신용 카드는 미국 어디에서나 볼 수 있으며 재정 자문 고객은 지갑에 적어도 하나는 가지고 있을 것입니다. 그리고 많은 소비자가 보유하고 있는 신용 카드로 얻는 보상에 대해 알고 있지만 모르거나 보상을 극대화할 수 있는 기회를 알고 있습니다. 사실, 신용 카드 가입과 정기적인 지출의 조합을 통해 개인은 매년 수천 달러의 캐쉬백 보상이나 여행 혜택을 받을 수 있습니다. 따라서 재정 고문은 고객이 개인 지출 습관에 따라 보상을 극대화할 수 있는 최고의 카드를 찾도록 돕는 데 노력을 투자함으로써 고객에게 상당한 지속적인 가치를 제공할 수 있는 기회를 갖게 됩니다.

신용 카드 보상은 캐시백, 여행 포인트/마일리지, 일반적으로 현금 또는 여행에 사용할 수 있는 양도 가능한 포인트의 세 가지 유형이 있습니다. 이들 각각은 다양한 유형의 클라이언트에 적합할 수 있습니다. 예를 들어, 단순함을 갈망하거나 여행에 거의 관심이 없는 고객은 캐시백 보상이 가장 유용할 수 있습니다. 이코노미 클래스 항공권에 익숙하고 비즈니스 또는 퍼스트 클래스 비행만을 꿈꾸는 다른 고객들은 여행 신용 카드 보상을 최대화하여 다른 방법으로는 얻을 수 없는 경험을 하고 싶을 수도 있습니다!

리워드는 가입 보너스와 카드로 정기적인 지출을 통해 얻을 수 있습니다. 신용 카드 가입 보너스(카드당 현금 또는 여행 경비로 $1,000 이상 가치가 있을 수 있음)는 보상을 받는 가장 빠른 방법이며 일반적으로 주어진 기간 동안 특정 금액을 지출한 경우 보너스를 제공합니다. 일반 지출의 경우 신용 카드는 카드 지출에 대해 고정 요율(예:모든 지출 범주에 대해 2% 캐시백) 또는 특정 지출 범주에 따라 변동 요율(예:1달러당 4% 캐시백)을 제공합니다. 여행에 지출하거나 레스토랑에서 지출한 1달러당 3% 캐시백).

고문의 경우 고객과의 현금 흐름에 대한 논의는 적절한 신용 카드 보상 프로그램을 소개하는 좋은 기회가 될 수 있습니다. 고문은 무엇을 고객이 구매하는 것뿐만 아니라 어떻게 그들은 그 구매에 대해 지불하고 있습니다. 이는 고객의 정기적인 신용 카드 지출(가입 보너스에 대한 지출 요건 충족 능력 측정), 구매 범주(예:식료품, 주유) 가장 자주(이 범주에서 보너스 보상을 제공하는 카드를 찾기 위해), 대규모 일회성 비용(가입 보너스 지출 요건을 스스로 충족하는 데 사용할 수 있음)을 계획하고 있는지 여부.

고객의 지출 패턴을 이해하는 것 외에도 신용 카드 보상을 지속적으로 관리하는 데 대한 고객의 관심을 측정하는 것도 중요합니다. 일부 고객은 가입 보너스를 통해 포인트와 마일을 적립하기 위해 매년 여러 장의 새 카드를 신청하는 데 관심이 있을 수 있지만 다른 고객은 카드 신청에 관심이 없고 대신 단일 카드로 보상을 받는 것을 선호할 수 있습니다. 두 옵션 모두 고객에게 이익이 될 수 있으므로 고객이 프로세스에 익숙해지는 것이 중요합니다(고객이 고정하기 쉽도록 우선 전략에!).

궁극적으로 요점은 고객과 협력하여 사용 가능한 보상을 최대화하는 신용 카드 지출 전략을 고안하면 어드바이저가 고객을 유치하고 유지하기 위한 지속적인 가치를 입증하는 데 도움이 될 수 있다는 것입니다. 왜냐하면 결국 고객이 하지 않을 매년 '무료' 휴가를 보낼 수 있도록 도와줄 수 있는 고문과 함께 일하고 싶으십니까?

Adam은 Kitces.com의 재무 계획 준회원입니다. 그는 이전에 메릴랜드주 베데스다에 있는 재무 기획 회사에서 은행 및 보험 산업을 다루는 기자로 일했습니다. 직장 밖에서 그는 북부 버지니아 지역의 비영리 자원 봉사 재정 기획자이자 수업 강사로 일하고 있습니다. Johns Hopkins University에서 석사 학위를, University of Virginia에서 학사 학위를 받았습니다.

