에 따라 달라집니다.

LIC Jeevan Shanti는 이연 연금 플랜의 변형입니다. 단일 프리미엄 플랜입니다. 즉, 프리미엄을 한 번만 지불하면 됩니다. 최대 20년까지 연금을 연기할 수 있습니다. 투자 수익이 보장되며 연기 기간이 끝날 때 연금 이자율도 보장됩니다. 따라서 불확실성이 수반되지 않습니다. 연기 기간이 끝난 후 매년 어떻게 받게 될지 미리 알고 있습니다.

그런데 LIC Jeevan Shanti는 즉시 연금 변형도 제공됩니다. 즉시 연금 계획은 연기 기간이 없는 이연 연금 계획으로 생각할 수 있습니다.

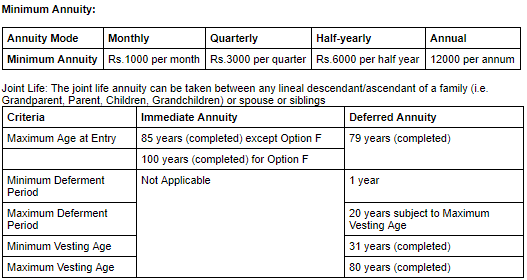

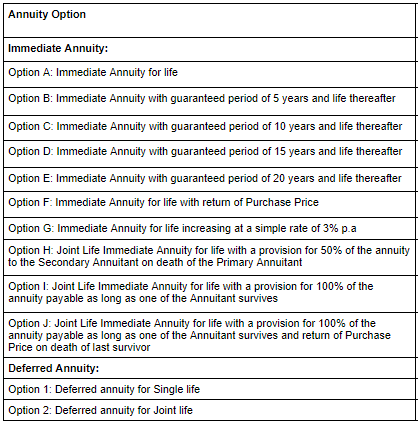

LIC Jeevan Shanti는 9가지 연금 유형으로 제공됩니다(즉시 연금 7가지, 후연 연금 2가지) .

읽기 :은퇴 계획:엄청난 연금 구매는 수입을 늘리고 위험을 줄일 수 있습니다.

LIC 웹사이트를 방문할 수도 있습니다. 자세한 내용은.

읽기 :HDFC 라이프 산차이 플러스:리뷰

LIC Jeevan Shanti는 9가지 유형의 연금으로 제공됩니다(즉시 연금 7가지, 이연 연금 2가지).

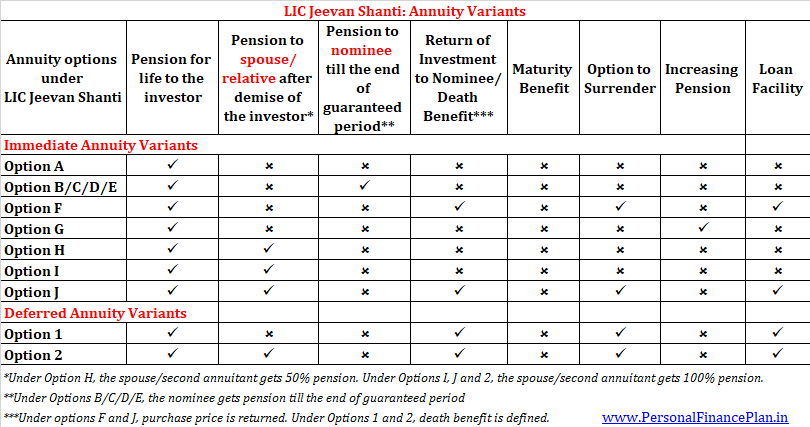

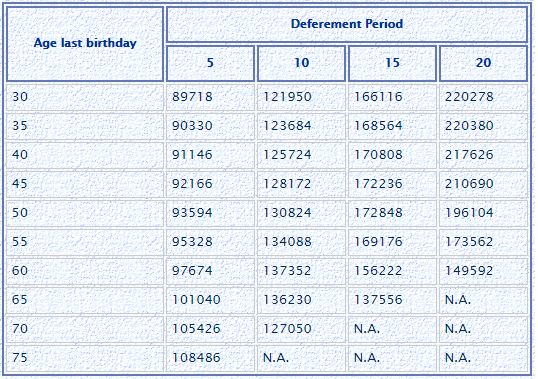

다음은 LIC Jeevan Shanti의 다양한 변형이 제공하는 것을 보여주는 스냅샷입니다.

