누군가에게 자신이 주식 시장의 투자자라고 말할 때 이 질문을 받은 적이 있습니까?

나는 이 질문을 셀 수 없이 많이 받았다는 것을 알고 있습니다. 비록 특정 단어를 다른 말로 바꾸어 표현하기는 했지만요.

그러나 주요 메시지는 명확합니다.

일반 개인 투자자가 자신의 게임에서 전문가를 이길 수 있습니까?

One Up on Wall Street에서 , 전설적인 투자자 Peter Lynch는 자신의 '아마추어 ' 피델리티의 수십억 달러 규모의 마젤란 펀드를 관리하는 접근 방식은 그를 미국 최고의 머니 매니저이자 역사상 가장 성공적인 투자자 중 한 명이 되도록 이끌었습니다.

1977년 5월부터 1990년 5월까지 Lynch는 S&P 500의 15.52%에 비해 29.06%의 연간 수익률로 Magellan을 이끌었습니다. 상황을 설명하기 위해 Magellan에 $1, S&P 500.

그의 만트라는 간단합니다:

보통 투자자는 자신의 분야에서 전문가가 될 수 있으며 약간의 조사를 통해 월스트리트 전문가만큼 효과적으로 성공적인 주식을 고를 수 있습니다.

이 방대한 기사에서 Peter Lynch의 책에서 얻은 핵심 내용, 즉 Peter Lynch의 주식 투자에 대한 일반 지침을 분석하고자 합니다.

Peter Lynch가 가르치는 교훈은 5가지 간단한 내용으로 나눌 수 있습니다.

이 책에서 설교하는 첫 번째 규칙은 전문가의 말을 듣지 말라는 것입니다. !

즉, 자신의 연구를 위해 인기 있는 팁, 중개 회사의 권장 사항 및 좋아하는 뉴스레터의 최신 "놓칠 수 없는" 제안을 무시합니다.

사실, 아마추어 투자자는 많은 장점이 내재되어 있으며 이를 악용할 경우 전문가는 물론 시장 전반의 성과를 능가하게 됩니다.

이는 다음 요인 때문입니다.

전문가들은 많은 자본에 접근할 수 있기 때문에 주머니가 매우 깊습니다. 그러나 이는 중소형 시가총액에 투자할 수 없다는 단점이 있다. 그것은 단순히 펀드 전체 성과에 의미 있는 영향을 미치지 않을 것입니다.

이것이 Warren Buffett이 소형 시가 주식에 대한 투자에서 나중에 회사 전체를 사는 것으로 전환한 이유입니다.

일반 개인 투자자가 이용할 수 있는 기회는 대규모 투자자의 기회보다 훨씬 많습니다. 그것은 Pasir Ris 연못에서 낚시하는 것과 비교하여 물고기의 바다에서 따는 것과 같습니다.

우리는 그것을 활용하기만 하면 됩니다.

알려지지 않은 회사에서 비정상적으로 큰 이익을 얻을 수 있는 기회와 기존 회사에서 적은 금액만 잃을 수 있다는 확신 사이에서 전문가들은 후자에 뛰어들 것입니다.

성공도 중요하지만 실패했을 때 나쁘게 보지 않는 것이 더 중요합니다. 이는 펀드매니저가 직원이고 그들의 업무는 대부분 그들의 성과에 달려 있기 때문입니다.

고객들은 DBS나 Keppel에서 작게 지고 Goodland Group Ltd에서 크게 이겼다는 소식을 듣고 싶어 합니다.

한편, 평범한 사람은 우리가 잘 알려지지 않은 카운터를 샀던 이유를 알려주기 위해 이른 아침이나 늦은 밤까지 우리에게 전화를 걸어 오는 사람이 없습니다.

우리는 잠재적인 반발에 직면하기 위해 20분 길이의 설명 대본을 준비할 필요 없이 스스로 결정을 내립니다.

따라서 Peter Lynch는 시간을 보다 생산적으로 활용할 수 있으므로 시장에서 이러한 이점을 활용하도록 권장합니다.

무엇보다도, 불행한 상황에서 주식 탱크가 있는 경우 아무도 투자 결정과 행동에 영향을 미칠 수 있는 귀하의 사전 판단을 비판할 사람이 없을 것입니다.

펀드 매니저가 다른 사람의 돈을 관리한다는 사실 때문에 이 펀드 매니저가 처분할 수 있는 자본의 양을 결정하는 것은 고객입니다.

이 사람들은 일반적으로 정통한 투자자가 아니며 약세장에서 돈을 회수하고 강세장에서 돈을 되돌리는 경향이 있습니다. 이것은 해야 할 일의 정반대입니다. 이로 인해 펀드 매니저는 모든 것이 너무 비싸면 너무 많은 자본을 보유하고 모든 것이 싸게 팔릴 때 너무 적은 자본을 갖는 딜레마에 빠지게 됩니다.

한편, 우리는 우리 자신의 펀드 매니저이며 자본을 투입하고 인출할 시기를 결정할 수 있는 유일한 권한을 가지고 있습니다. 이는 자본을 의미 있게 전략화할 때 중요한 이점을 제공합니다.

당신이 무시하는 법을 배워야 하는 당신의 약한 마음 외에는 주식이 탱크에 있을 때 당신에게 자본을 빼라고 부르는 사람은 없을 것입니다. (Lynch는 다음 섹션에서 다룰 심리적인 측면을 매우 중요하게 생각합니다.)

현재 시스템에서는 많은 대형 기관이 그 적합성을 인식하고 동일한 수의 분석가(다양한 산업 및 회사를 추적하는 연구원)가 해당 주식을 매수 또는 추가 목록에 올릴 때까지는 주식이 진정으로 매력적이지 않습니다.

즉, 주식의 분석 보고서가 발표될 때 스마트 머니가 현재 보고하는 가격과 비교하여 훨씬 저렴하고 매력적인 가격으로 해당 주식을 이미 구입했는지 확인해야 합니다.

따라서 이러한 "매수" 또는 "추가" 보고서에 의존하여 주식을 식별하지 않고 자신의 기준으로 자체 주식을 선별하는 것이 좋습니다.

이것은 또한 그러한 분석 보고서가 자신의 투자 범위에 비해 단기 범위를 가지고 있기 때문입니다. 애널리스트는 자신이 설정한 목표 가격을 기준으로 주식 등급을 매기며 일반적으로 이러한 목표는 12개월(1년) 기간에 제공됩니다.

투자자(스윙 트레이더 아님)의 경우 1년 동안 주식을 소유하는 것은 위험이 따릅니다.

행동 경제학자 드 본트와 탈러는 사람들이 합리적으로 결정을 내리지 않는다는 사실을 깨달았습니다. 그들의 결정은 그들이 싸워야 하는 방대한 양의 인지 오류로 인해 왜곡되었습니다.

따라서 1년의 보유 기간을 갖는 것은 시장이 결국 속담의 계량기로 기능하기까지 시간이 걸리기 때문에 투자자를 시장 변동에 노출시킵니다.

팩터 기반 투자 가이드에서 보유 기간에 대해 자세히 알아보세요.

우리 모두는 다음과 같이 말할 기회가 있습니다. “대단합니다. 주식이 궁금해" 전문 분석가가 원래의 단서를 얻기 훨씬 전에.

우리 모두는 보통 사람보다 더 많이 알고 있는 특정 산업, 제품 및 서비스를 가지고 있습니다. 아마도 당신은 레벨 99 마술사 닌자이고 당신이 만지는 모든 게임을 지배하기 때문에 게임 산업에 대해 더 많이 알고 있을 것입니다. 아마도 당신은 패션 업계에서 일하고 있으며 최신 트렌드에 동조하고 있을 것입니다.

린치는 보통 사람이 1년에 2~3번, 때로는 그 이상 가능성이 있는 잠재 고객을 만난다고 말합니다.

결론은 우리 모두는 일상 생활을 통해 상장 기업에 대한 가치 있고 관련성 있는 정보를 가지고 있다는 것입니다. 이것은 전문가들이 아직 알지 못하거나 100시간의 연구를 통해 얻은 정보입니다.

인간의 감정은 우리를 끔찍한 주식 시장 투자자로 만든다고 Peter Lynch는 말합니다.

무지한 투자자는 계속해서 세 가지 감정 상태를 왔다갔다 합니다.

그/그녀는 관심 있습니다. 시장이 하락했거나 경제가 흔들리고 있어 좋은 기업을 저렴한 가격에 사지 못하는 경우

그런 다음 다음 상승세가 도래하면 더 높은 가격에 다시 진입하고 만족합니다. 보유 자산이 늘어나고 있기 때문입니다. 이것이 바로 현재 가격에 대한 펀더멘털을 확인하고, 그것이 과대평가되고 부풀려져 있는지(그러나 그는 그렇지 않음) 결정하기 위해 충분히 관심을 가져야 할 때입니다.

마지막으로, 그의 주식이 어려운 시기에 하락하고 가격이 그가 지불한 금액 아래로 떨어지면 그들은 항복합니다. 순식간에 판매됩니다.

많은 사람들이 스스로를 "장기 투자자 그러나 다음 큰 하락(또는 작은 이익)까지만 가능하며, 그 시점에서 그들은 빠르게 단기 투자자가 되어 막대한 손실이나 가끔 발생하는 작은 이익을 위해 매도합니다.

비결은 당신의 직감을 신뢰하는 법을 배우는 것이 아니라, 그것을 무시하도록 자신을 훈련하는 것입니다. 회사의 펀더멘털이 변하지 않는 한 주식을 고수하십시오.

Lynch는 시장의 기복과 금리에 대한 끝없는 투기를 무시한다면 장기적으로 기본적으로 올바른 선택을 하면 포트폴리오가 보상을 받을 것이라고 약속합니다.

워렌 버핏의 가장 위대한 장기 투자 중 하나(워싱턴 포스트)조차도 처음 몇 년 동안은 완전히 패자처럼 보였습니다.

워싱톤 포스트의 주식은 버핏이 인수한 후 약 20% 폭락했고 3년 동안 그 자리에 있었습니다! 약 220만 달러의 종이 손실이 발생했습니다. 그러나 Warren은 재무제표를 재검토하여 비즈니스 펀더멘털에 큰 변화가 없음을 발견했습니다. 따라서 그는 시장이 Post의 진정한 가치를 깨닫기를 기다리기로 결정했습니다. 2007년 말까지 Post에 대한 그의 지분은 10,000% 이상 증가한 14억 달러로 성장했습니다.

장기 수익률이 높은 주식은 단기적으로는 정말 고된 투자가 될 수 있습니다.