현금 흐름 분석은 고문과 그 고객을 위한 재무 계획 프로세스의 기본적인 부분이므로 고객의 모든 수입원과 지출을 이해하고 미래에 이러한 요소에 대한 현실적인 변화를 예측할 수 있는 것은 의미 있는 계획하고 제안합니다. 그러나 재무 계획 프로세스의 일부는 얼마나 고객이 지출하고 있는 무엇을 그들은 구매하고 있지만 반드시 어떻게 그들은 그러한 구매를 하고 있으며 소비 습관이 더 효율적일 수 있는지 여부를 확인합니다.

일부 고객은 신용 카드 보상의 가치를 극대화하여 현금, 무보상 직불 카드 또는 종이 수표(!)와 같이 지출에 대한 보상 측면에서 거의 제공하지 않는 방법을 사용할 수 있지만 고객은 실제로 수천 달러를 벌 수 있습니다. 매년 정기적으로 지출하는 1달러 상당의 현금 또는 여행!

신용 카드 보상을 최대화하려면 주어진 개인에게 가장 적합한 카드를 결정하는 데 약간의 노력이 필요하지만, 고객이 그렇게 하도록 돕는 재정 고문은 그럼에도 불구하고 고객에게 상당한 지속적인 가치를 제공하고 신용 카드로 지출을 최적화하도록 지원함으로써 충성도를 높일 수 있습니다. 지출 및 보상 전략. 결국, 어떤 고객이 매년 수천 달러를 벌거나 심지어 유럽이나 하와이로 무료 여행을 가는 데 도움을 주는 고문과 일하고 싶어하지 않겠습니까!

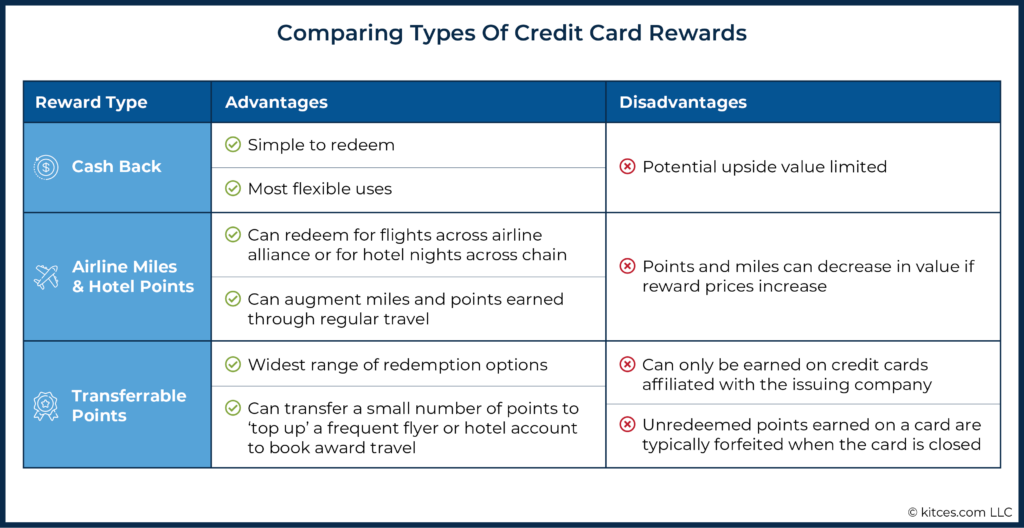

고객이 신용 카드 보상을 최적화할 수 있도록 지원하는 첫 번째 단계는 다양한 유형의 보상과 지급 방식을 이해하는 것입니다. 신용 카드 보상은 세 가지 기본 그룹으로 분류할 수 있습니다. 1) 캐시백; 2) 항공권 또는 호텔 숙박에 사용할 수 있는 전용 여행 포인트 3) 현금, 항공사 마일리지, 호텔 포인트로 전환하거나 기타 보상에 사용할 수 있는 양도 가능한 포인트입니다.

세 가지 유형의 신용 카드 보상은 각각 장단점이 있으며 주어진 개인에게 가장 좋은 유형의 보상은 주로 현금 환급 또는 여행에 대한 선호도에 따라 다릅니다.

가장 간단한 유형의 신용 카드 보상은 카드 구매에 대한 캐시백입니다. 예를 들어, 카드는 사용자의 월별 명세서에 크레딧으로 사용하거나 은행 계좌에 입금할 수 있는 구매에 대해 2% 캐시백을 제공할 수 있습니다.

캐시백 보상의 주요 이점은 사용자가 보상의 가치와 지출 요구 사항에 대해 사용할 수 있는 금액을 정확히 알고 있기 때문에 단순성과 대체 가능성입니다. 일을 단순하게 유지하려는 고객에게는 캐쉬백을 받는 것이 좋은 선택이 될 수 있습니다. 반면, 보상의 상방 가치는 받은 캐시백으로 제한되는 반면, 다른 유형의 보상은 사용 방법에 따라 훨씬 더 큰 가치를 가질 수 있습니다.

