공개: 본 게시물은 제휴 파트너십을 통해 등록된 파트너로부터 무료로 보상을 받을 수 있습니다. 이는 우리의 평가에 영향을 미치지 않으며 의견은 우리 자신의 것입니다. 여기에서 자세히 알아보세요.

수백 가지의 복리 투자가 있습니다. 그러나 이들 모두가 귀하의 시간과 비용을 들일 가치가 있는 것은 아닙니다.

이것이 제가 최고의 복리 투자 및 계좌 목록을 만든 이유입니다.

여기에서 귀하에게 가장 적합한 투자를 찾는 데 필요한 모든 정보를 찾을 수 있습니다.

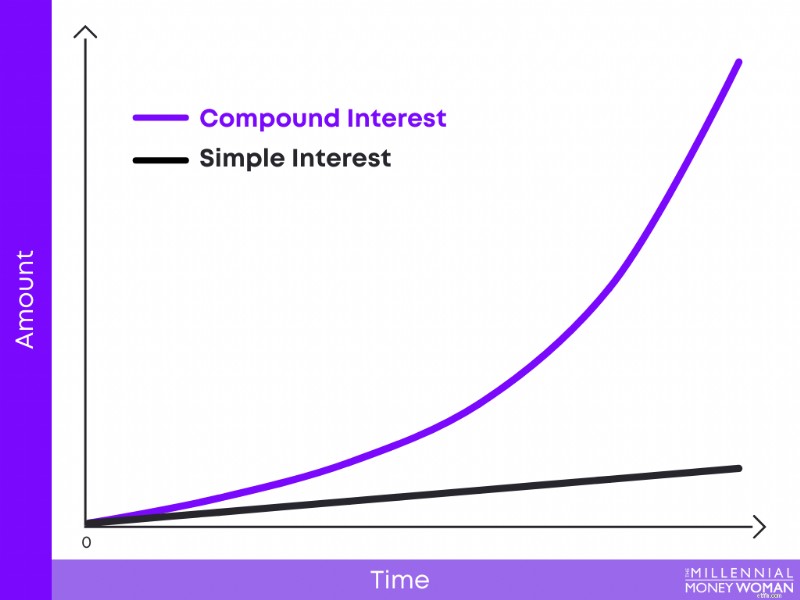

복리 이자는 원래 투자한 금액과 해당 투자에서 얻은 이자를 통해 이자를 얻을 수 있도록 도와줍니다.

기본적으로 귀하는 이자에 대한 이자를 받고 있습니다.

복리를 얻는 방법 이해하기 결국에는 단리와 복리의 차이를 이해하는 것이 중요합니다.

단리를 이용하면 귀하의 계좌에 발생한 이자가 얼마인지에 관계없이 원래 예금에 대한 이자를 받을 수 있습니다.

복리를 사용하면 원금뿐만 아니라 발생한 이자에서도 이자를 받을 수 있습니다.

그렇기 때문에 장기적인 복리 이자가 문자 그대로 세대의 부를 구축하는 데 도움이 될 수 있습니다. .

복리를 얻고 싶다면 이제 제가 보여드릴 전략을 실행해 보세요.

전통 자산과 대체 자산 모두에 대한 복리 투자를 어디에 투자해야 할지 정확히 공유하겠습니다.

시작해 보겠습니다.

복리 투자는 주식이나 채권에만 국한되지 않습니다.

실제로 포트폴리오를 다양화하고 높은 수익을 얻기 위해 개설할 수 있는 최고의 복리 계좌 중 하나는 부동산 투자 계좌입니다.

당신이 사랑한다면:

싫다면:

…그렇다면 당신은 민간 시장 온라인 REIT 투자자가 되는 것을 고려해 보아야 합니다.

REIT가 무엇인지 물어보실 수 있나요?

REIT(부동산 투자 신탁이라고도 함)는 투자자를 위한 소극적 소득을 창출하기 위해 여러 부동산을 소유 및 관리하는 회사입니다.

REIT는 다음과 같은 분야에 특화되어 있습니다:

REIT에는 2가지 유형이 있습니다.

여분의 현금이 있고 부업으로 약간의 추가 소극적 소득을 만들고 싶다면 Fundrise를 확인하세요 👇

Fundrise는 최고의 부동산 크라우드 펀딩 플랫폼 중 하나입니다. , 2012년 설립 이후 10억 달러 이상의 자산을 관리하고 있습니다.

모금 활동:

가장 좋은 점은 무엇인가요?