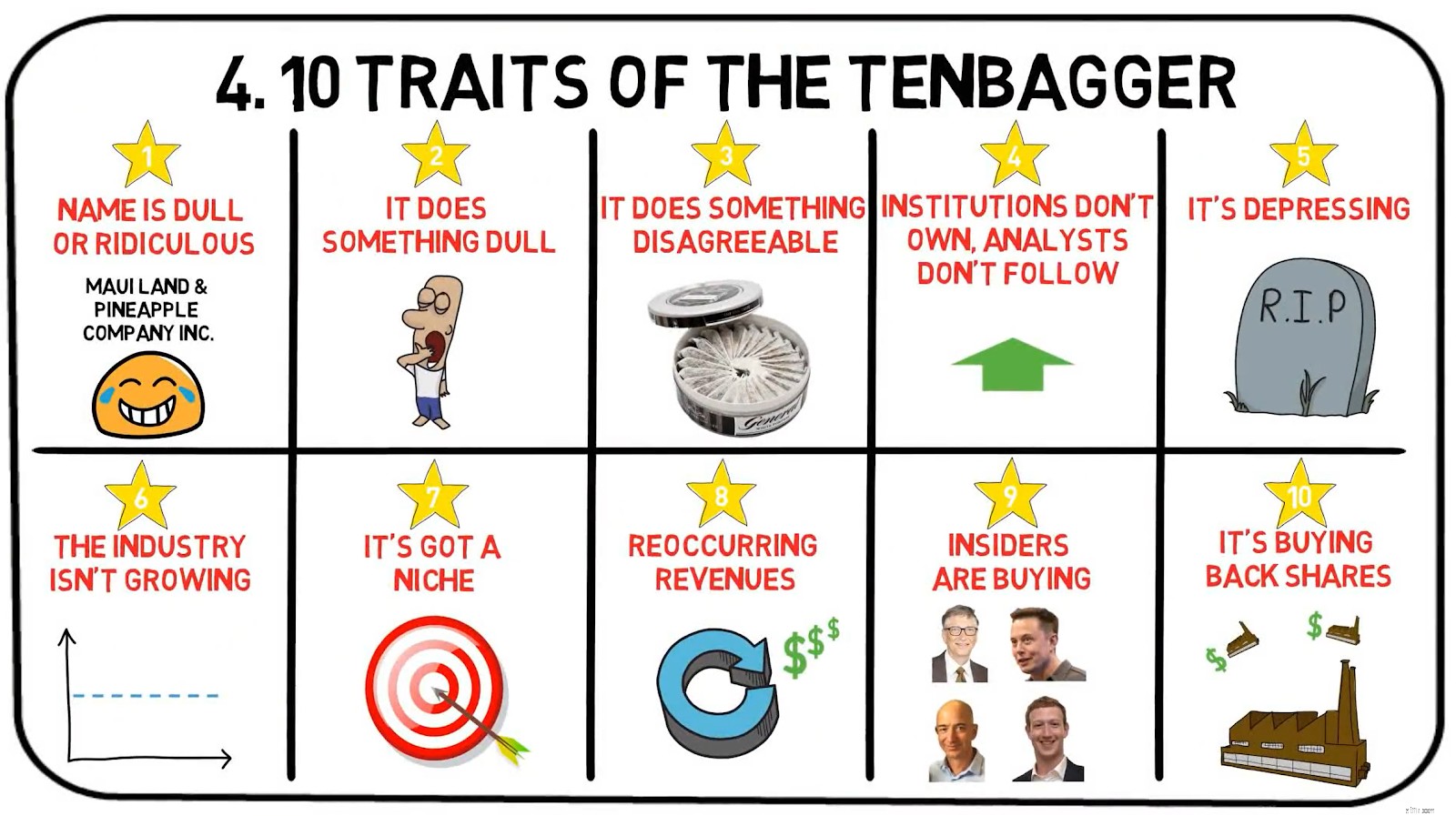

전설적인 '텐배거(Tenbagger)'는 린치가 구매 가격이 10배나 오른 주식을 설명하는 데 사용하는 표현입니다. One Up on Wall Street에서 그는 그러한 Tenbaggers가 포함해야 하는 몇 가지 특성을 나열합니다.

Peter Lynch는 그의 책에서 Greatest Company Of All을 제시합니다. – 이상적인 린치 텐배거.

이 신화적인 회사의 이름은 케이준 클렌저입니다.

꿈의 기업의 속성에 대한 장에서 설명한 마법 같은 회사는 Peter Lynch였습니다.

케이준 클렌저는 아열대 습도의 피해를 입은 가구, 희귀 서적 및 커튼의 곰팡이 얼룩을 제거하는 지루한 사업에 종사하고 있습니다. 뉴욕이나 보스턴의 분석가는 케이준 클렌저를 방문한 적이 없으며 어떤 기관도 주식을 매입하지 않았습니다.

칵테일 파티에서 케이준 클렌저를 언급하면 곧 자신과 이야기하게 될 것입니다. 귀에 들리는 모든 사람에게 우스꽝스럽게 들립니다.

케이준 클렌저는 전국적으로 빠르게 확장하면서 놀라운 매출을 올렸습니다. 회사가 옷, 가구, 카펫 및 욕실 타일에서 모든 종류의 얼룩을 제거하는 새로운 젤에 대한 특허를 공개했기 때문에 이러한 판매는 곧 가속화될 것입니다. 이 특허는 케이준이 찾던 틈새 시장을 제공합니다.

회사는 모든 표면에서 발생하는 미래의 모든 얼룩 사고에 대한 보장된 제거에 대해 미리 지불할 수 있는 연간 할부로 평생 오염 방지 보험을 제공할 계획입니다.

이 주식은 7년 전 IPO에서 $8에서 시작하여 곧 $10로 상승했습니다. 그 가격에 중요한 기업 이사들은 그들이 감당할 수 있는 한 많은 주식을 샀습니다.

회사를 방문하여 훈련된 갑각류라면 누구나 젤 제조를 감독할 수 있다는 것을 알게 되었습니다.

케이준 클렌저는 가상의 사업이지만 전설적인 마젤란 펀드 매니저의 눈에는 텐배거가 어떻게 생겼는지 느낄 수 있습니다. 앞서 언급한 스토리 설명은 우리가 속한 여러 기업의 비즈니스 모델과 기존 환경에서 그리 멀지 않다.

인기 있는 주식은 일반적으로 알려진 가치의 랜드마크가 보이지 않는 곳에서 빠르게 오를 수 있지만, 이를 뒷받침할 희망과 희박한 공기 외에는 아무것도 없기 때문에 빠르게 하락합니다.

보니타스 리서치가 프리미엄 스킨케어 회사의 수익에 대한 진정성과 합법성에 의문을 제기하는 28페이지 분량의 보고서를 발표한 후 폭락한 뜨거운 주식 베스트 월드를 살펴보겠습니다.

가장 인기 있는 업계에서 가장 섹시한 주식 외에 Peter Lynch가 확실히 피해야 할 주식의 4가지 다른 특성은 다음과 같습니다.

누군가가 주식을 차세대 'Facebook'이나 'Google'이라고 부를 때 조심하십시오. 거의 그렇지 않기 때문입니다.

사실, 이것들은 단지 마케팅 전술일 뿐이며 당신이 더 읽어보게 하기 위해 전술적으로 배치된 미끼를 클릭합니다.

"이 주식인 ABCXYZ는 주당 2달러에 Facebook을 사는 것과 같을 수 있습니다."

종종 그들은 그러한 주식을 대기업에 비유하여 관련성을 높이고 소문으로 매수하는 무지한 투자자를 끌어들입니다.

이것은 차례로 그들을 유혹하고 다음으로 알다시피 그는 은퇴를 위해 저축한 돈의 절반을 ABCXYZ의 주식을 사는 데 사용하고 친구들에게 자신이 일찍 탔다고 자랑스럽게 선전합니다.

어떤 사람들은 이것을 다각화라고 부르지만 Lynch는 잘못된 결정을 Di더 나쁘게 표현하는 것을 좋아합니다. 화해.

주식을 다시 사거나 배당금을 늘리는 대신 수익성 있는 회사는 종종 어리석은 인수에 돈을 날리는 것을 선호합니다.

종종 회사의 확장이 핵심 운영과 관련이 있는지 자문해야 합니다.

몇 가지 가상의(과장된) 예는 다음과 같습니다.

어리석게 들릴 것입니다. 그런 인수에 대한 아이디어가 경영진과 리더십의 심사를 어떻게 통과했는지 의아해할 수 있습니다. 어려운 사실은 그런 형편없는 확장이 존재한다는 것입니다.

Hyflux에 대한 사람들의 고통스러운 교훈을 활용하면 회사가 물 솔루션 혁신에서 전력 및 에너지 생성으로 확장함에 따라 혼란스러운 다양화 사례를 볼 수 있습니다.

싱가포르 및 아시아 최초의 Tuaspring Integrated Water and Power Project는 효율성 수준을 높이고 담수화 비용을 절감할 것으로 기대되었습니다.

발전소는 2016년에 문을 열었고 Hyflux의 에너지 사업에 대한 첫 번째 벤처였습니다.

Hyflux가 Tuaspring을 제외하여 수익과 수입을 보고하기로 선택한 방법에 주목하십니까?

Tuaspring이 회사의 수익과 이익에 걸림돌이 되었기 때문입니다. Hyflux는 현지 에너지 시장의 "장기적인 약세"가 손실의 주요 원인 중 하나라고 밝혔습니다.

여기에서 그 운명적인 교훈에 대해 자세히 읽어보십시오.

이러한 주식을 "롱샷"이라고 합니다.

그들은 종종 모든 종류의 암을 치료하거나, 지구 온난화를 해결하거나, 세계 평화를 만드는 것과 같은 기적적인 일을 하기 직전에 있다고 생각합니다.

속삭임은 최면 효과가 있으며 일반적으로 이야기에는 감정적 호소력이 있습니다. 스테이크가 없다는 사실을 잊어 버릴 정도로 지글지글한 맛이 나는 곳입니다.

Moringa Elixir가 모든 종류의 질병을 해결하겠다고 약속하는 MLM 계획과 매우 흡사합니다...

돈을 잃었다는 사실 외에 이 모든 롱샷의 공통점은 아무 내용도 없는 훌륭한 스토리가 있다는 것이었습니다.

매출의 25~50%를 단일 고객에게 의존하는 회사는 위태로운 상황이다.

고객 한 명을 잃는 것이 공급업체에 치명적이고 매출에 막대한 피해를 입힐 경우 Lynch는 공급업체에 대한 투자를 경계할 것입니다.