신용 카드 보상의 또 다른 유형은 특정 항공사 또는 호텔 회사의 로열티 프로그램에 대해 적립되는 포인트 및 마일입니다. 대부분의 여행 제공업체는 서비스 사용자에게 상용 고객 마일 또는 여행에 사용할 수 있는 포인트를 보상하고 항공사를 이용하거나 호텔에 숙박할 때 업그레이드 및 기타 서비스 특전을 제공하는 로열티 프로그램을 제공합니다.

이러한 로열티 프로그램은 여행 제공업체에 매우 수익성이 높지만 여행자에게도 상당한 혜택을 제공합니다. 여행을 통해 마일과 포인트를 적립하는 것 외에도 많은 항공사와 호텔은 소비자가 추가 마일을 적립하는 데 사용할 수 있는 공동 브랜드 신용 카드를 제공합니다. 예를 들어, 항공사 신용 카드는 카드에 지출한 1달러당 상용 고객 마일리지 1마일을 제공할 수 있습니다. 신용 카드 사용을 통해 상용 고객 마일과 호텔 포인트를 적립하는 것은 소비자가 이미 사용하고 있는 항공사나 호텔의 마일이나 포인트를 늘리는 좋은 방법이 될 수 있으며 항공편이나 호텔 숙박에 대한 사용은 종종 동등한 것보다 훨씬 더 가치가 있을 수 있습니다. 다른 카드에서 생성할 수 있는 캐쉬백. 단점으로는 항공사와 호텔이 특정 항공편이나 호텔에 대해 마일리지 또는 포인트로 가격을 인상하여 보상의 가치를 떨어뜨리는 경우가 있습니다.

세 번째 신용카드 리워드는 카드사에서 직접 발행하는 포인트로 다양한 용도로 사용할 수 있다. 예를 들어, 신용 카드 사용자는 각 회사에서 발급한 신용 카드로 비용을 지불하여 Chase Ultimate Rewards, American Express Membership Rewards 또는 Citi ThankYou Rewards를 받을 수 있습니다.

이러한 포인트를 독특하게 만드는 것은 일반적으로 다양한 용도로 사용할 수 있다는 것입니다. 예를 들어, 신용 카드 사용자는 명세서에 크레딧으로 캐쉬백을 받도록 선택하거나, 카드 제공자를 통해 직접 포인트를 사용하여 여행을 예약하거나(달러로 지불하는 대신), 여행 포인트/마일로 사용할 포인트를 양도할 수 있습니다. 다양한 항공사 및 호텔 파트너와 함께 합니다.

이러한 유연성과 파트너의 범위는 이러한 포인트를 특히 가치 있게 만듭니다. 예를 들어 유나이티드 항공의 공동 브랜드 신용 카드로 적립한 마일은 유나이티드를 통해 항공편을 예약하는 데 사용할 수 있지만 Chase Ultimate Rewards 포인트는 유나이티드 마일뿐만 아니라 Southwest, JetBlue, British Airways 및 하얏트, 메리어트 및 IHG의 호텔 포인트뿐만 아니라 다른 항공사. 또한 포인트는 증분(일반적으로 한 번에 1,000포인트)으로 이전될 수 있기 때문에 여행 프로그램 자체로 잔액을 '충전'하는 데 사용할 수 있습니다.

양도 가능한 포인트는 매우 유용할 수 있지만 발행 회사와 제휴한 신용 카드로만 적립할 수 있습니다. 신용 카드 지출을 통해 적립되는 항공사 마일리지나 호텔 포인트와 달리 이러한 포인트는 일반적으로 카드가 폐쇄될 때 소멸되기 때문에 개인은 카드를 취소하기 전에 포인트를 사용해야 합니다(개인이 이러한 포인트를 적립하는 다른 카드가 있는 경우 제외).

적립할 수 있는 신용 카드 보상의 유형이 다양한 것처럼 정기적인 신용 카드 사용을 통해 보상을 적립할 수 있는 방법도 많습니다. 가장 단순한 보상 수익 구조는 지출 범주에 관계없이 지출된 1달러에 대해 고정 수익을 제공합니다. 예를 들어 Citi Double Cash 카드는 모든 구매에 대해 2%의 캐시백을 제공합니다. 단순함을 중요시하고 캐쉬백을 우선시하며 주어진 거래에 어떤 카드를 사용할지 생각하고 싶지 않은 고객에게 이 스타일이 매력적일 수 있습니다.