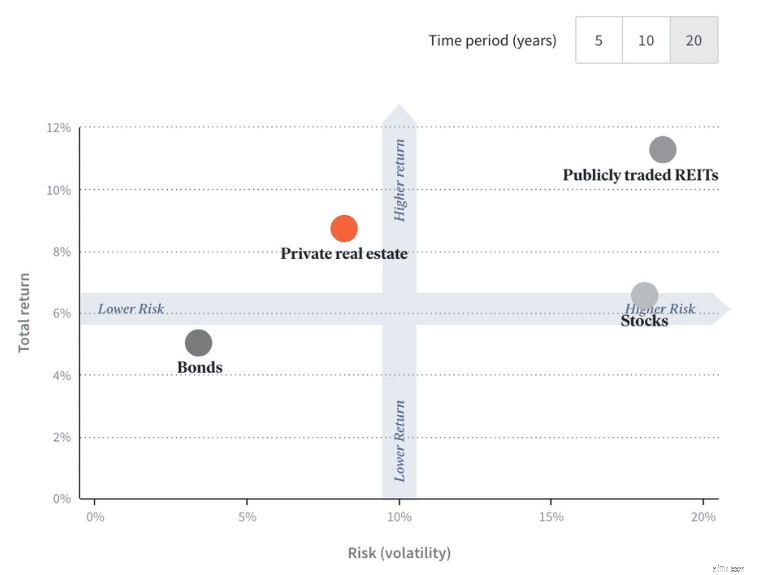

민간 시장 REIT는 주식 및 일부 공개 거래 REIT보다 위험 프로필이 낮습니다.

특히 S&P 500과 같은 주식 시장이 부진한 성과로 인해 폭락하는 해에는 REIT 투자가 귀하의 포트폴리오를 실제로 방해할 수 있습니다.

2022년 전체 429,627개 계좌에서 Fundrise 수익률은 평균 5.52%였으며, 이는 공공 REIT와 주식 시장 모두에서 대략 -19% 수익률을 기록했습니다.

수동적으로 현금을 벌고 싶다면 소득 창출 자산에 투자하세요. Fundrise가 제공하는 부동산 프로젝트가 귀하에게 매우 적합할 수 있습니다.

추천 도서: 모금 검토

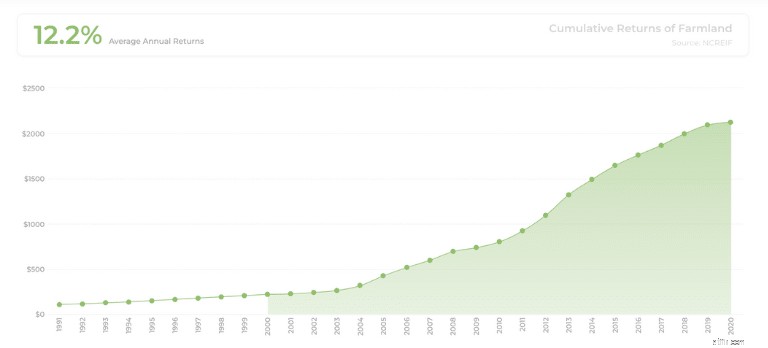

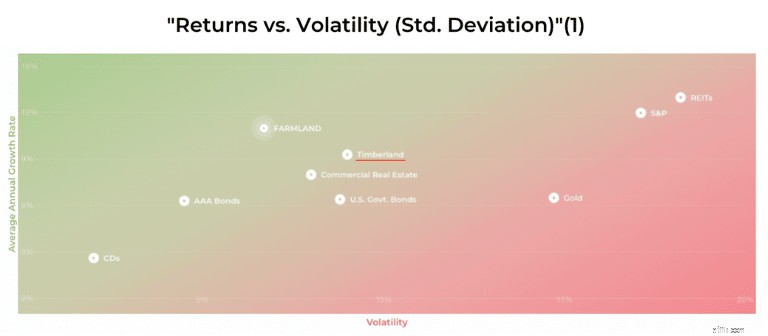

공인 투자자들이 제가 가장 좋아하는 복리 투자 중 하나는 농지와 목재입니다.

1990년 이후 농지 투자는 많은 주요 투자 유형을 능가했습니다.

실제로 1991년에 1,000달러를 투자하고 계속 투자했다면 현재 농지 투자 가치는 21,500달러가 조금 넘을 것입니다.

농지에 투자하는 것은 인플레이션 시기에도 최고의 투자 중 하나입니다.

보시다시피 농지의 연간 수익률은 약 11%로, 특히 2022년의 높은 인플레이션 수치를 고려하면 인플레이션을 이길 수 있습니다.