즉시 연금 유형의 경우 이자율(연금 요율)은 연령 및 연금 유형에 따라 다릅니다. 공동 생활 계획의 경우(배우자 또는 다른 가족 구성원이 있는 경우), 연금 비율도 두 번째 연금 수급자의 나이에 따라 달라집니다.

연금 요율은 투자자의 연령에 따라 증가합니다. 보험 회사는 책임이 낮을 때 더 높은 요율을 지불합니다. 40세의 사람은 70세와 비교하여 더 많은 년 동안 연금을 받을 가능성이 있습니다. 따라서 40세의 경우 연금 요율이 낮아지고 70세의 경우 더 높아집니다.

이연 연금 변형의 경우 연금 비율은 위의 모든 요소에 따라 달라집니다. 또한, 연금 비율은 유예 기간의 양과 두 번째 연금 수급자의 연령(공동 생명 보험의 경우)에 따라 달라집니다.

연기 기간이 늘어남에 따라 연금 요율이 증가합니다.

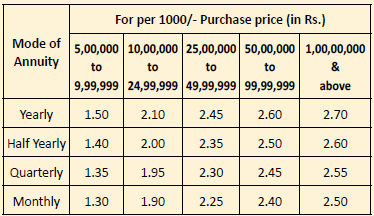

다음은 LIC Jeevan Shanti의 즉시 연금 변형에 대해 LIC 웹사이트에서 사용할 수 있는 샘플 세트입니다. 가격은 Rs 10 lacs의 구매 가격입니다.

이연 연금의 샘플 연금 요율(구매 가격은 Rs 10 lacs). 요금은 독신 생활에 대한 것입니다(공동 생활 계획이 아님).

연금 변형에 대해 자세히 살펴보겠습니다. LIC Jeevan Akshay와 LIC Jeevan Shanti의 즉시 연금 변형 사이에는 연금 요율을 제외하고는 구별할 것이 없습니다. LIC Jeevan Akshay에는 이연 연금 변형이 없습니다.

따라서 먼저 LIC Jeevan Shanti의 이연 연금 변형에 대해 설명하겠습니다. 완성을 위해 이 게시물의 끝에 즉각적인 연금 변형에 대한 그림을 제공했습니다.

더 깊이 파고 들기 전에 이연 연금 변형에 대해 이해해야 할 몇 가지 사항이 있습니다.

연기된 연금 변형에서는 끝날 때까지 아무 것도 얻지 못합니다. 연기 마침표. 따라서 유예 기간 동안 연금 수급자의 사망이 발생한 경우 후보자는 적어도 구매 가격보다 약간 더 많은 금액을 받아야 합니다. 말이 됩니까?

따라서 이연 연금 변형에서 LIC는 추가 보장의 개념을 도입했으며 사망 혜택은 구매 가격보다 높습니다(적어도 유예 기간이 끝날 때까지).

추가 보장은 이연 연금 변형에만 적용됩니다.

보장된 추가는 유예 기간 중 또는 유예 기간 종료 후 사망 혜택을 계산하는 데 사용됩니다.

보장된 추가 금액은 각 보험 월 말, 연기 기간 또는 사망 중 더 이른 날짜까지 발생합니다.

월 추가 보장 =구매 가격 * 월별 표 형식의 연금 요율

월별 표 형식의 연금 요율은 선택한 연금 요율과 유예 기간에 따라 달라집니다. 월별 연금 비율 =(연간 연금 비율 * 96%)/12

사망 혜택 =A와 B 중 더 높음, 여기서

A =구매 가격 + 누적 보장 추가 – 날짜까지 이루어진 총 연금 지불

B =구매 가격의 110%(지금은 무시합시다)

따라서 유예 기간 동안 사망한 경우 귀하의 지명자는 구매 가격 + 누적 보장 추가 금액을 받게 됩니다(아직 연금 지불이 이루어지지 않았기 때문에).

사망 보험금이 계산되는 방식은 계획에 많은 복잡성을 가져옵니다(섹션:LIC Jeevan Shanti에 대한 이상한 점 참조). 사망 보험금은 유예 기간 동안 증가하고 연금 지급이 시작되면 감소하기 시작합니다.

지명자는 사망 보험금을 일시금으로 받거나 해당 금액으로 즉시 연금을 구매하거나(연금 요율은 지명자의 연령에 따라 다름) 분할 혜택(5년, 10년 또는 15년). LIC Jeevan Akshay VI에서는 이러한 옵션을 사용할 수 없습니다.