보다 일반적인 구조는 지출한 1달러에 대한 기본 보상 금액을 제공하며, 특정 범주에서 획득한 추가 포인트는 연중 고정으로 유지됩니다. 예를 들어 Chase Sapphire Preferred 카드는 레스토랑에서 지출한 1달러당 Ultimate Rewards 포인트 3점, 여행 지출 시 2포인트, 기타 모든 구매 시 1포인트를 제공합니다. 카테고리는 카드마다 다르지만 더 인기 있는 옵션에는 주유, 식료품, 여행 및 레스토랑이 있습니다. 이러한 범주 중 하나 이상에 상당한 비용을 지출하는 고객에게는 이 구조의 카드가 유용할 수 있습니다.

세 번째 수익 구조는 지출한 1달러에 대한 기본 보상 금액을 제공하며, 연중 순환하는 특정 카테고리 구매에 대한 추가 캐시백 또는 보너스 포인트를 제공합니다. 예를 들어, Discover It 카드는 분기별로 특정 카테고리에서 최대 $1,500까지 구매 시 5% 캐시백을 제공하고 기타 모든 구매에는 1% 캐시백을 제공합니다. 한 분기의 카테고리는 식료품점일 수 있고 다음 분기는 주유소에서 구매 시 5%를 다시 제공할 수 있습니다. 각 분기에 이러한 보너스 카테고리를 활용하면 고정 수익 카드 지출에 비해 더 나은 보상을 얻을 수 있지만 사용자는 주어진 분기에 어떤 카테고리가 보너스 보상을 받는지 기억해야 합니다.

소비자는 일년 내내 카드에 대한 지속적인 지출을 통해 상당한 보상을 얻을 수 있지만 보상을 얻는 가장 빠른 방법은 새 카드에 가입하여 보너스를 받는 것입니다. 일부 카드는 가입하기만 하면 보너스를 제공하는 반면, 최고의 보너스는 일반적으로 특정 기간 동안 카드에 최소한의 지출을 요구합니다.

예를 들어, 항공사 공동 브랜드 신용 카드는 계정 개설 후 처음 3개월 동안 카드에 $3,000를 지출하는 경우 상용 고객 마일리지 50,000마일을 제공하고 카드로 이루어진 모든 구매에 대해 1마일을 제공할 수 있습니다. 3개월 동안 카드를 사용하여 $3,000를 성공적으로 사용한 사람은 3,000마일($3,000 사용 시 적립) + 50,000마일(소개 보너스) =총 53,000마일을 받게 됩니다. 보너스가 없다면 카드 소지자는 동일한 포인트를 획득하기 위해 카드에 $53,000를 지출해야 합니다!

신용 카드 가입 보너스의 수익성 때문에 개인은 1년 동안 많은 카드에 가입하려는 유혹을 받을 수 있습니다. 이것이 가능하지만 신용 카드 회사는 개인이 회사에 가질 수 있는 카드의 수와 가입 보너스를 받을 수 있는 빈도에 제한을 두고 있습니다. 이러한 제한 사항은 카드 발급사에 따라 다르며 시간이 지남에 따라 변경됩니다. 예를 들어, Chase는 일반적으로 신청자가 지난 24개월 동안 발행사로부터 5개 이상의 신용 카드를 개설한 경우 카드 신청을 승인하지 않습니다("5/24 규칙"이라고 함). 동일한 카드를 열거나 닫은 후 24개월 이내에 최대 보너스.

특히 주요 대출(예:모기지 또는 자동차 대출) 신청을 준비하는 고객과 관련된 또 다른 고려 사항은 새 신용 계좌 개설이 개인의 신용 점수 계산에 미치는 영향입니다. 새로운 신용 카드 계좌를 개설하는 것은 신용 점수에 긍정적인 영향을 미칠 수 있지만(예:총 신용을 높이고 신용 활용 비율을 낮춤으로써), 신용 신청은 일반적으로 개인의 신용 보고서에 대한 '어려운' 조회를 초래하며, 이는 부정적인 결과를 초래할 수 있습니다. 영향 점수.

또한 새 계정은 개인의 신용 점수에 영향을 미치는 다른 요소인 개인의 신용 계정 평균 연령과 가장 최근에 개설한 계정 연령을 낮출 수 있습니다. 궁극적으로 신용 카드 신청의 순 영향은 개인마다 다를 수 있으므로 가입 보너스에 관심이 있는 고객은 한 번에 하나의 새 계정만 개설하여 각 계정이 자신의 계정에 미치는 영향을 확인하는 것이 현명할 수 있습니다. 추가 카드를 신청하기 전에 신용 점수.

중요한 것은 신용 카드 보상이 수익성이 있을 수 있지만 고문은 남은 잔액에 대한 이자가 거의 (전부는 아닐지라도) 상당 부분을 상쇄할 가능성이 높기 때문에 매월 말에 잔액을 전액 상환하도록 조언하여 개인이 지출을 관리하는 데 도움을 줄 수 있습니다. 가입 보너스의 혜택입니다.