2018년 AEM Holdings 하나의 주요 고객에 크게 의존했지만 회사에서 구체적으로 밝히지는 않았지만 약 93% 기여한 미국 최대 칩 제조업체 중 하나인 Intel로 여겨집니다. 총 수익 중

이것은 또한 약한 교섭 위치에 있으며 회사는 잠재적으로 이 유일한 고객에 의해 압박을 받아 영향을 받을 수 있습니다.

책의 마지막 장에서 Lynch는 더 깊이 파고들기 전에 주식에 대해 배우고 싶은 중요한 사항 중 일부(전부는 아님)에 대한 요약 체크리스트를 공개합니다.

부지런한 연구를 할 때 Peter Lynch의 평범한 단순함에 혼동하지 마십시오. 엄격한 연구는 그의 성공의 초석이었습니다.

훌륭한 아이디어의 초기 불꽃을 추적할 때 Lynch는 구매할 가치가 있는 모든 주식에 대해 충족될 것으로 기대했던 몇 가지 기본 가치를 강조합니다.

알 수 있듯이 Peter Lynch는 정량적 분석을 시작하기 전에 정성적 분석을 사용하여 주식을 식별합니다.

하지만 Dr. Wealth에서는 정성적인 내용을 다루기 전에 주식에 대한 정량적 분석을 수행해야 한다고 생각합니다.

그렇게 하면 당신에게 해를 끼칠 수 있는 모든 감정적 편견을 무시할 수 있습니다.

우리는 두 가지 접근 방식이 모두 효과가 있다는 점을 강조하고 싶습니다. 연구에서 어느 쪽이든 잊지 마십시오.

모든 주식 연구는 양적 요소와 정성적 요소로 구성됩니다.

지금까지 유용한 정보를 배웠기를 바랍니다. 다음 몇 세션에서 저는 Peter Lynch가 사용한 3가지 주식 카테고리에 대해 알아볼 것입니다. 그들은:

Peter Lynch에는 실제로 6개의 주식 카테고리가 있습니다. 느린 성장자, 견고함, 빠른 성장자, 순환, 자산 재생, 턴어라운드.

또한 저처럼 미국 최고의 머니 매니저에게 감동과 감동을 받았다면 그의 책을 구매하는 것도 고려해 볼 수 있습니다. 전자 방식으로 책을 읽는 것이 당신의 스타일이라면 킨들 버전이 더 저렴할 수 있습니다.

그런데 구조화된 투자 전략을 공유하기 위해 정기적인 입문 과정을 개최합니다. 성장주를 찾기 위해 몇 가지 자체 전략을 결합한 방법을 알고 싶다면 여기에서 자세히 알아볼 수 있습니다.

Stalwarts는 더 느리고 안정적인 성장을 통해 더 큰 회사로 성장한 이전의 빠르게 성장하는 회사입니다(연간 3%가 예상 평균). ).

또한 건실한 회사는 필요하고 항상 수요가 있는 제품을 생산합니다(음식, 물, 전기, 기름을 생각 ) , 이는 강하고 안정적인 현금 흐름을 보장합니다.

비록 그들이 시장에서 최고의 성과를 낼 것으로 기대되지는 않지만 좋은 가격에 구입한다면 충실한 기업은 4-5년의 보유 기간 동안 약 50% 정도의 상당한 이익을 제공합니다.

필요한 제품에서 생성되는 강력한 현금 흐름으로 인해 충실한 사람들은 일반적으로 배당금을 지불할 수 있습니다.

충실한 기업의 예로는 맥도날드, SBS 트랜짓, 프록터&갬블이 있습니다.

또한 Peter Lynch는 Stalwarts에게 1.0 미만의 P/E 성장 비율(PEG)을 요구했습니다. PEG 비율은 회사의 가격 대비 수익을 나누어 계산합니다. (PE) 수익 성장률에 따른 비율 .

Lynch는 PEG가 1.0 미만인 회사는 가격이 저렴하고 PEG가 0.5 미만인 회사는 매우 저렴한 것으로 간주했습니다. PEG가 1 미만인 회사를 사는 경우 1달러의 수익 성장에 대해 1달러 미만을 지불하게 되므로 이는 이해하기 쉽습니다. 더 적은 비용으로 더 많은 비용을 지불하는 것이 모든 투자의 기본 원칙입니다.

배당금을 지급하는 회사의 경우 Lynch는 배당금 수익률을 추가로 고려하여 수익률 조정 PEG 비율에 도달했습니다. Walmart는 종종 Lynch의 Stalwart 주식 방법론의 좋은 예로 인용되었습니다.

한 시점에서 Wal-Mart는 20배에 가까운 PER에 거래되었습니다. 이는 평균 투자자가 수익 1달러당 20달러를 지불한다는 것을 의미했습니다.

Lynch는 회사가 여전히 20-30%의 성장을 하고 있고 더 많은 성장의 여지가 있다고 판단했습니다.

이는 투자자가 지불하게 될 실제 수익 대비 가격이 향후 몇 년 동안 매년 20-30% 낮아질 것임을 의미합니다. 20달러는 흥정이었다. 그리고 Wal-mart는 실망시키지 않았고 향후 20년 동안 20~30%의 성장률을 기록할 것입니다.

이제 우리는 Stalwarts의 특성 중 일부를 알고 있습니다.

우리는 주식 선택을 더욱 엄격하게 하기 위해 몇 가지 추가 기준을 추가했으며 조사할 최고의 주식에만 초점을 좁혔습니다. 이것이 우리가 싱가포르에서 충실한 사람을 찾는 데 사용할 최종 기준입니다.

위의 기준은 다소 자명합니다.

위의 기준을 감안할 때 우리는 오늘 다룰 3개의 충실한 기업을 선정했으며 상당한 성장 잠재력이 있다고 생각합니다. 또한 모든 주식은 투자한 것의 10배의 잠재적 수익을 나타내는 텐배거의 다음 특성 중 하나 이상을 갖습니다.

| 시가총액 | 2억 5300만 달러 |

| 과거 배당 수익률 | 3% |

| 선셋 산업이 아님 | 예 |

| PER 비율 | 21.73 |

| 산업 평균 PER 비율 | 23.8 |

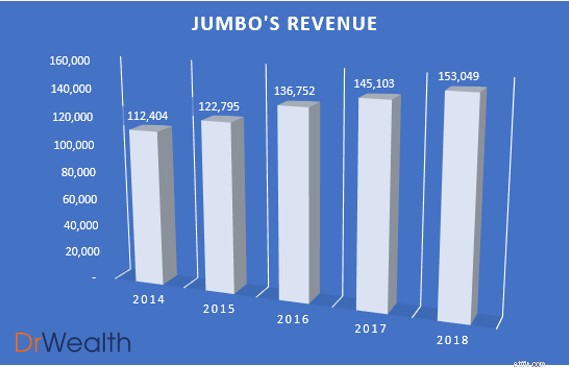

차트에서 볼 수 있듯이 Jumbo의 매출은 2017년 1억 4,500만 달러에서 2018년 1억 5,300만 달러로 5% 성장하면서 매년 성장하고 있습니다.

또한 Jumbo가 중국 및 기타 지역에서 더 확고한 발판을 마련하기 위해 노력함에 따라 수익 성장이 유지되거나 증가할 것으로 예상할 수도 있습니다.

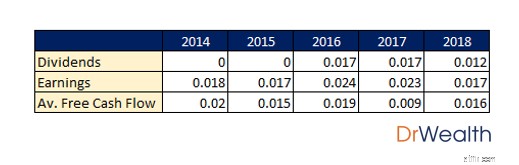

Jumbo는 IPO 이후 지난 3년 동안 배당금을 지급해 왔으며 수익과 잉여 현금 흐름은 2017년을 제외하고 분배된 배당금보다 많습니다.

베이징, 상하이, 대만, 호치민으로 전례 없는 확장을 했기 때문이다. 이는 2017년 잉여 현금 흐름의 하락과 2018년의 배당금 분배 하락을 정당화합니다.

Jumbo는 세 가지 접근 방식을 통해 성장 전망을 해결하는 것을 목표로 합니다.

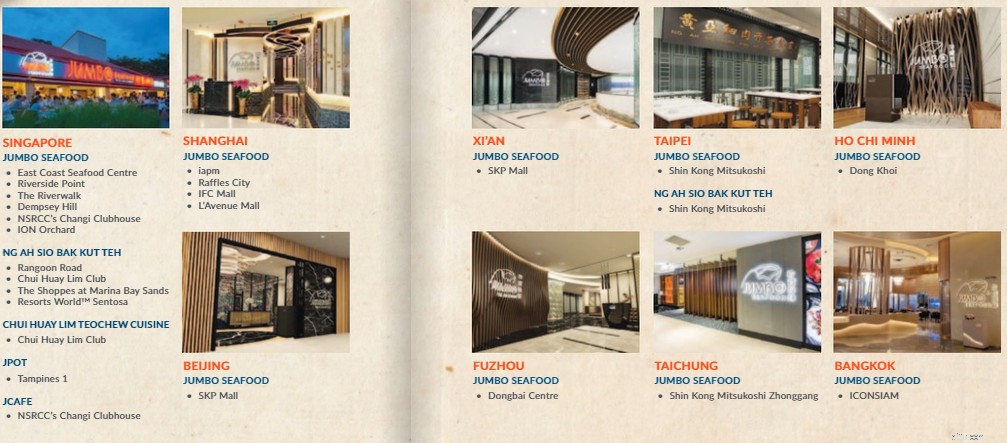

레스토랑 포트폴리오를 다양화함으로써 성공적인 해산물 비즈니스 모델의 일부를 Ng Ah Sio Bak Kut Teh와 같은 다른 브랜드에 복제할 수 있습니다. 따라서 그룹이 잘 실행할 수 있다면 이는 또 다른 수익성 있는 벤처가 될 수 있습니다. Jumbo는 Ng Ah Sio Bak Kut Teh를 중국에 소개할 계획이며 앞으로 12개월 동안 대만에 Ng Ah Sio Bak Kut Teh 매장과 Tsui Wah 홍콩 스타일의 "Cha Chaan Teng" 매장을 1개 더 추가로 열 예정입니다. .

또한, 해외 소비자 시장으로 확장함으로써 Jumbo는 더 큰 소비자 기반에 노출됩니다.

그들이 싱가포르에서 했던 것처럼 성공적으로 브랜드를 구축할 수 있다면 그룹에 밝은 전망이 있을 것입니다.

Edge Singapore는 오늘 Jumbo가 서울 강남에 첫 번째 프랜차이즈 매장을 오픈했다고 보도했습니다. 이로써 방콕, 푸저우, 호치민, 타이페이, 타이중에 프랜차이즈 매장이 있는 아시아 전역의 점보 해산물 수가 18개로 늘어났습니다.

Jumbo는 현재 매출의 약 20.4%를 차지하므로 중국에 대한 투자와 확장이 무르익기 시작했습니다. 이러한 수치는 중국에서의 성공에 대한 강력한 증거입니다.