증가하는 세계 인구와 식량 생산에 대한 수요와 함께 농지 투자는 실제로 더 높은 수익과 더 낮은 변동성을 지닌 다양한 투자 기회를 제공합니다.

농지와 같은 자산에 투자하는 것은 훌륭한 대체 투자입니다. , 특히 인플레이션을 극복하고 높은 수익을 창출하려는 경우.

농지에 투자할 준비가 되셨나요?

그렇다면 FarmTogether 플랫폼을 확인해 보세요👇

FarmTogether를 사용하면 농지 투자가 쉬워지며 모두 온라인으로 가능합니다.

FarmTogether에 투자할 때 주의할 점은 공인 투자자여야 한다는 것입니다.

공인 투자자:

여분의 현금이 있다면 다음과 같은 작물에 투자할 수 있습니다.

그리고 평균적으로 농지 수익률은 연간 약 10%입니다!

따라서 최고의 복리 투자 중 하나에 투자하고 싶다면 FarmTogether와 같은 크라우드 펀딩 플랫폼을 통해 농지에 투자하는 것이 좋은 다음 단계가 될 수 있습니다.

의심할 여지 없이 최고의 복리 투자 중 하나는 인덱스 펀드입니다.

인덱스 펀드는 뮤추얼 펀드일 수도 있고 전체 시장 지수의 수익률을 추적하는 ETF일 수도 있습니다.

복리를 발생시키는 인덱스 펀드에는 다음이 포함됩니다.

즉, 인덱스 펀드는 Apple과 같은 우량 기업(S&P 500 인덱스 펀드)부터 소규모 스타트업(Russell 2000과 같은)에 이르기까지 다양한 지수를 추적할 수 있습니다.

인덱스 펀드는 다음과 같은 이유로 초보자에게 좋습니다:

게다가 장기적으로 투자한다면 실제로 많은 돈을 벌 수 있습니다.

물론 시장에는 항상 상승과 하락이 있을 것이지만, 적어도 역사적 관점에서 볼 때 시장은 항상 상승해 왔습니다.

예를 들어, 1985년에 1,000달러를 투자하고 2022년 11월까지 주식 시장에 남겨 두었다면 최종 가치는 약 69,730달러가 됩니다.

따라서 초기 투자금 1,000달러에 대해 6,873%의 이익을 얻었을 것입니다.

그리고 점점 더 좋아지고 있습니다. 인덱스 펀드에 투자하는 것은 실제로 정말 쉽습니다.

방법은 다음과 같습니다:

그렇다면 최고의 주식 거래 플랫폼은 무엇일까요?

초보투자자라면 늘 도토리를 추천드려요👇

Acorns는 다음을 수행할 수 있는 온라인 투자 플랫폼입니다.

큰 금액처럼 들리지 않을 수도 있지만, 가지고 있는 작은 센트까지 계속 투자하면 시간이 지남에 따라 복리 이자로 큰돈을 벌 수 있습니다.

주식으로 부자가 되고 싶다면 그렇다면 가장 좋은 방법 중 하나는 장기적으로 인덱스 펀드를 구입하는 것입니다.

임대 부동산에 투자하는 것은 아마도 복리와 소극적 소득을 얻을 수 있는 가장 일반적인 방법 중 하나일 것입니다.

임대 부동산 투자는 다양한 수입원을 구축할 수 있는 방법이기도 합니다. 생계를 유지하기 위해 급여에만 의존하지 마세요.

임대 부동산을 이용하면 다음 두 가지 방법 중 하나로 돈을 벌 수 있기 때문입니다.

특히 지난 10여년 동안 임대 부동산 투자는 매우 수익성 있는 투자가 되었습니다:

임대 부동산의 가장 좋은 점은 경기 침체기에도 임대 소득이 매우 안정적인 수입원이라는 것입니다.