여러 장의 카드를 등록하는 개인도 다양한 지불 기한에 유의해야 합니다. 연체하면 이자와 벌금이 부과될 뿐만 아니라 개인의 신용 보고서에 마이너스 표시가 생기기 때문입니다!

일반적인 지속적인 지출을 통해서만 상당한 보상을 얻을 수 있지만, 신용 카드 등록 보너스는 수천 달러의 여행 가치가 있을 수 있으므로 실질적인 혜택을 가장 빠르게 모을 수 있는 방법 중 하나는 신용 카드 등록 보너스를 이용하는 것입니다! 그러나 사용할 수 있는 신용 카드 보상이 광범위하기 때문에 고문은 고객이 잠재적인 수익을 극대화할 수 있는 전략을 개발하는 데 어떻게 도움을 줄 수 있습니까?

결국, 어떤 고객이 매년 수천 달러를 벌거나 유럽이나 하와이로 무료 여행을 가도록 도와주는 고문과 일하고 싶지 않겠습니까!?트윗하려면 클릭

신용 카드 회사는 종종 카드 마케팅에 공격적입니다. 그리고 이러한 제안 중 일부는 매력적인 가입 보너스와 함께 제공되지만 가장 좋은 것은 일반적으로 온라인에서 찾을 수 있으며 제한된 시간에만 제공되는 경우가 많습니다.

여행 블로그 프리퀀트 마일러(Frequent Miler)는 고객을 위한 추천을 찾고 있는 고문에게 유용한 리소스가 될 수 있는 광범위한 신용 카드 발급사에 걸쳐 현재 사용 가능한 최고의 신용 카드 가입 제안 목록을 유지하고 있습니다. 신용 카드 회사. 예를 들어, 프리퀀트 마일러(Frequent Miler)는 현재 최고의 신용 카드 가입 제안이 첫해에 $1,500 이상의 가치가 있으며 다른 여러 카드에도 $1,000 이상의 보너스가 있다고 추정합니다!

신용카드 가입 보너스는 일반 대중이 사용할 수 있는 개인 카드뿐만 아니라 사업자 전용 '비즈니스' 신용카드에도 제공됩니다. 이 명함은 개인 카드에 필적하는 보너스를 제공할 수 있습니다. 비즈니스 소유자의 경우 신용 카드 가입 보너스는 지속적인 지출에 대해 상당한 보상을 받을 수 있는 좋은 방법이 될 수 있습니다!

신용카드 가입 보너스의 규모는 매우 다양하므로 보너스의 규모뿐만 아니라 개인에게 적합한 보상인지 여부도 고려하는 것이 중요합니다. 예를 들어 개인이 다양한 여행 로열티 프로그램으로 전환하거나 캐쉬백 보너스로 사용할 수 있는 50,000포인트의 보너스는 개인이 항공편에 대한 보상을 사용할 계획이 없는 경우 상용 고객 마일리지 60,000마일보다 더 가치가 있을 수 있습니다. .

가입 보너스를 비교할 때 '포인트당 센트' 프레임워크를 사용하는 것이 유용할 수 있습니다. 이를 통해 개인은 다양한 유형의 포인트 또는 마일에서 기대해야 하는 가치를 비교할 수 있습니다. 예를 들어 개인이 가입 보너스 50,000 호텔 포인트를 받고 해당 포인트를 $750의 호텔 숙박에 사용했다면 $750 ÷ 50,000 포인트 =사용한 포인트당 가치의 1.5센트를 받게 됩니다.

특정 항공사 또는 호텔 로열티 프로그램에 대해 개인이 받는 포인트당 센트는 특정 회사 및 사용된 보상 유형에 따라 다릅니다. While no two redemptions for a specific airline or hotel are exactly the same, the Frequent Miler blog has estimated cents per point values individuals can reasonably expect to receive from travel redemptions through these programs.

In the example above, even though the Hilton bonus was worth more points, Jerry is likely to get more value from the United miles. Often, the best cents-per-point value comes from redemptions for premium-class travel, which can have a very high cash cost and cents-per-point value.

Assessing the relative value of reward points can also depend on how points will be redeemed. In the following example, business-class travel offers twice the cents per point value than economy-class travel.

Ultimately, the best redemption offer for an individual can come down to their unique preferences. Just as there is no single 'right' choice for all financial planning clients, there is no 'right' miles or points redemption choice for everyone!

Clients who amass credit card rewards for travel have several ways to redeem them. Transferrable points (e.g., Chase Ultimate Rewards and American Express Membership Rewards) typically offer the most value because of their flexibility. They can be used to book travel directly through the credit card company’s travel portal, and can also be extremely useful for transferring to other airline and hotel reward programs, particularly when the individual has already earned miles or points (e.g., from business travel) but needs more for a given flight or hotel stay.