경영진과 경영진이 중국에서 했던 것처럼 성공적으로 매장을 확장하여 다른 지역 내에서 시장 지위를 구축한다면 잠재적으로 회사 매출의 전례 없는 성장을 볼 수 있습니다.

여전히 회사 수익 성장의 기반을 형성하고 있는 본거지에서 Jumbo는 ION Orchard에 매장을 열었습니다.

이것은 프리미엄 쇼핑 및 엔터테인먼트 벨트인 오차드(Orchard)의 첫 번째 레스토랑으로서 중요한 이정표입니다. 이것은 Jumbo가 해외 확장 중에 있지만 여전히 관련성을 유지하고 주요 판매 소스를 유지하기 위해 현지 시장에서 확장하는 것이 중요하다는 것을 보여줍니다.

틈새가 있습니다

점보라는 이름을 들었을 때 가장 먼저 떠오르는 이미지는 확실히 칠리 크랩/페퍼 크랩입니다. 그것이 바로 점보의 틈새 시장으로, 싱가포르의 상징적/유명한 현지 요리 중 하나를 판매하고 유명합니다.

칠리 크랩 전문 지식을 연마하는 것 외에도 틈새 시장을 확보하면 Jumbo가 입에서 입으로 전해지는 데 매우 친숙해집니다.

경쟁업체보다 이러한 경쟁 우위를 확보하는 것은 경쟁이 치열한 F&B 산업에 속한 Jumbo와 같은 레스토랑에 중요합니다. 이렇게 하면 높은 고객 유지율로 인해 새로운 해산물 진입이 있을 때 매출에 큰 영향을 미치지 않습니다.

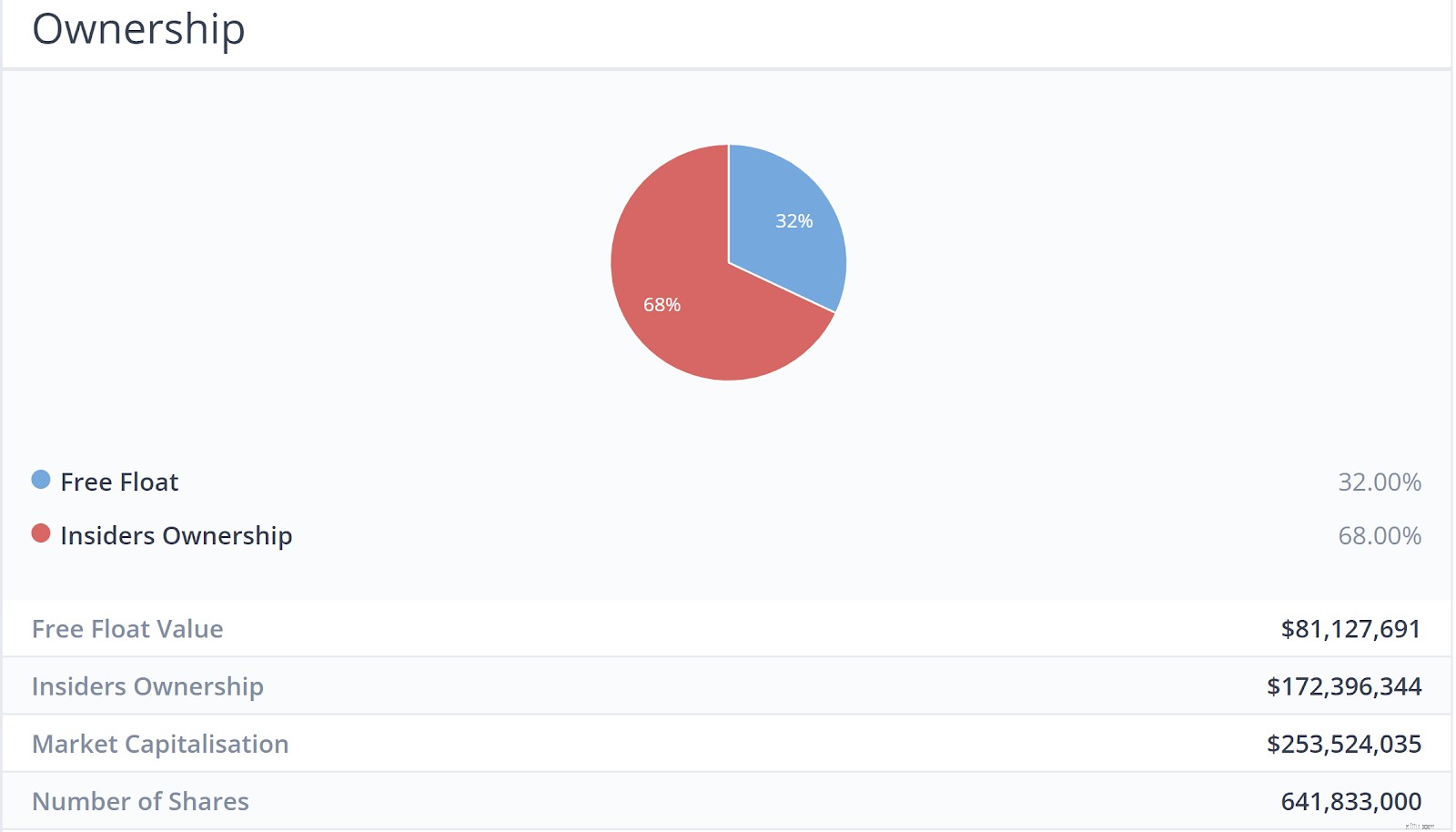

Skin in the Game (Insiders are buying/owning shares)

If the Chairman or the CEO of a company owns more than 50% of shares in the company, their interests are more likely to be more aligned with the shareholders.

That is because they are unlikely to take actions to harm their own wealth and would look towards improving the prospects of the company.

As can be seen, insiders of the company owned a majority of the shareholder-ship. Therefore, it proves that the management has skin in the game.

The Company is buying back Shares

Buying back shares is the simplest and best way a company can reward its investors, according to Peter Lynch.

If it has faith in its own future, then it would invest in itself, just as shareholders do.

Jumbo has been doing just that, posting notices from 31st May – 11th June on their daily share buy-backs.

| Market Cap. | $81M |

| Historical Dividend Yield | 4.27% |

| Not in Sunset Industry | Yes |

| PE Ratio | 24.22 |

| Industry Average PE ratio | 23.8 |

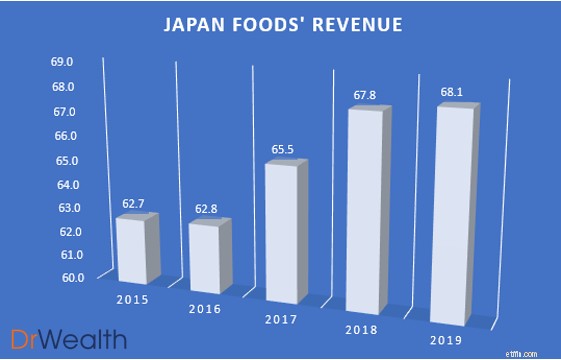

As seen in the chart, Japan Foods’ revenue has been growing year on year, albeit not substantially from 2018 to 2019. However, we would expect the top line to grow with the growth potential lined up for Japan Foods.

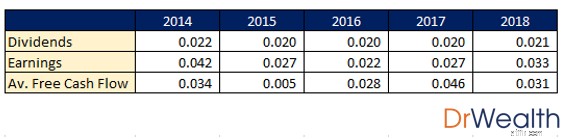

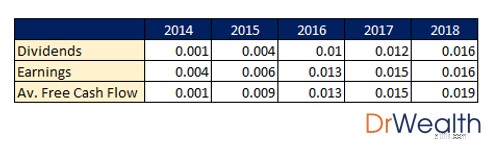

Japan Foods has been distributing consistent dividends for the past 5 years and its earnings and free cash flow has been more than the dividends distributed for all 5 years.

Similar to Jumbo, Japan Foods business growth model focuses on three things:

Japan Foods’ approach moving forward seems logical and sound. Their joint venture under the franchise “Dining Collective” is a great leap forward in their overseas ambitions, allowing them to unlock a larger customer pool by expanding their outlets and having a presence in foreign markets.

They also managed to secure and launch a new franchised ramen brand “Konjiki Hototogisu”, known for its clam-flavoured broth. The restaurant chain also has One Michelin Star.

They have since opened four restaurants under this brand in Singapore, with the latest one being launched in Jewel Changi.

This is definitely not a form of diworseification as Japan Foods aims to tackle the premium market in Singapore whilst maintaining more affordable brands for the general crowd. This caters to the tastes and wallets of the consumers, unlocking more potential for growth.

Lastly, they launched two brand extensions of “Ajisen Ramen”, named “Den by Ajisen Ramen” and “Kara-Men”.

By refreshing and rejuvenating brands, it allows Japan Foods to remain competitive and relevant in the market. To date, the response to the two variations has indeed been well with an increase in same-store sales following the rebranding.

It’s got a Niche

Lynch found that if a company focused on a particular niche, it often had little competition. Japan Foods is one of the leading F&B groups in Singapore specializing in Japanese cuisine. With 19 Dining Brands under their name and 50 locations islandwide, it seems that their restaurant network is stable and well-built.