이제 옵션 1로 돌아가기(단일 연금에 대한 연기 기간)

연금 혜택 :유예 기간이 끝날 때까지 연금이 없습니다. 연기 기간이 끝난 후 t 그 투자자는 평생 연금을 받게 됩니다.

사망 혜택 :위에서 언급한 바와 같이(나중에 예를 들어 설명함)

만기 혜택 :해당 없음

항복 혜택 :허용됨

대출 옵션 :가능

그림

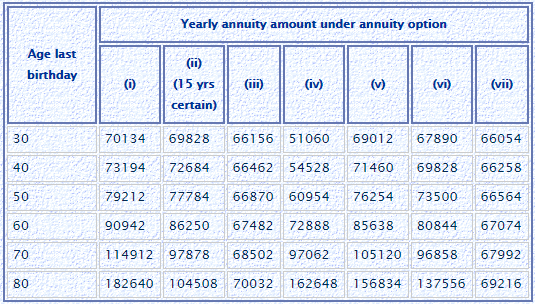

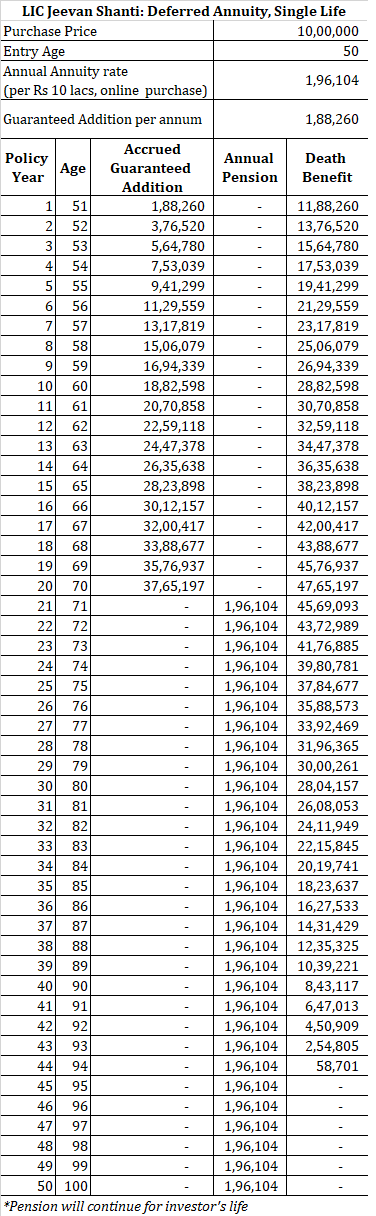

60세의 사람이 옵션 1에 1000만 루피를 투자합니다. 총 지출 금액은 Rs 10.18 lacs(GST 포함)입니다.

60세와 옵션 1(유연 연금, 20년)에 대한 표의 해당 값은 149,592입니다.

처음 20년 동안은 아무 것도 얻지 못할 것입니다. 유예 기간(20년)이 끝나면 평생 동안 연간 Rs 149,592의 연금을 받게 됩니다.

연기 기간이 끝날 때까지 매달 보장된 추가 금액은 (149,592*96%)/12 =Rs 11,967/월 .

따라서 10년 후(유예 기간이 끝나기 전) 사망이 발생하면 후보자는 10락 + 120개월 * 11, 967 =24.36루피를 받게 됩니다.

연금이 유예 기간에서 살아남는 경우 보험은 Rs 28.72 lacs의 보장된 추가를 누적했을 것입니다.

투자자가 85세에 사망하면(예를 들어) 투자자는 5년 동안 연금을 지급받게 됩니다. 사망 시 후보자는 다음을 얻습니다.

루피 10락 + 루피 28.72락(추가 보장 누적) – 5*1.49락(이미 연금 지불) =루피 31.24락. 지명자는 자신의 선택에 따라 일시금, 즉시 연금 또는 할부로 사망 혜택을 받을 수 있습니다.

옵션 1과 옵션 2의 유일한 차이점은 옵션 2에서는 연금이 두 번째 연금도 계속된다는 것입니다. 그리고 사망보험금은 두 수급자가 모두 사망한 후에만 지급됩니다.

두 번째 연금은 배우자, 형제자매 또는 직계존속 또는 직계비속(조부모, 부모, 자녀, 손자녀)

또한 연금 요율에는 두 번째 연금 수급자의 나이도 고려됩니다.