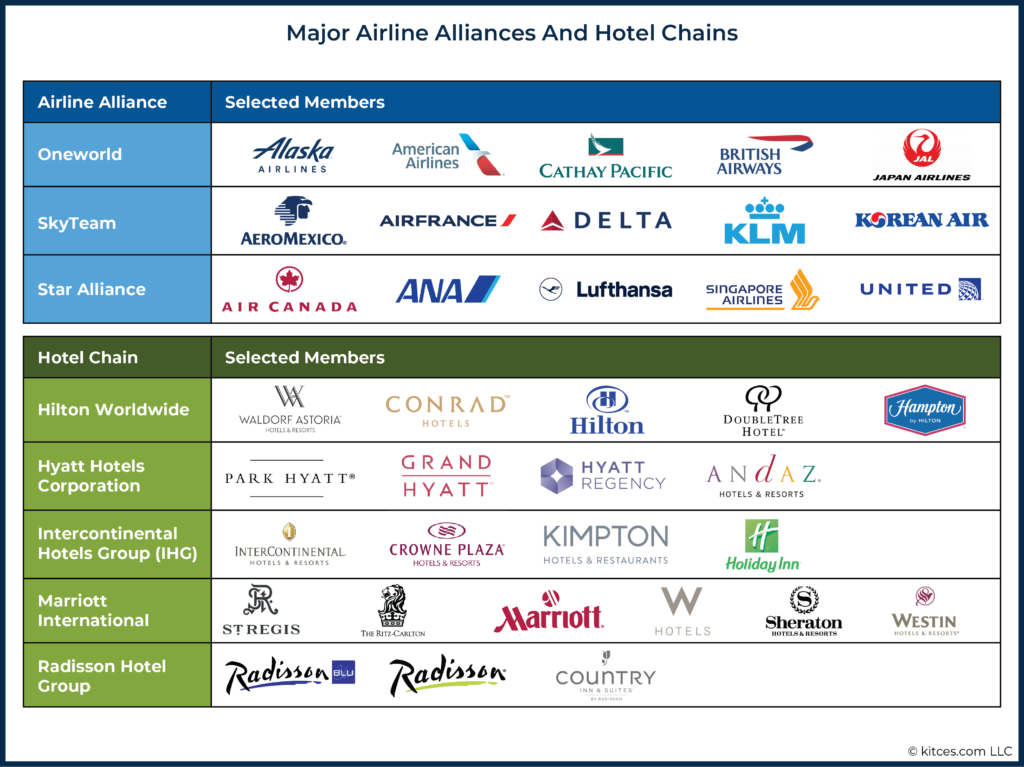

Frequent flyer miles and hotel points are affiliated with loyalty programs belonging to a specific airline or hotel (e.g., American AAdvantage miles or IHG Rewards Club points). And while airline miles and hotel points are less flexible than transferrable points, they do provide some flexibility for redemptions. Most major airlines are part of alliances (e.g., Star Alliance and one world Alliance) that allow individuals to earn and redeem miles with airlines across participating companies in the alliance.

For example, Delta SkyMiles can be redeemed not only for flights on Delta, but also on other SkyTeam alliance partners, such as Air France and Korean Air. The ability to use miles for flights on other airlines provides more options when booking flights using award points, particularly for international flights.

While there are no similar alliances for using hotel points, these points still offer flexibility in redemptions across a hotel chain’s portfolio of brands. For example, Marriott Bonvoy points can be earned and used at Marriott hotels, but also Ritz-Carlton, W Hotels, Westin, and Courtyard hotels, among others.

While the most valuable component of credit card offers is typically the sign-up bonus (which can consist of points, miles, or cash), many cards also come with additional perks (and expenses) that can also be evaluated when making comparisons.

Some cards affiliated with airlines or hotels offer perks related to that company. For example, airline-affiliated credit cards often offer a free checked bag or priority boarding benefits to their credit cardholders, while hotels might offer access to room upgrades. These perks can vary widely, but they still can be valuable for those who are able to take advantage of them.

Another consideration when evaluating a credit card offer is the annual fee that is associated with the card. Some cards with large bonuses and travel-related perks have large annual fees, so it is important to consider these in the calculation as well. For example, a card with a $95 annual fee offering a 50,000-point bonus is likely to be more valuable than a card with a $495 annual fee and a 60,000-point bonus for the same airline or hotel. At the same time, cards with higher annual fees often come with credits that can defray the cost of the annual fee. For example, while the American Express Platinum Card has a $695 annual fee, it comes with a $200 airline fee credit, $200 in Uber cash, a $200 credit for certain hotels, and a $240 credit for specified digital entertainment providers, among other credits and rebates. For cardholders who are frequent travelers, these perks can more than make up for the annual credit card fee!

Cards with annual fees may not be worth keeping after the first year, but some credit card companies may offer retention bonuses for those who ask to close their account, so it can be worthwhile to call the card company each year to see what might be available.