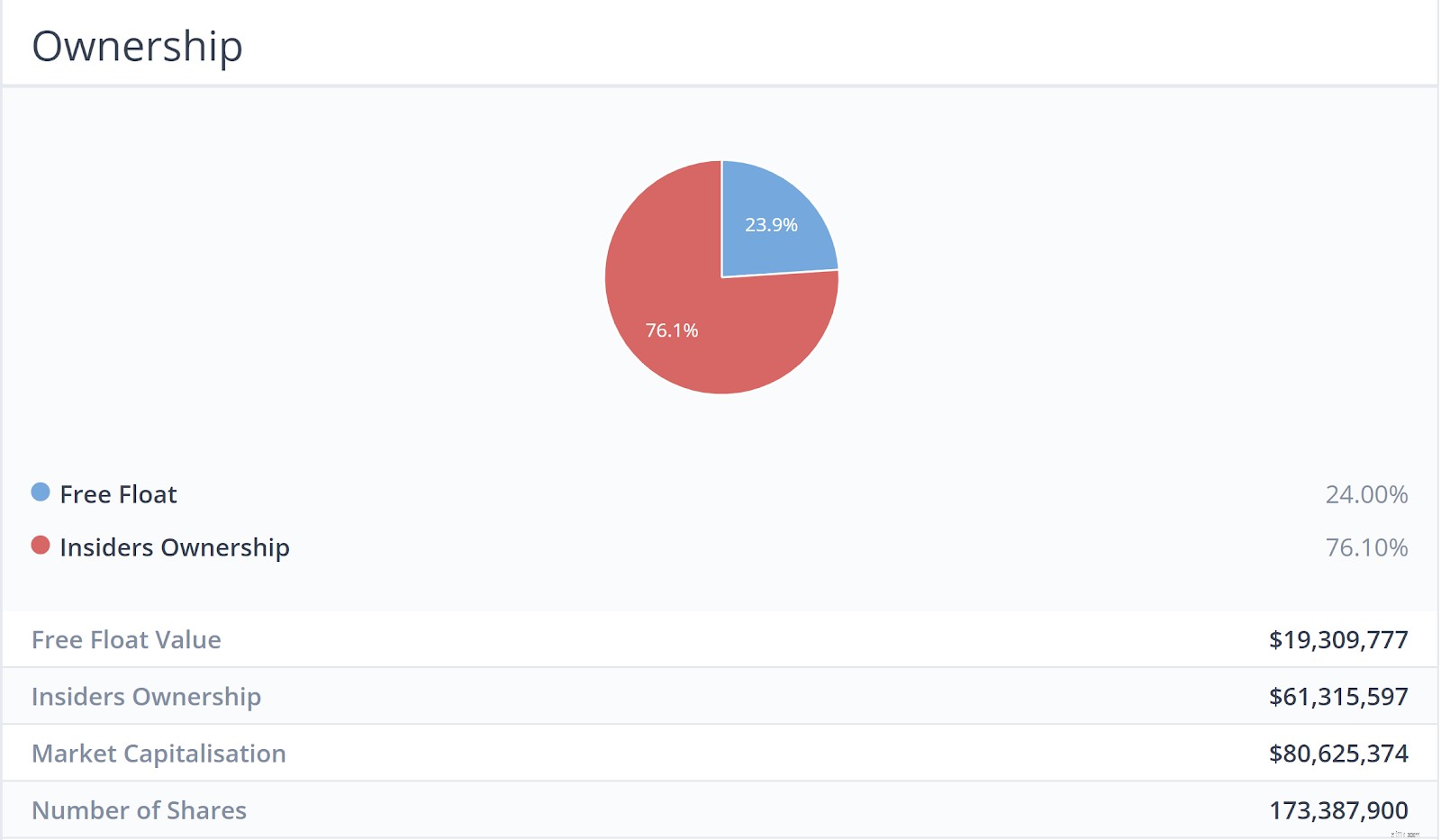

Skin in the Game (Insiders are buying/owning shares)

As can be seen, insiders of the company owned a majority of the shareholder-ship. Therefore, it proves that the management has skin in the game.

The Company is buying back shares

Japan Foods has also been posting notices in Aug 2018, Sep 2018, Dec 2018 and Feb 2018 on its daily share buybacks. Such notices can either be found on the SGX website or their investor relations website.

| Market Cap. | $186M |

| Historical Dividend Yield | 6.12% |

| Not in Sunset Industry | Yes |

| PE Ratio | 21.53 |

| Industry Average PE ratio | 47.95 |

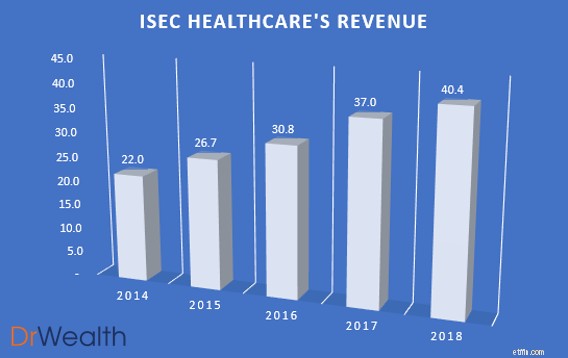

As seen in the chart, ISEC’s revenue has been growing year on year with a 9.19% growth from $37m in 2017 to $40.4M in 2018. We would also potentially expect the revenue growth to increase due to the region’s aging population and increasing awareness towards seeking early treatment for ophthalmology issues will continue to drive demand and sales upwards.

ISEC Healthcare has been distributing consistent increasing dividends for the past 5 years and its earnings and free cash flow has been more than or equal to the dividends distributed for all years.

We see growth potential in ISEC Healthcare’s business due to 3 key reasons:

Due to ageing populations, requirements for eye health care will increase. This is because there are higher incidences of Cataract, Glaucoma, Age Macular Degeneration, Dry Eyes and Vitreoretinal.

Furthermore, not only is government spending on healthcare services increasing across the region in line with changes in demographics, rising income levels and subsequent private insurance coverages has led to an increase in individual spending on private eye-care services.

ISEC Healthcare is also keen on regional expansions with large populations. They took a positive step towards this direction by announcing the incorporation of ISEC MYANMAR. They are also keen on leveraging upon the aforementioned trends to continue pursuing investment opportunities and explore up-and-coming markets such as China, Indonesia and Vietnam.

It’s got a Niche

In terms of devising a business strategy, a niche company can remain focused on its area of specialization. Over time, a niche company can develop a reputation for its work in a given field. This reputation allows a niche company to position itself as a leader and expert in the field. Niche companies focus on doing one thing well rather than doing many things only adequately. ISEC Healthcare definitely has an Eye Specialist Niche. This gives it better margins as a specialist clinic than a generalist.

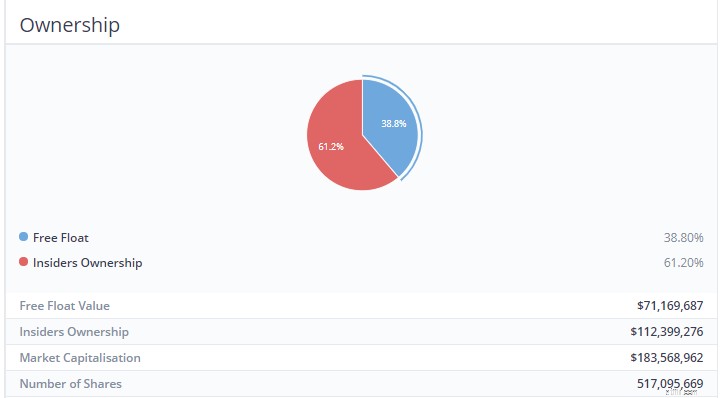

Skin in the Game (Insiders are buying/owning shares)

As can be seen, insiders of the company owned a majority of the shareholder-ship. Therefore, it proves that the management has skin in the game.

Not many Institutions own it

Peter Lynch states that if you find a stock with little or no institutional ownership, you’ve found a potential winner. Such companies have not been discovered by the smart money, giving it an extra potential upside.

So there you have it. The Stalwart Category explained in accordance with Peter Lynch’s guidebook.

Lynch expected stalwarts to deliver gains of 30% to 50%, after which he would sell them and find new, undervalued counters. These are the stocks that he would frequently replace with others in this category.

Next, we’re going in-depth into one of the six different categories pointed out by Lynch – The Fast Growers

These counters are among Lynch’s favourite investment. These stocks typically have the characteristics of small, aggressive new enterprises that grow at 20-25% a year. Lynch claims that if you were to choose these Fast Growers correctly, it could potentially be a 10 to 40 bagger.

We would be picking stocks utilizing the following criteria to select our Top 3 Fast Growers:

To elaborate a little further on the above criteria:

At Dr Wealth, we believe that the Singapore Stock Exchange Market is more catered towards investors with the strategy of earning a passive income. Thus, while SGX is a fantastic market for dividend stocks/REITs there are much better growth stocks available beyond SGX.

We would, therefore, apply the aforementioned criteria in the US markets as we feel that growth stocks are aplenty there.

Given the above criteria, we shortlisted 3 Fast Growers that we will cover today, which we feel have significant growth potential. In addition, all of the stocks will have one or more of the following traits of a ten-bagger, representing a potential return 10X of what you invested.

| Market Cap. | $11.62B |

| Debt-to-Equity Ratio | 18.54 |

| Stable Top &Bottom Line Y-O-Y | Yes |

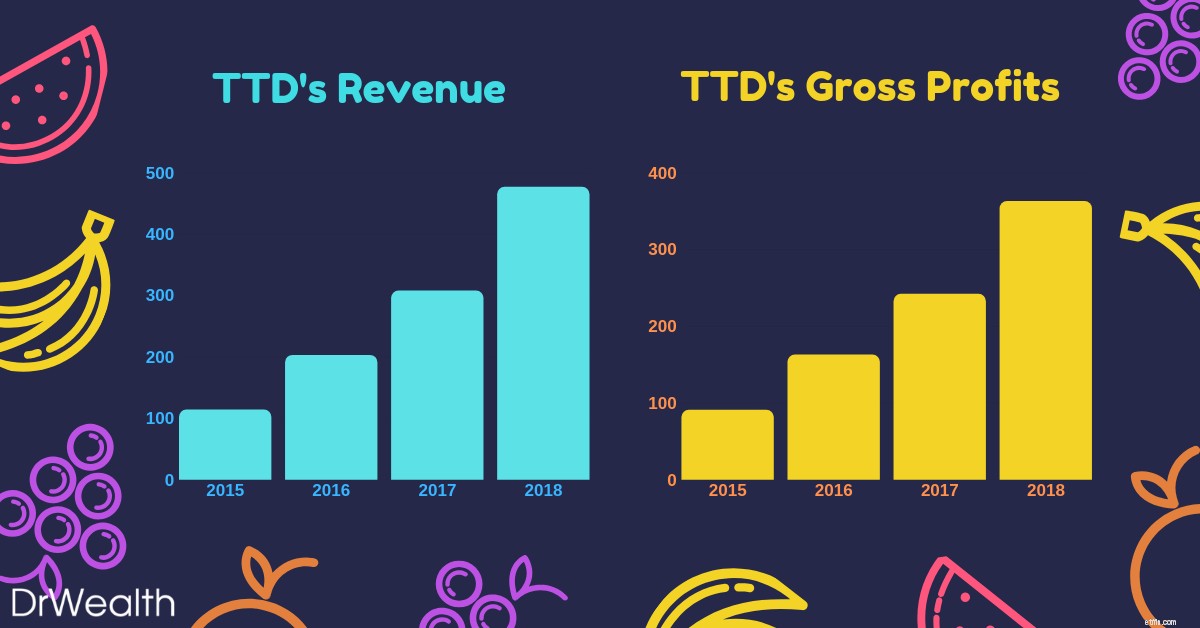

As seen in the graph, The Trade Desk’s earnings have been growing year-on-year from 2015 to 2018. Earnings grew from $242M in 2017 to $363M in 2018, displaying a whopping 50.1% growth versus the prior year.