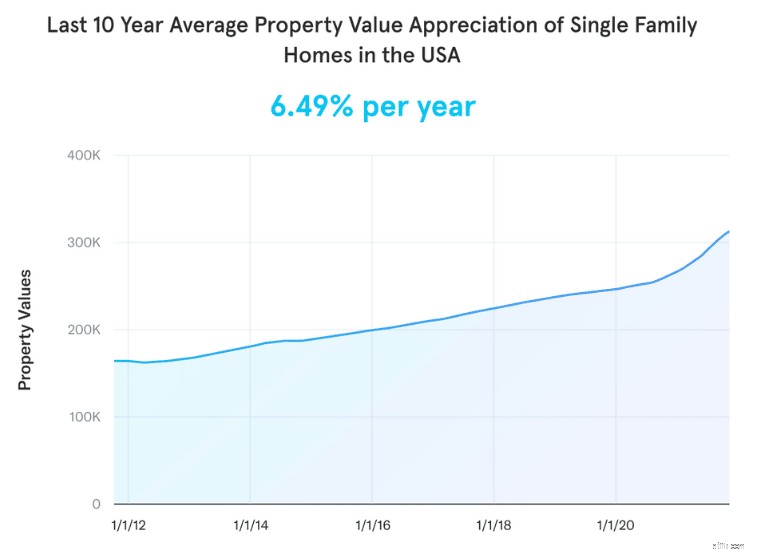

물론 임대 수입을 얻을 수 있을 뿐만 아니라 부동산 가치 상승을 통해 추가 현금을 얻을 기회도 있습니다.

실제로 지난 10년 동안 부동산 가치는 연간 약 6.49% 증가했습니다.

대부분의 임대 부동산 투자에는 1,000달러를 선불로 지불해야 하지만, 임대 부동산 투자 플랫폼인 Arrived Homes에 가입하면 실제로 100달러만 있으면 투자를 피할 수 있습니다. .

Arrived Homes는 미국 전역의 여러 부동산에 투자할 수 있는 온라인 임대 부동산 투자 플랫폼입니다.

Arrived Homes를 사용하면 미국 전역의 다양한 단독 주택에 투자하고 소극적 소득 포트폴리오를 구축할 수 있습니다.

추천 도서: 도착된 주택 검토

당신이 더 위험한 투자자이고 복리를 창출하고 싶다면 휴가용 임대 부동산을 확인해 보는 것이 좋습니다.

휴가용 임대 서비스는 다음을 제공할 수 있습니다:

다음은 휴가용 주택과 단독 주택 임대용 부동산을 비교한 것입니다.

휴가용 임대 주택은 단독 주택 임대 주택보다 훨씬 더 높은 현금 흐름 기회를 제공합니다.

실제로 풀타임 렌탈에 투자하면 기존 렌탈보다 130% 더 많은 수익을 얻을 수 있습니다.

하지만 휴가용 임대 부동산 소유와 관련된 위험을 확실히 이해해야 합니다.

특히 업무 유연성이 향상되고 '재택근무' 트렌드가 확산되면서 휴가용 임대 주택의 가치가 급등했습니다.

그렇다면 휴가용 임대 숙소에 투자하려면 어떻게 시작해야 할까요?

Arrived Homes와 같은 플랫폼에 가입 👇

휴가용 임대 부동산을 찾으면 나머지 투자 과정은 실제로 매우 간단합니다.

모든 부동산 투자와 마찬가지로 귀하의 자금은 몇 년 동안(최대 5년) 비유동적이라는 점을 기억하십시오.

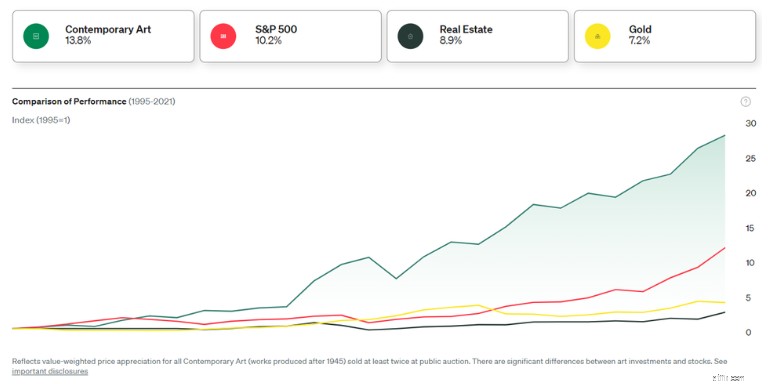

미술품에 투자하는 것은 시간이 지나면서 순자산을 쌓아가는 자산을 활용할 수 있는 또 다른 방법입니다.

실제로 2000년 이후 우량 미술품이 주식 시장보다 250% 이상 더 나은 성과를 냈다는 사실을 알고 계셨나요?

여유 현금이 있고 조금 더 위험을 감수할 의향이 있다면 미술품 투자가 적합할 수 있습니다.