However, closing a credit card can potentially impact an individual’s credit score by reducing their total amount of credit available or the average age of credit accounts (depending on how old the account is). Therefore, it might not be prudent to close credit cards immediately before applying for a loan.

Finally, those applying for cards should also consider whether a sign-up bonus will be subject to taxation. While the IRS has not provided definitive guidance on the matter, points received for spending money on a credit card (including those received through sign-up bonuses and as rewards for regular spending) are typically treated as a non-taxable ‘rebate’ for purchases made, while sign-up bonuses that do not require spending on the card can be treated as taxable income. Credit card companies will typically issue the cardholder a 1099-MISC form for any taxable bonuses.

Individuals can get significant value from credit card rewards, but creating a realistic strategy for maximizing rewards can take time. Financial advisors who are familiar with the rewards landscape are well-positioned to support clients in deciding whether to apply for new credit cards and which ones to use for ongoing spending.

With the potential for clients to get thousands of dollars of value annually, crafting a credit card reward strategy can be a helpful way for advisors to demonstrate ongoing value to their clients.

Cash flow discussions can be a good opportunity to broach suitable credit card reward programs. Advisors can discuss not only what clients are purchasing with their money, but also how they are doing so. This can uncover important information to help craft a sensible rewards strategy, including how much the client spends with credit cards in total, which categories of expenses (e.g., groceries, gas) they spend the most money on, and whether they are planning any large one-time expenses that can be incorporated into the client’s strategy.

Understanding a client’s spending habits can help the advisor create a range of options for credit card bonuses and ongoing spending. For example, a client who spends $10,000 per month with credit cards will have greater capacity to meet any spending requirements for sign-up bonuses than one that only spends $1,000 per month.

Understanding the categories on which the client spends the most money can also help the advisor to recommend appropriate credit cards that maximize the spending in those areas. For example, a client that spends $20,000 per year on travel could be well-suited for a card that offers multiple points per dollar spent on travel expenses, while a client with a large family that spends $15,000 per year on groceries can consider a card with a points bonus for spending at grocery stores.

Finding out whether a client is expecting to have large one-time expenses can also be useful because a single expense could potentially cover the full amount of required spending for a credit card sign-up bonus.

For example, a client paying expenses for a child’s wedding could leverage sign-up bonuses to give themselves a vacation afterward!

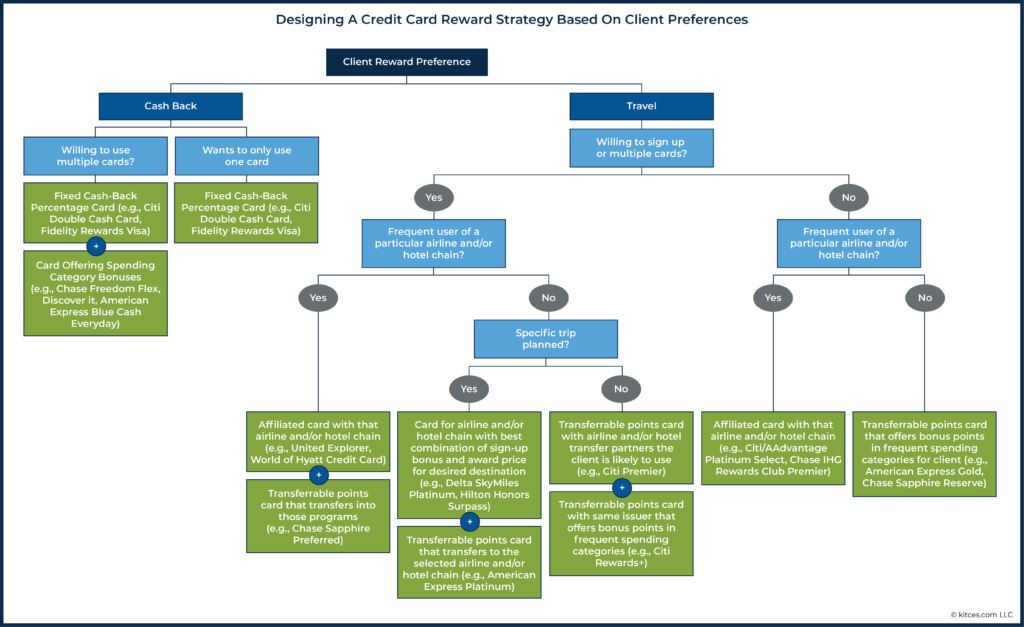

In addition to understanding a client’s spending patterns, it is also important to gauge their interest in certain credit card rewards and their preferences for using them. While some clients might be interested in applying for multiple new cards each year to build up points and miles through sign-up bonuses, others might be less interested in applying for cards and would prefer earning rewards on a single card. Either option can be profitable for the client, but it is important that they are comfortable with the process.