We would also potentially expect the earnings growth to maintain or even increase as The Trade Desk looks towards gaining a firmer foothold in China and other regions.

What does The Trade Desk do?

Do you realize that what you have searched on Google would start popping up in your Facebook/Instagram/Youtube feeds as adverts?

Eerily, most of the adverts are also very relevant to what you are interested in. Welcome to the world of Programmatic Advertising!

The Trade Desk is essentially a programmatic advertising company which operates a cloud-based platform that lets companies streamline their efforts to the apt consumer’s groups they are targeting.

This, in turn, cuts down the advertising expenditure of the company and allows it to achieve a greater ROI with its adverts.

TTD allows its customers to buy targeted ad space on many different channels like social media, video/streaming, audio and many more.

The Trade Desk’s Growth Potential

Jeff Green, chief executive officer and founder of The Trade Desk, sees China as an untapped market.

This strategic move was solidified with its launch in China earlier this year, inking deals with tech powerhouses such as Alibaba, Baidu and Tencent.

Thus far, companies such as Sheraton Hotels have successfully utilized the platform to expand their customer base greatly through its targeted advertisements.

In the next five years, CEO Jeff Green claims that The Trade Desk plans to turn China into one of its top three markets.

The company says international revenue currently accounts for about 15% in revenue but expects it to grow to roughly two-thirds of its total revenue as the programmatic industry matures.

For investors, this means that there is still huge untapped potential for The Trade Desk to grow as it would take awhile for one to see material contributions from the China market to its top &bottom lines.

With the company already growing at such a blistering pace Y-O-Y without tapping on China, one would potentially expect their growth to sustain or even increase in the future.

With earnings growth, this would inevitably lead to greater appreciation in stock prices, thus allowing the investor to potentially attain a multi-bagger.

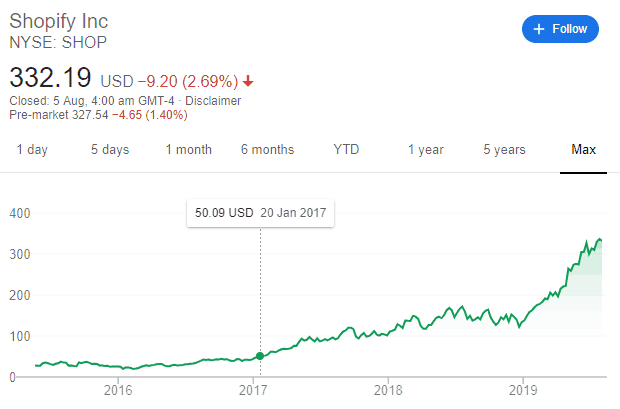

| Market Cap. | $37.38B |

| Debt-to-Equity Ratio | 5.3 |

| Stable Top &Bottom Line Y-O-Y | Yes |

As seen in the graph, Shopify’s earnings have been growing year-on-year from 2015 to 2018. Earnings grew from $380M in 2017 to $596M in 2018, displaying a huge 56.8% growth versus the prior year.

Shopify has secured its status as the e-commerce platform of choice for small entrepreneurs. Its client base and gross merchandise volume are both growing explosively.

As of June 2019, there are 820,000 Merchants from Shopify growing 55% from the prior year.

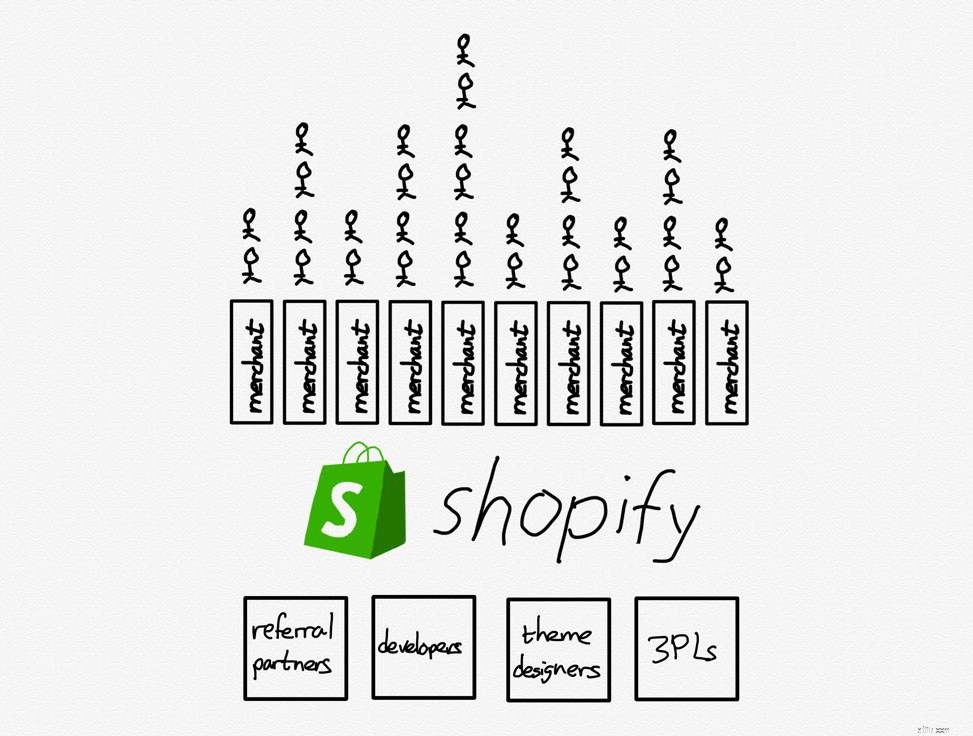

What does Shopify do?

Shopify is an e-commerce platform that allows merchants of all sizes to “set up” their own stores online. They all provide a suite of advantages such as fulfilment, payment and shipping services.

Shopify’s winning formula includes its platform’s ability to give online merchants an easy way to handle many aspects of their business:inventory management, fulfilling orders, processing payments, and communicating with current and prospective customers alike.

It is also extremely flexible with its ability to be connected with sites such as Ebay and social media such as Instagram. Small and medium-sized businesses still make up the core of Shopify’s clientele.

However, the company also offers a $2,000 a month Shopify Plus package for bigger businesses which the likes of Nestle and Red Bull utilize.

Shopify’s Growth Potential

The company estimates that there are 46 million small and mid-sized businesses around the world, and it’s only serving 1.3% of them. That leaves plenty of opportunities for Shopify to keep growing well into the future.

With the advent of the switch from traditional/physical shopping to online commerce, Shopify’s addressable market continues to grow as e-commerce captures a larger share of overall shopping.

Furthermore, one should note that Shopify isn’t a competitor to Amazon.

Amazon is an aggregator who internalises suppliers (people think they buy from amazon but actually make purchases from other suppliers).

Shopify as a platform externalises suppliers (people buy from various brands without knowing shopify powers them). There is nothing to purchase on Shopify.com other than its suite of platforms, unlike Amazon.

TLDR, Amazon is pursuing customers and bringing suppliers and merchants onto its platform on its own terms. Shopify is giving merchants an opportunity to differentiate themselves while bearing no risk if they fail.

The only way to beat an aggregator is to be a platform that externalise suppliers with differentiation.

For investors, this is a great business model which is still helmed by its charismatic and visionary founder, Tobi Lutke. In the long run, Shopify could potentially continue dominating the market and growing at a blistering pace.

With a huge untapped addressable consumer market and large growth capacities, Shopify as a fast grower could turn into one of the legendary Lynch Multi-Baggers.

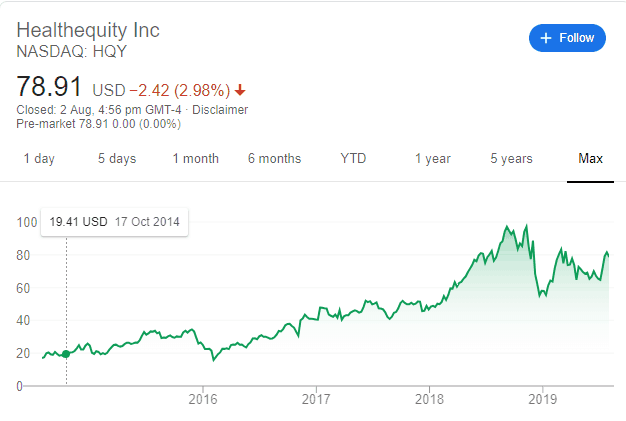

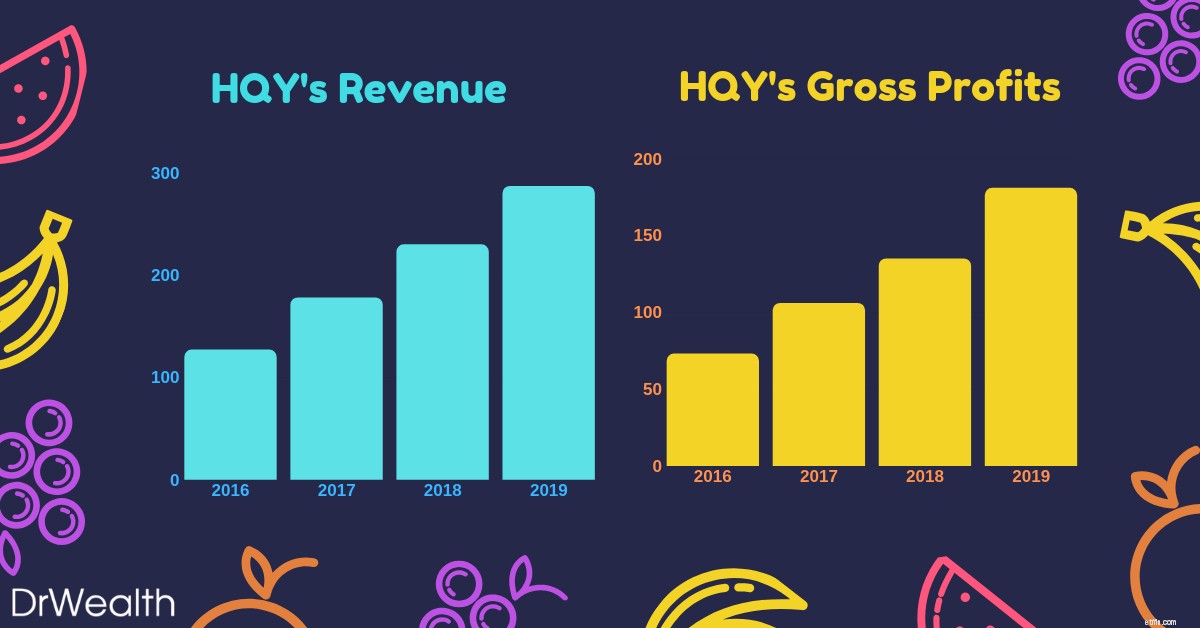

| Market Cap. | $4.95B |

| Debt-to-Equity Ratio | 7.56 |

| Stable Top &Bottom Line Y-O-Y | Yes |

As seen in the graph, Health Equity’s earnings have been growing year-on-year from 2016 to 2019. Earnings grew from $135M in 2018 to $181M in 2019, displaying a 34% growth versus the prior year.