연금 혜택 :유예 기간이 끝날 때까지 연금이 없습니다. 연기 기간이 끝나면 그 그 투자자는 평생 연금을 받을 것입니다. 투자자가 사망한 후 두 번째 연금은 평생 동일한 연금을 받게 됩니다. 두 번째 연금이 투자자보다 먼저 사망한 경우, 연금은 투자자가 사망한 후 중단됩니다.

사망 혜택 :사망보험금은 두 수급자가 모두 사망한 후에 지급됩니다. 사망 보험금 계산은 옵션 1과 동일합니다.

만기 혜택 :해당 없음

항복 혜택 :허용됨

대출 옵션 :가능

그림

60세의 사람이 옵션 2에 1000만 루피를 투자합니다. 총 지출 금액은 Rs 10.18 lacs(GST 포함)입니다.

두 번째 연금의 나이는 50세입니다. 두 번째 연금의 나이도 연금 요율에 영향을 미칩니다.

연금 요율(이연 연금, 20년)은 216,036입니다.

처음 20년 동안은 아무 것도 얻지 못할 것입니다. 유예 기간(20년)이 끝나면 평생 동안 연간 Rs 216,036의 연금을 받게 됩니다.

당신 다음으로 두 번째 연금 수령자(배우자/친척)가 평생 연금을 받게 됩니다. 두 번째 연금이 귀하보다 먼저 사망하면 귀하가 사망한 후 연금이 중단됩니다. 후보자는 연금을 받지 못합니다.

연기 기간이 끝날 때까지 매월 보장된 추가 금액은 (216,036*96%)/12 =Rs 17,282의 비율로 귀하의 정책에 발생합니다.

이 경우 사망 보험금은 두 연금 수급자가 모두 사망한 후 피지명인에게 지급됩니다.

따라서 10년 후(유예 기간이 끝나기 전) 마지막 생존 연금이 있는 경우 후보자는 Rs 10 lacs + 120개월 * 17,282 =Rs 30.73 lacs를 받게 됩니다.

연금 수령자가 유예 기간 동안 살아남는 경우 해당 정책은 Rs 41.47 lacs의 보장된 추가를 누적했을 것입니다.

마지막 생존 연금이 유예 기간 종료 후 5년 후에 사망하면 투자자는 5년 동안 연금을 지급받게 됩니다. 사망 시 후보자는 다음을 얻습니다.

10루피 + 루피 41.47락(추가 보장 누적) – 5*2.16락(이미 연금 지불) =루피 40.67락

지명자는 자신의 선택에 따라 일시금, 즉시 연금 또는 할부로 사망 혜택을 받을 수 있습니다.

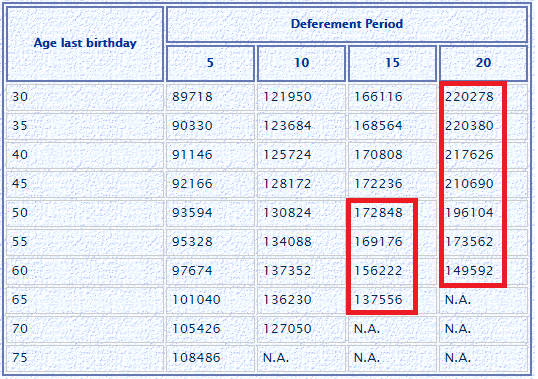

이상적으로는 연금의 경우 연금 비율이 연령에 따라 증가할 것으로 예상할 수 있습니다.

그러나 샘플 표(옵션:1:이연 연금, 독신 생활)를 보면 반드시 그렇지는 않습니다.

몇몇 경우에 연금 요율은 연금 수령자의 연령이 증가함에 따라 낮아졌습니다. 이는 이연 연금 변형의 경우에만 발생합니다(즉각 연금 변형은 아님).

왜?

사망 혜택이 관련되어 있기 때문이라고 생각합니다. 사망 혜택은 동적이며 적어도 유예 기간 동안에는 구매 가격보다 클 것입니다.

사망 혜택 =구매 가격 + 추가 보장 – 연금 지급은 이미 완료되었습니다.

추가 보장은 연금 요율에 따라 달라집니다.

따라서 사망 보험금은 처음에는 시간이 지남에 따라 인상됩니다(유예 기간이 끝날 때까지). 그 이후에는 연금이 지급되면서 내려갑니다.

연금 수령자가 조기 사망할 경우 보험사는 상당한 금액(사망 보험금)을 지급해야 합니다. 분명히 보험 회사는 지불이 곧 이루어지지 않으면 선호할 것입니다.