Clients who don’t travel much and who don’t want to manage multiple credit cards would benefit more from the flexibility and convenience of cash back rewards as opposed to point-based reward programs.

Clients who travel and who are willing to sign up for multiple credit cards in a given year can earn significant value from credit cards that offer transferrable points as well as those affiliated with the airlines and hotels they regularly use for travel.

Of course, clients are likely to have a wide range of preferences when it comes to earning and redeeming credit card rewards. The flow chart below shows how an advisor can work through the various credit card reward styles given client preferences to determine the best strategy and to recommend useful credit cards for the client.

To make better credit card recommendations over time, advisors can create a system to track their recommendations and how they are implemented. For example, including a client’s reward preferences (e.g., cash back or travel) and approximate credit card spending in their CRM file would allow the advisor to quickly come up to speed if the client asked for a credit card recommendation outside of the annual meeting.

Further, advisors can create a file to track the cards that clients apply for to ensure that they do not make duplicate recommendations and that their clients do not run afoul of the application limits imposed by the credit card companies.

Combining these steps with quarterly reviews of the Frequent Miler’s Best Offers page would give an advisor an understanding of both client preferences and available credit card options.

In addition to helping clients earn credit card rewards, advisors can also support the overall goal of redeeming points and miles for cash and travel. Cash back rewards are the easiest to redeem and are typically applied as statement credits (which are generally simpler than redeeming via direct deposit or physical check, which are sometimes also available options).

It is important to note that, depending on the card, cash back awards are not always automatically applied to each statement. Sometimes, cardholders may need to request the reward to be issued as a statement credit. Advisors can support this process by confirming with clients not only how much cash back they earned in a given year (which allows them to determine if clients have the best card(s) to maximize their rewards), but also that they actually redeem their rewards!

Redeeming credit card rewards for travel is a trickier process than getting cash back, but advisors can play an important role in helping clients get the travel awards they want if they understand how travel rewards work and the flexibility offered by transferrable points.

For example, some transferrable points can be redeemed for travel booked directly through the credit card issuer’s site at a fixed rate, such as with the Chase Sapphire Reserve card. Cardholders can redeem their Ultimate Rewards points at a rate of 1.5 cents per point for any travel booked through the Ultimate Rewards portal. For example, a cardholder would be able to redeem 20,000 points (earned through a signup bonus or through regular spending) × 0.015 cents per point =$300 toward flight expenses. This shows how transferable points can provide excellent flexibility, as clients can use them to book available flights with any airline, or lodging at any hotel, rather than be limited to flights offered by a certain airline alliance or hotel chain, as is the case with frequent flier miles or hotel loyalty programs.

On the other hand, airline flight rewards are determined either through award charts that set a fixed mile cost for travel between two regions or, increasingly, dynamically based on demand. This means that since a particular company’s miles or points can decline in value if the airline or hotel changes its award chart or pricing (e.g., to require more miles for a given flight or hotel stay), it is typically recommended to earn these travel rewards with a specific use in mind rather than building up a stash for an unspecified trip in the future (that could end up costing more points than it does now).

Hotel chains also publish reward charts that put their hotels in different reward redemption categories. For example, Hyatt’s chart has eight categories for its hotels, ranging from 5,000 points for a standard night at a Category 1 hotel (that typically includes Hyatt’s least expensive hotels in dollar terms) to 40,000 points per night at a Category 8 hotel (that includes some of Hyatt’s most expensive properties). While some clients might prefer to redeem their points for several nights at a lower-cost hotel, others might want to splurge on the luxury redemption.

Advisors can support clients in booking travel using miles and points by first understanding the client’s travel plans, researching approximately how many miles and/or points it will cost (using the companies’ award charts or pricing out the trip on the airline or hotel website), and then suggesting a credit card strategy that can earn them enough rewards to book the trip.

It is important to note that award availability can change, so it helps if clients plan well in advance and if they can be flexible with the dates of their trip. For clients who do not want to go through the process of searching for and booking the award travel on the airline’s or hotel’s website, many award-booking services are available; these can be particularly useful for booking premium-class flights where availability can sometimes be hard to find.

Ultimately, the key point is that clients can be leaving money (or travel opportunities) on the table by not maximizing their credit card rewards, and advisors who help them take advantage of their rewards can demonstrate ongoing value to clients.

Cash flow discussions during client meetings can serve as a starting point for gauging a client’s potential credit card spending and rewards preferences. Advisors can also recommend suitable credit cards for sign-up bonuses and ongoing spending based on a client’s interest, as well as supporting the award redemption process.

With the potential to earn thousands of dollars’ worth of cash or travel rewards annually, incorporating credit card rewards into financial planning discussions can be a major driver of client loyalty!