HealthEquity is not only profitable but has also seen impressive profit growth to go with rising sales in recent years.It’s identified multiple pathways toward future expansion that includes both organic growth and potential strategic transactions.

What does Health Equity do?

Health Equity is a cloud-based platform that provides access to Health Savings Accounts (HSAs) and other health-care benefits.

HSAs were implemented by the US Federal Government in 2003. It allows one to set aside cash for certain healthcare expenses that are not covered by their insurance.

HSAs come with huge tax benefits:money placed inside of HSAs are tax-deductible, and investments inside the HSA grow on a tax-deferred basis.

Additionally, withdrawals from HSAs aren’t taxed as long as the money is used to cover qualified healthcare expenses.

They help employers and employees alike to save on healthcare costs while taking advantage of tax incentives provided.

Health Equity’s growth potential

Health Equity’s business model is also simple:

With recurring revenue and simple services, Health Equity is definitely in it for the long run.

Furthermore, its founder, Stephen Neeleman was one of the doctors that lobbied for the federal government to implement HSAs and then subsequently built the platform, Health Equity to trade the accounts.

Rising Health Care costs will definitely be a huge proponent that drives up the demand for Health Equity services and products.

As the number of discerning healthcare consumers expands exponentially, interest in Health Savings accounts and highly deductible savings plans will rise in tandem.

For investors, the rising number of consumers being aware of Health Savings Accounts will drive demand for Health Equity’s platform. This would subsequently propel top-line sales and in turn, earnings.

With Earnings growth comes appreciation in stock prices.

So there you have it. The Fast Growers Category explained in accordance with Peter Lynch’s guidebook. If you choose wisely, this is the land of the 10-40 baggers and even the 200 baggers. However, Lynch reminds us that there’s plenty of risk in fast growers, especially in the younger companies that tend to be overzealous and underfinanced.

The stock market also does not look too kindly fast growers that run out of steam and turn in to slow growers. Hence, it is essential to figure out when the company is going to stop growing (lack of future plans, depreciating financials and loss of key leadership).

As one would notice, Peter Lynch identifies a stock using Qualitative Analysis before diving into the Quantitative.

That means he looks at a stock’s story before he looks at a stock’s business. There is nothing inherently wrong with that.

Whether you approach it from the numbers angle or the story, both ways work. However, we would advise retail investors to focus on approaching stock investing from the quantitative side of things.

This is to avoid biases and to avoid falling in love with a stock’s story. To hunt growth stocks, we have developed a robust, evidence-based framework that has delivered stellar returns per year historically. You can join us at a live session to learn more.

Next, we would be going in-depth into one of the six different categories pointed out by Lynch – The Asset Plays

Asset Plays are stocks that are believed by investors to be undervalued because the current price does not reflect the current value of the company’s assets displayed on its balance sheet.

The rationale for purchasing the stock is that the company’s assets are being offered to the market relatively cheaply, making it attractive to investors.

It would be sort of like buying a house for $0.40 on the $1.

Investors who utilize this strategy believe that the market overreacts, resulting in stock price movements that do not correspond with a company’s long-term fundamentals, giving an opportunity to profit when the price is deflated.

In fact, here at Dr Wealth, we employ our Conservative Net Asset Valuation (CNAV) method to identify to evaluate and select deeply undervalued Asset Plays.

We provide “Skin in the Game” case studies of our winning stocks that were hand-picked using our proprietary CNAV screener, substantiating them with past transaction statements.

We would thus be picking stocks utilizing the following criteria to select our Top 3 Asset Plays:

To elaborate a little further on the above criteria:

This is the formula we use to calculate a stock’s Conservative Net Asset Value:

All of which can be found in the Balance Sheet of the company’s financial statements.

We would then take the CNAV2 value, divided by total shares outstanding to find the CNAV2 per-share value .

Thus, if the CNAV2 per-share value is HIGHER than that of the current price per share, it is deemed to be on a discount.

To make our selection more stringent, we turn to Dr Joseph Piotroski’s F-score to find fundamentally strong low price-to-book stocks that are worth investing in.

As we have already added conservativeness, we do not need to adopt the full 9-point F-score. A proxy 3-point system known as POF score would be used instead.

It stands for Profitability , Operating Efficiency and Financial Position .

The stocks selected has to have a POF score of 2 and above.

To learn more about the POF score and how we use it in our investment strategies, click here.

An easy way to bypass such subjective questions is to look at whether management owns the majority of the shares in the company.

Today, we would be looking at the Hong Kong Stock Exchange market due to the recent correction caused by the protests. This resulted in many counters being ‘On-Sale’ even though its fundamentals have not faced any drastic changes.

To facilitate your reading, we have structured the content into clear and concise points to sum up what you have to know:

While there isn’t a hard and fast exit strategy, at Dr Wealth we would either sell at the 3 year holding period , when the Financial Fundamentals change or when a key qualitative point has been changed (i.e. change of CEO/founder steps down).

| Market Cap. | $1.173B |

| Market Price | $0.173HKD |

| CNAV2 Value per share | $0.386HKD |

| Net Asset Value per share | $0.659HKD |

| POF score | 3 |

| Potential Profit | 281% |

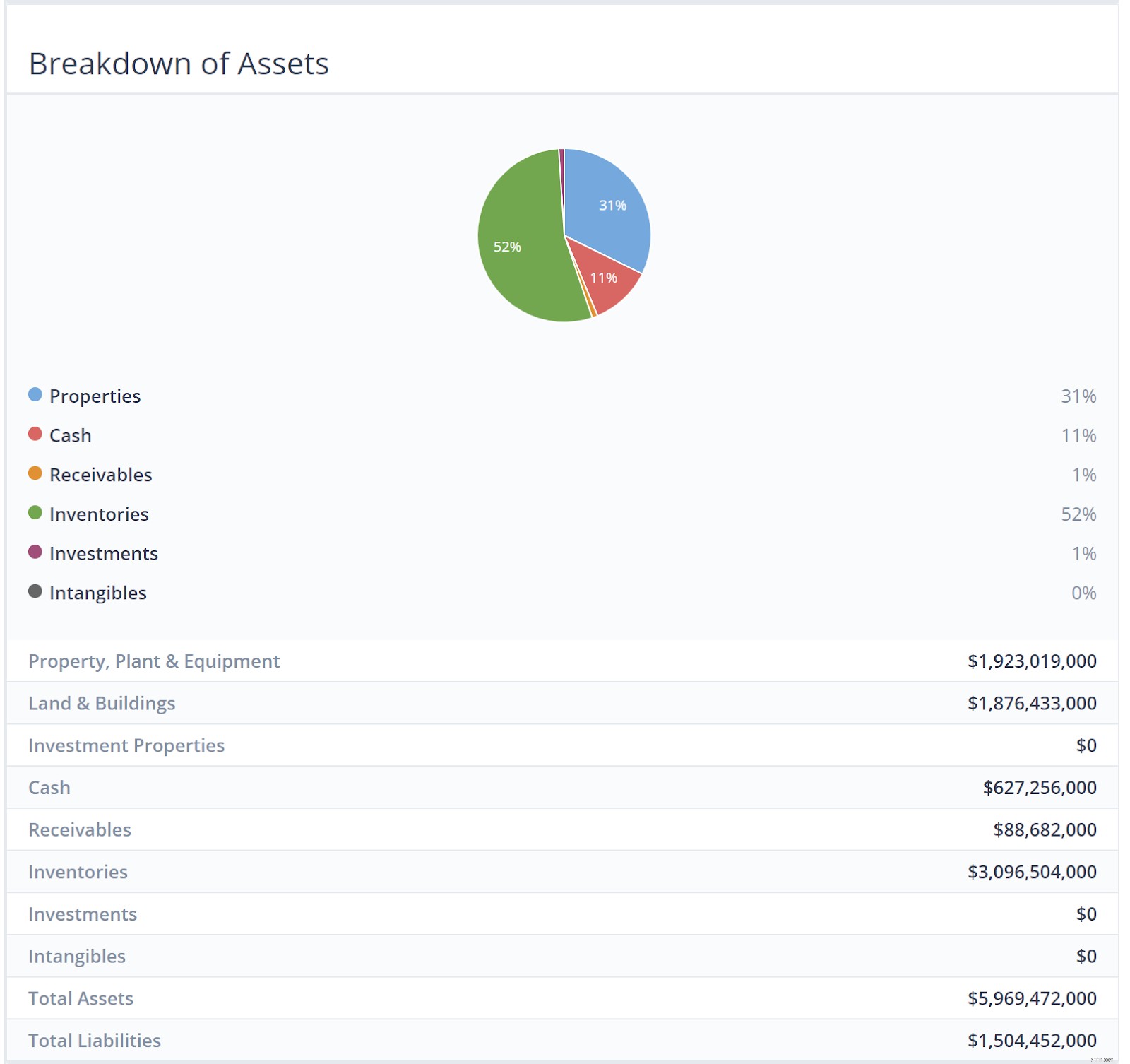

Emperor Watch &Jewellery is a retailer of European-made internationally renowned watches such as Patek Philippe, Rolex and Tudor. This is coupled with the sales of self-designed fine jewellery under its own brand, ‘Emperor Jewellery’.

The company has a history of over 75 years, establishing over 90 stores across Hong Kong, Macau, mainland China, Singapore and Malaysia, as well as an online shopping platform, and now has over 1,100 staff.

As seen in the infographic above, Inventories and Properties make up the bulk of their assets. There is a whopping HK$3.09 billion worth of luxury watches and Jewellery.

My hypothesis was that it wouldn’t be that bad because luxury watches and jewellery retain value pretty well as long as they are not worn and still in good condition.

We went ahead to discount the current inventory of watches and jewellery at 50%. We should account for a large margin of safety when calculating the valuation of Emperor Watch &Jewellery.

The Company’s core strategy focuses on maintaining its position as the leading watch and jewellery retailing group in Greater China, coupled with an eye on expansion beyond the region.

As most of their customers are mainlanders, boutique stores that peddled luxury goods such as watches and jewellery enjoyed the patronage of this swell of new customers as a result.

However, most of this all came to a halt when President Xi Jing Ping decided to rein in on the corruption.

This discouraged ostentatious displays of wealth in public. Sales of luxury goods to Chinese consumers slowed for a time and as earnings dropped, so did share prices.