연금 수령자가 조기 사망할 경우 보험사는 상당한 금액(사망 보험금)을 지급해야 합니다. 분명히 보험 회사는 지불이 곧 이루어지지 않으면 선호할 것입니다.

그리고 노인이 곧 사망할 가능성도 높아집니다. 그러한 경우에 더 낮은 연금 요율은 지출을 줄이는 좋은 방법입니다(아마도 좋은 보험 계약도 마찬가지입니다).

이것이 이연 연금 변형의 연금 요율이 연령에 따라 낮아질 수 있는 이유라고 생각합니다(가입 연령이 특정 임계값을 초과하는 경우).

이제 공동 수명이 있는 이연 연금은 훨씬 더 까다로울 것입니다. 사망급여는 두 번째 연금이 사망한 후에만 지급되기 때문에 두 번째 연금의 연령이 낮아질수록 연금 요율(첫 번째 연금의 연령을 일정하게 유지)이 증가합니다.

너무 많은 요인이 작용합니다.

그런데, 연금 요율은 유예 기간이 증가함에 따라 증가합니다(즉시 연금 및 이연 연금 변형 모두에 대해). 주된 이유는 지불(연기 기간이 더 긴 옵션)이 지연되기 때문입니다. 따라서 화폐의 시간가치는 보험사의 책임을 줄여줍니다. 더 낮은 연기 기간 옵션에서는 연금이 곧 시작될 수 있습니다(따라서 보험사는 그에 따라 연금 가격을 책정해야 함).

이 웹사이트에는 LIC Jeevan Shanti에 대한 좋은 계산기가 있습니다. 내 계산이 계산기와 정확히 일치하지는 않지만 숫자는 작동 방식에 대한 아이디어를 제공하는 데 매우 가깝습니다. 계산기를 가지고 놀아도 연금 수령자의 연령과 유예 기간이 어떻게 조합되어 흥미로운 숫자가 나오는지 확인할 수 있습니다.

LIC Jeevan Shanti 계획에 따른 투자는 섹션 80CCC에 따라 세금 혜택을 받을 수 있습니다. 섹션 80CCC에 따른 혜택은 섹션 80C에 따른 전체 한도인 Rs 1.5 lacs입니다.

연금 소득(연금 소득)은 소득세 슬래브 세율로 과세됩니다.

이 플랜은 LIC 지점으로 가거나 LIC 에이전트의 도움을 받아 구입할 수 있습니다.

LIC Jeevan Shanti 플랜을 온라인으로 구입할 수도 있습니다. LIC 웹사이트로 이동해야 합니다. 위에서 언급했듯이 온라인으로 제품을 구매하거나 NPS 탈퇴 시점에 구매하면 더 나은 연금을 받을 수 있습니다.

답하기 쉬운 질문이 아닙니다. 먼저 장점을 살펴보겠습니다.

단점도 꽤 있습니다.

이 게시물에서 이러한 측면에 대해 더 자세히 논의했습니다.

읽기 :연금 플랜은 언제 구매해야 하나요?

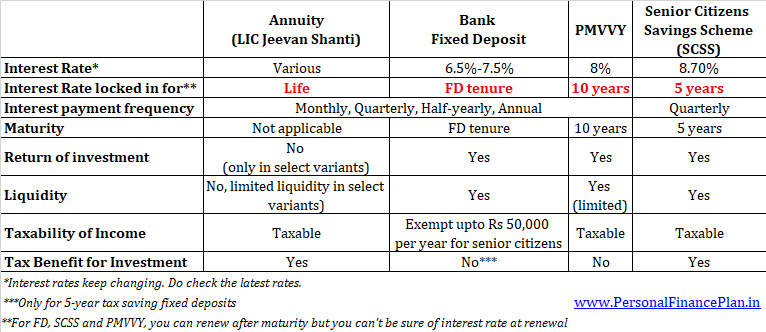

은퇴 중 소득 창출을 위한 대안도 살펴봐야 합니다. 고정 예금이나 부채 뮤추얼 펀드에 투자할 수 있습니다. 고령자인 경우 Pradhan Mantri Vaya Vandana Yojana(PMVVY) 및 Senior Citizens Savings Scheme(SCSS)에 추가 옵션이 있습니다.

선택할 때 수익률(이자율), 과세 가능성 및 유동성을 살펴봐야 합니다.

다음은 LIC Jeevan Shanti, 은행 FD, SCSS 및 PMVVY를 간략하게 비교한 것입니다.

이것은 양자택일 전략이 아님을 유의하십시오. 현명한 은퇴 전략은 이러한 제품을 혼합하여 활용할 수 있습니다.

투자자 입장에서 이 상품은 이해하기 쉽습니다.

또한 연금 플랜의 모든 이점이 있습니다. 이전 섹션에서 이러한 연금 혜택에 대해 설명했습니다.

반면에 LIC Jeevan Shanti는 연금 계획의 모든 결함을 가지고 있습니다. 또한 이연 연금 변형은 이해하기 쉽지 않습니다.

즉시 연금 플랜의 변형은 LIC Jeevan Shanti 및 LIC Jeevan Akshay 플랜 모두에서 동일합니다. 따라서 LIC에서 즉시 연금 플랜을 구매하기로 결정했다면 , 두 플랜에서 원하는 변형에 대한 연금 요율을 비교하기만 하면 됩니다. 더 나은 연금 요율을 제공하는 플랜을 선택하십시오.

LIC에서 연기된 연금 계획을 구매하려면 LIC Jeevan Shanti가 유일한 옵션입니다(LIC Jeevan Akshay와 LIC Jeevan Shanti 사이).

당신이 50세라고 가정해 봅시다. 60세에 은퇴하면 현금 흐름이 필요합니다.

현금 흐름을 생성하기 위해 연금 경로를 택한다고 가정하면 두 가지 옵션이 있습니다.

접근법 1에서는 LIC Jeevan Shanti-Deferred annuity-10년에 Rs 10 lacs를 투자합니다. 연기 기간이 끝나면 연간 Rs 130,824의 수입을 얻게 됩니다.

접근법 2에서는 금액을 어딘가에 투자하고 투자 판매 수익을 사용하여 10년 후 즉시 연금 플랜을 구매합니다.

즉시 연금이 일정하다고 가정 , 연간 Rs 130,824의 연금을 받으려면 10년 후 Rs 14.38 lacs가 필요합니다.

루피 14.38 lacs에 어떻게 도달했습니까?

130,824/90,942*10 lacs =14.38 lacs, 60세 및 구매 가격을 반환하지 않는 즉시 연금(옵션 A)의 경우 해당 가치는 Rs 90,942입니다.

이제 10년 안에 루피 10락이 루피 14.38락으로 성장하려면 연 3.7%의 세후 수익률이 필요합니다. 달성하기 쉬워야 합니다.

10년이 끝날 때 구매 가격을 반환하지 않고 연금(옵션 F)을 구매한다고 해도(연봉 130,824루피) 루피 19.3락이 필요합니다. .

130,824/67,482* 10 lacs =19.3 lacs

Annuity value for Rs 10 lacs purchase, 60 years, Immediate annuity with return of purchase price =Rs 67,482

To get to Rs 19.3 lacs in 10 years, you need post-tax return of 6.8% p.a. Not very difficult again.

However, the caveat is that the immediate annuity rates may change over the next 10 years. If the annuity rates move lower in the interim, you need a much larger corpus to achieve the same level of income. For a larger corpus, you need higher returns.

Therefore, Approach 1 provides guaranteed pension while Approach 2 carries some risk.

Are you willing to take such a risk?

Assuming you have decided to go with an annuity plan, you still need to select the annuity variant.

The choice between immediate annuity plans is relatively simpler.

It will depend on your requirement.

If you want to leave a legacy for your family, you should consider Option F and J.

If you want to ensure pension for your spouse too, consider Options H, I or J.

If you want your annuity pay-outs to grow gradually, you may opt for Option G.

If you want higher income but want to ensure cashflows to the family for a minimum period, Options B/C/D/E may be the right choice for you.

If you merely want to maximize income (and are not concerned about leaving a legacy), you may like Option A the most.

However, in my opinion, the choice between the deferred annuity variants is quite complex. Since the death benefit is dynamic and the age of the second annuitant also matters, there are so many permutations and combinations I can think of.

For instance, if you are 60 and want to purchase a plan with deferment of 10 years (Option 1, single life) , you will get an annual pension of Rs 1.37 lacs (after the end of deferment period).

However, if you were to add a second annuitant (aged 30) in the same plan (Option 2, joint life), you will get an annual pension of Rs. 1.2 lacs.

So, a higher pension under Option 1.