Coupled with the recent 10 straight weeks of anti-government protests in Hong Kong, stock prices in the HK Exchange have inevitably taken a massive beating. This is without even mentioning the massive backdrop created by the Trump-China trade war affecting prices as well!

More than $600 billion of stock market value has been erased since early July thanks to the riots and protests.

The culmination of all these events have thus done something favourable for us; create opportunities for us to businesses at fantastic bargain prices.

| Market Cap. | $97.101B |

| Market Price | $47.4HKD |

| CNAV2 Value per share | $68.357HKD |

| Net Asset Value per share | $105.846HKD |

| POF score | 3 |

| Potential Profit | 121% |

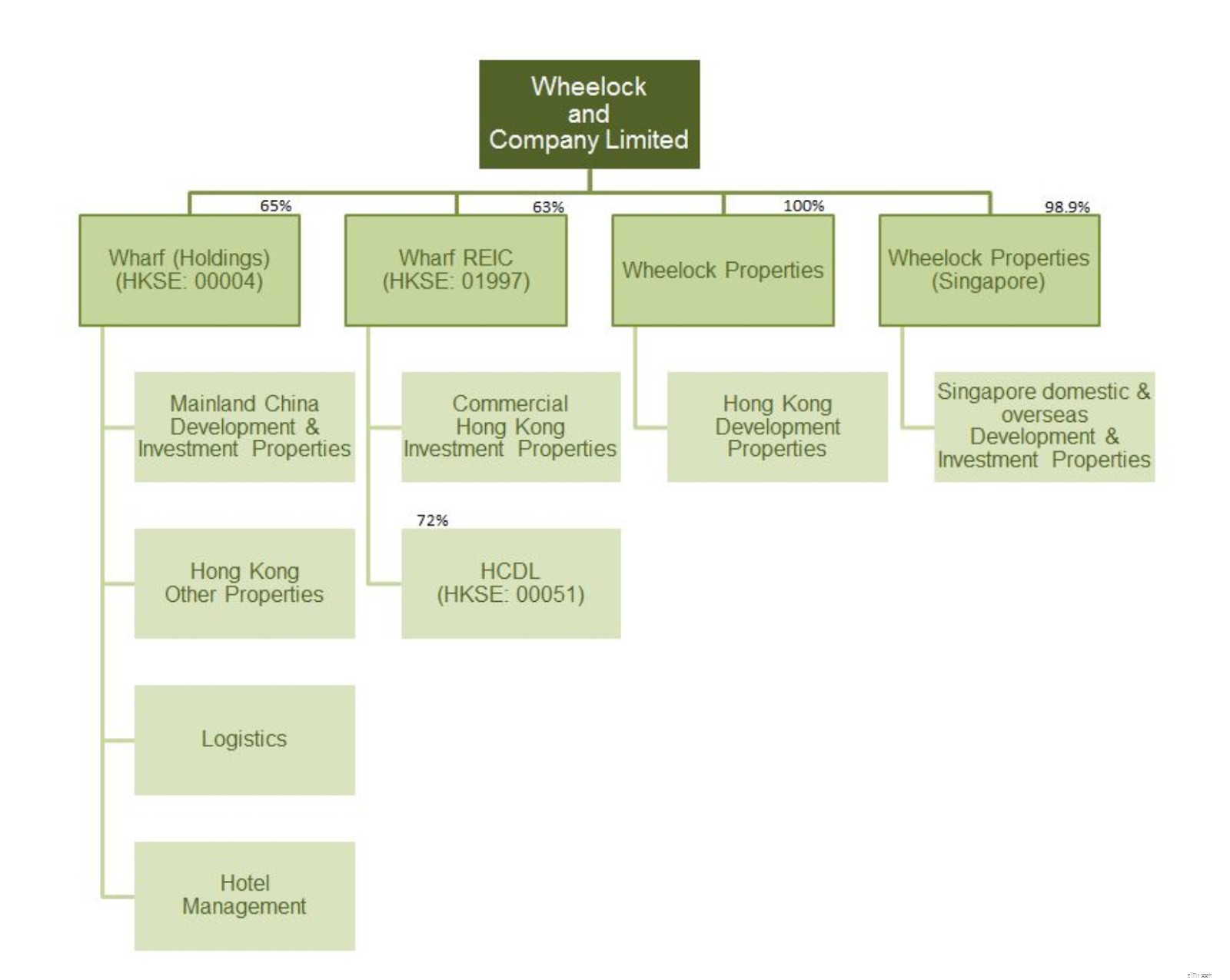

Wheelock &Co. is principally engaged in property development in Hong Kong, and in property investment and development in Singapore.

Their major subsidiaries include Wharf (Holdings) Limited (HKSE:00004), Wharf REIC Limited (HKSE:01997), Wheelock Properties Limited and Wheelock Properties (Singapore) Limited.

As seen in the infographic above, Properties make up the bulk of their assets. This should be rightfully so as they are engaged in the property development business.

Due to the sheer amount of properties available in the company, we would only touch on the assets of Wheelock Properties here.

Kindly refer to the company’s website should you like to find out more about its other major subsidiaries asset breakdown.

| Market Cap. | $2.48B |

| Market Price | $4.69HKD |

| CNAV2 Value per share | $15.067HKD |

| Net Asset Value per share | $24.966HKD |

| POF score | 3 |

| Potential Profit | 420% |

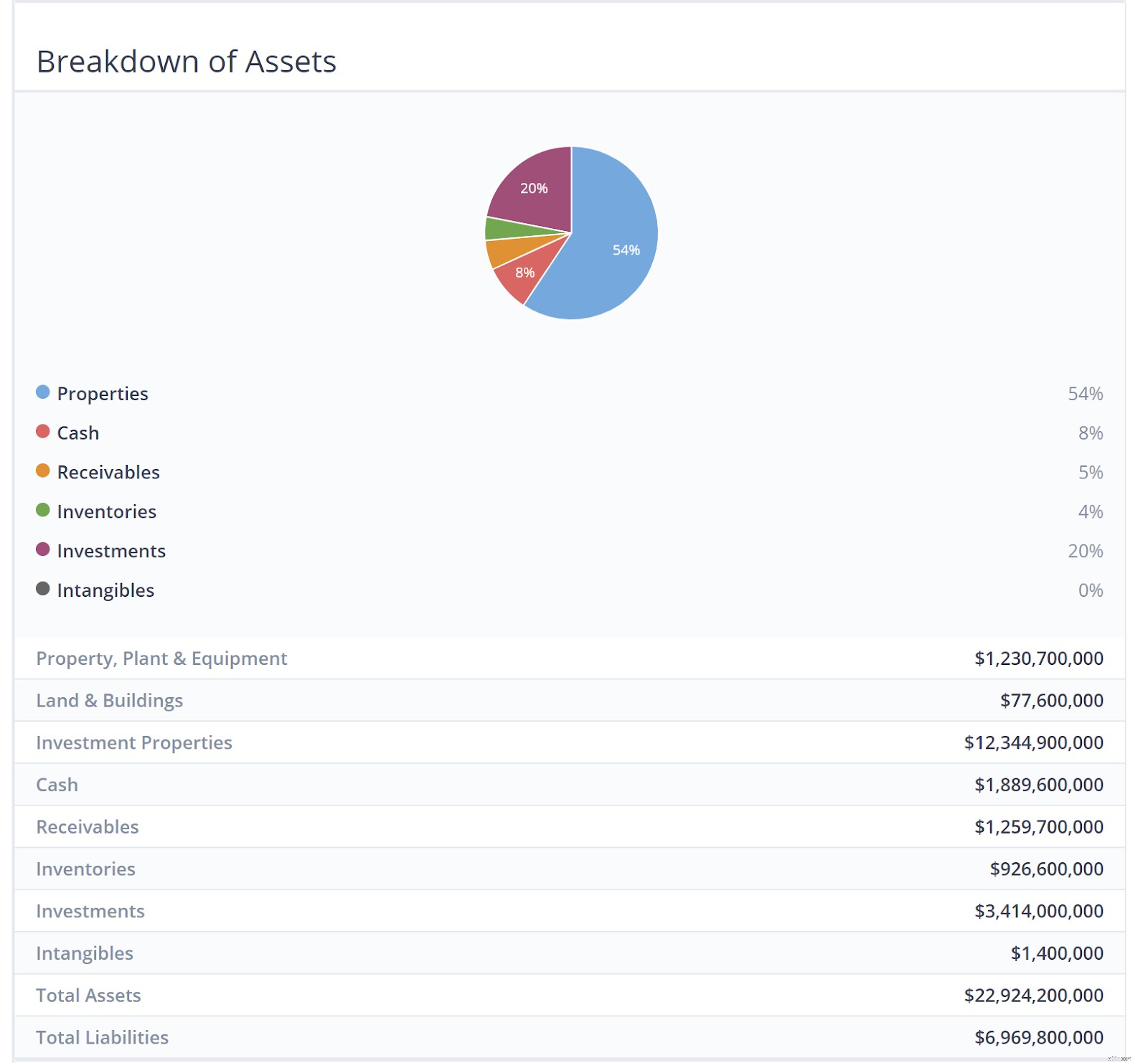

The Group is a Hong Kong-based property developer focusing on investing and developing property projects in Mainland China and aims to develop high-quality products to create sustainable value for its shareholders.

The Group has a diversified property portfolio model with investments in both residential projects for sale and commercial projects mainly for rental income.

The group is organized into 3 main operating segments:

Over the long term, the Group seeks to maintain a balance between residential development for sale and commercial investment properties for lease in order to create a sustainable model with growth potential.

Residential properties for sale generate fast turnover, which should enhance return on equity. Investment properties for lease, on the other hand, create steady recurring income and cash flow as well as long term capital appreciation and are relatively immune from the periodic restrictions on residential properties.

The Group has also made an investment in the renewable energy sector and believes shareholders may benefit from China’s need to develop non-polluting sources of energy.

As seen in the infographic above, similar to Wheelock &Co, Properties make up the bulk of their assets. This should be rightfully so once again as they are engaged in the property development business.

The assets are mostly located around the more developed, coastal regions of China – where population density and income levels are much higher.

This could largely be attributed to the slowdown of the Chinese property sector in 2018. China’s massive property market is expected to cool further in 2019, with smaller price rises and falling home sales adding to pressure on the world’s second-largest economy, a Reuters poll showed.

As a result, residential sales volume began declining in the second half of 2018, with declines of 1% year on year in September and October and 4% in November. It increased by 2.5% in December, but poor Chinese New Year’s data suggest that the decline will continue into 2019.

Moreover, the price rise growth for new residential properties has decelerated for the third straight month. In January, residential prices for 70 major cities increased by only 0.61% compared to December, the slowest pace in nine months.