If the deferment period were to be increased to 20 years, you will get a pension of Rs 1.49 lacs under Option 1 and Rs. 2.19 lacs under Option 2. Now, higher pension under Option 2.

Complicated, isn’t it?

Which variant will you choose?

We have discussed only deferred annuity variants earlier. The immediate annuity variants are explained with illustrations below.

Immediate annuity, single life

Pension Benefit :You will get pension throughout life. Pension will stop after your death.

Death Benefit :Nominee will not get anything after demise of the annuitant. Payment of pension will also stop.

Maturity Benefit :Not applicable

Surrender Benefit :Not allowed. This means that you or your nominee will never get the invested amount back.

The annuity rates are the highest under this option because the insurer has to pay only till the end of purchaser’s life. No payments (lumpsum or annuity) to be made after investor’s demise.

Example

A 60 year old person invests Rs 10 lakh in Option A. The total outgo will be Rs 10.18 lacs (inclusive of GST).

If you look at the corresponding age and option (i) in the table, you will find 90,942.

This means you will get Rs 90,942 per annum.

You will get this pension for life. Pension will stop after your death. No annuity or lump sum will be given to your spouse or nominee .

In case of an early death, your money goes to the sink. For instance, if the investor dies after two years, he would have got pension of only Rs 1.82 lacs (90,942 X 2). Nothing will be given to spouse or nominee after the demise of the investor.

Immediate annuity, single life

Under this variant, you can choose from 4 options for Guaranteed period:5 years, 10 years, 15 years or 20 years

Pension Benefit :

You will get pension for life.

If you pass away before the end of the guaranteed period, the nominee will get the pension till the end of the guaranteed period. The pension to the nominee will stop at the end of the guaranteed period.

If you pass away after the expiry of the guaranteed period, the pension will stop after your demise. Nothing will be paid to your nominee.

As expected, the lower the guaranteed period, the higher the interest rate.

Death Benefit :No lumpsum payout shall be made to the nominee after demise of the investor. As mentioned above, if the purchaser were to die before the end of guaranteed period, the nominee will get the pension till the end of such period.

If the investor passes away after the end of guaranteed period, the nominee gets nothing.

Maturity Benefit :Not applicable

Surrender Benefit :Not permitted

Illustration

A 60 year old person invests Rs 10 lakh in Option D (15 years). The total outgo will be Rs 10.18 lacs (inclusive of GST).

From the table (60 years and option ii), you can check that the corresponding value is Rs 86,250. For an investment of Rs 10 lacs, you will get an annual pension of 86,250 rupees.

You will get this pension for your entire life.

But if you die after 6 years, then your nominee will get pension for the remaining 9 years (15 years – 6 years). Pension to the nominee will stop at the end of guaranteed period.

If the you pass away after 15 years (end of guaranteed period), then the pension will stop after your demise. Your nominee will not get anything.

Immediate annuity, single life

The only difference between Option A and Option F is that, under Option F, the purchase price is returned to the nominee. Since the liability of the insurer is higher under Option F, the annuity rate is also lower (as compared to Option F)

Pension Benefit :You will get pension for life. Pension will stop after your death.

Death Benefit :On the death of the investor, the payment of pension will stop and the investment amount will be returned to the nominee. If you had invested Rs 10 lakh, then 10 lakh rupees will be returned to the nominee. GST charged at the time of will not be returned.

Under Jeevan Shanti, the nominee has the option to get the death benefit as lump sum. Or he can use the death benefit amount to purchase an immediate annuity plan. Or he can choose to receive the benefit in the form of monthly/quarterly/half-yearly/annual investments over 5, 10 or 15 years. LIC Jeevan Akshay provides the option of only lump sum.

Maturity Benefit : Not applicable

Surrender Benefit : You can surrender the policy one year after taking the policy.

Surrender Value will depend on your age at the time of surrender. I am not sure how to calculate this amount.

Illustration

A 60 year old person invests Rs 10 lakh in Option 3. The total outgo will be Rs 10.18 lacs (inclusive of GST).

From the table, you can check that the corresponding value (60 years and Option iii) is Rs 67,482. For an investment of Rs 10 lacs, you will get an annual pension of 67,482 rupees.

You will get the pension for life. Pension will stop after your death.

10 lakhs will be returned to your nominee on the amount of death. Alternatively, the nominee can choose to purchase an immediate annuity with the amount or the receive the benefit in installments.

Immediate annuity, single life

Pension Benefit :You will get pension for life. Your pension will increase by 3% every year.

Death Benefit :On the death of the investor, the pension (annuity payments) will stop. Nominee will not get anything.

Maturity Benefit :Not applicable

Surrender Benefit :Not permitted

Illustration

A 60 year old person invests Rs 10 lakh in Option G. The total outgo will be Rs 10.18 lacs (inclusive of GST).

For an investment of Rs 10 lacs, you will get a pension of Rs 72,888 in the first year.

In the second year, the pension amount will increase by 3% i.e. Rs. 75,074

In the third year, the pension will increase to Rs. 77,261.

Similarly, the pension amount will continue to rise throughout your life.

Pension will stop after your death. Your nominee will not get anything back.

Immediate annuity, Joint Life

Pension Benefit :The investor will get pension for life. After the death of the investor, the spouse will get pension for his/her life. However, the spouse will get only 50% of the pension amount (that was being paid to the investor).

Death Benefit :50% of the pension will be paid to the spouse on the death of the investor.

After the demise of the spouse, the pension will stop and the nominee will not get anything.

If the spouse passes away before (predeceases) the investor, the pension will stop after demise of the investor. Nominee will not get anything.

Maturity Benefit :Not applicable

Surrender Benefit :Not permitted

Illustration

A 60 year old person invests Rs 10 lakh in Option H. The total outgo will be Rs 10.18 lacs (inclusive of GST).

The corresponding value in the table for the age of 60 and Option H is 85,638.

You will get this pension for life. After you, your spouse will get half this amount for life i.e. your wife (or husband) will get an annual pension of 85,638 * 50% =42,819.

After the death of your spouse, pension will stop. Nominee will not get anything.

If your spouse predeceases (passes away before) you, the pension will stop on your demise. Your family or nominee will not get anything.

Immediate annuity, Joint Life

Only a minor difference as compared to option H.

Under Option H, after investor’s demise, the spouse got 50% pension for life.

Under Option I, after investor’s demise, the spouse will get 100% pension for life.

Since the liability of the insurance company is higher under Option 6, the annuity rate for Option 6 is lower as compared to Option 5.

Illustration

A 60 year old person invests Rs 10 lakh in Option 6. The total outgo will be Rs 10.18 lacs (inclusive of GST).

The corresponding value in the table for the age of 60 and Option I (or option vi) is 80,844.

For an investment of Rs 10 lacs, you will get a pension of Rs 80,844 per annum.

You will get this pension for life. After you, the exact same pension will continue to your spouse. Your wife (or husband) will get an annual pension of Rs. 80,844.

After the death of your spouse, pension will stop. Nominee will not get anything.

If your spouse predeceases (passes away before) you, the pension will stop on your demise. Your family or nominee will not get anything.

Immediate annuity, Joint Life

Under Option I, the family gets nothing after the demise of husband and wife.

The difference in option J is that after the death of husband and wife, the investment amount is returned to the nominee.

Pension Benefit :The investor will get pension for life. After the death of the investor, the spouse will get the 100% pension for his/her life.

Death Benefit :100% of the pension will be paid to the spouse on the death of the investor. Under Jeevan Shanti, the nominee has the option to get the death benefit as lump sum. Or he can use the death benefit amount to purchase an immediate annuity plan. Or he can choose to receive the benefit in the form of monthly/quarterly/half-yearly/annual investments over 5, 10 or 15 years. LIC Jeevan Akshay provides the option of only lump sum.

After the demise of the spouse, the pension will stop and the nominee will be given back the investment amount.

If the spouse passes away before (predeceases) the investor, the pension will stop after demise of the investor. The investment amount will be returned to the nominee.

Maturity Benefit :Not applicable

Surrender Benefit :Not permitted

Illustration

A 60 year old person invests Rs 10 lakh in Option J. The total outgo will be Rs 10.18 lacs (inclusive of GST).

The corresponding value in the table for the age of 60 and Option J (or option vii) is 67,074.

For an investment of Rs 10 lacs, you will get a pension of Rs 67,074 per annum.

You will get this pension for life.

After you, the exact same pension will continue to your spouse. Your wife (or husband) will get an annual pension of Rs. 67,074.

After the death of your spouse, pension will stop. Your nominee will get Rs 10 lacs.

If your spouse predeceases (passes away before) you, the pension will stop on your demise. Your nominee will get Rs 10 lacs. Alternatively, the nominee can choose to purchase an immediate annuity with the amount or the receive the benefit in installments over 5/10/15 years.