신중하게 선택하시면 미술품 투자에 도움이 될 수 있습니다:

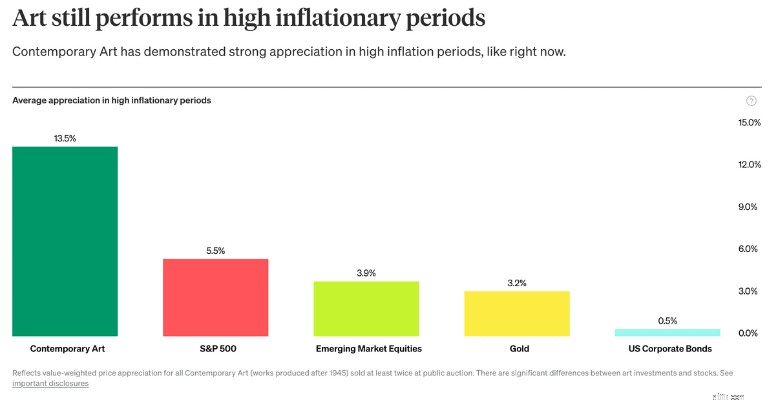

실제로 지난 몇 년 동안 미술이 인플레이션을 어떻게 극복했는지 확인해 보세요.

그러나 미술에는 위험도 따릅니다.

일부 위험은 다음과 같습니다:

또한 귀하의 자금은 해당 잠금 기간 동안 수익을 창출하지 못한 채 오랜 기간(때로는 최대 5년 이상) 동안 잠겨 있다는 점에 유의해야 합니다.

하지만 – 예술 작품으로 연간 15.3%의 수익을 올릴 수 있습니다.

이는 주식시장의 연평균 수익률 7~9%보다 훨씬 높은 수치입니다.

그렇다면 미술품 투자를 어떻게 시작하나요?

Masterworks라는 최상위 미술 투자 플랫폼에 투자하여 👇

Masterworks를 사용하면 다음과 같은 아티스트의 상징적인 걸작에 투자할 수 있습니다.

그리고 주식을 팔고 싶다면 2차 시장을 이용하면 됩니다.

그렇지 않은 경우, 귀하가 주식을 보유하면 Masterworks는 고객에게 29.03%의 연간 순수익을 자랑했습니다.

추천 도서: 걸작 리뷰

최고의 복리 투자 중 하나에 투자하려는 경우 중소기업 투자를 고려해야 합니다.

실제로 중소기업에 투자 소극적 소득 흐름을 구축하고 인플레이션에 맞서 싸우는 데 도움이 될 수 있습니다.

시간이 지남에 따라 중소기업이 어떻게 주식 시장보다 나은 성과를 냈는지 확인하세요:

Russell 2000은 일반적으로 미국 전역의 중소기업을 대표하는 데 사용되는 벤치마크 지수입니다.

그러나 보라색 선은 S&P 500으로 대표되는 대형주인 블루칩보다 변동성이 훨씬 더 크다는 점에 유의하세요.

중소기업은 다음과 같은 이유로 위험할 수 있습니다.

그러므로 투자하기 전에 항상 조사를 하십시오.

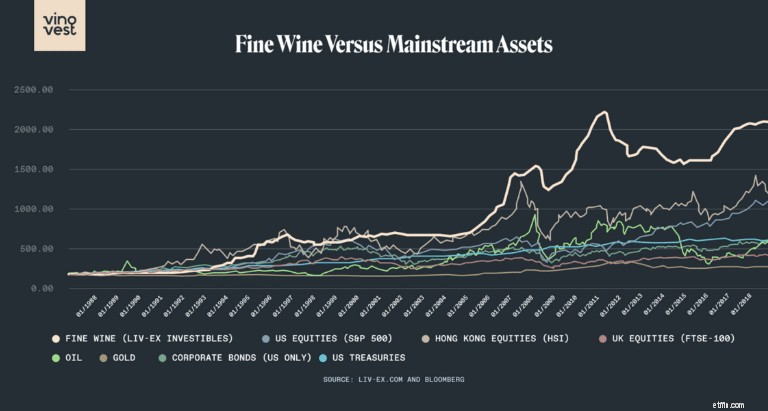

고급 와인 투자가 석유, 금, 주식과 같은 주류 자산보다 지속적으로 더 좋은 성과를 냈다는 사실을 알고 계셨습니까?

아래에서 확인해 보세요:

고급 와인이 실제로 좋은 투자 옵션인 이유는 다음과 같습니다.

이제 좋은 소식은 기술 덕분에 고급 와인에 투자하는 것이 예전만큼 어렵지 않다는 것입니다.

와인에 투자하려면 Vinovest를 확인하세요👇

Vinovest는 귀하의 위험 허용 범위와 선호도에 따라 맞춤형 와인 포트폴리오를 관리하며, 시작하는 것은 완전히 무료입니다!

Vinovest는 말 그대로 다음을 포함한 모든 것을 처리해 드립니다.

와인을 구매하는 대신 실제로 실제 병을 구매한 후 판매하기로 결정할 때까지 외부 시설에 보관됩니다.

좋은 와인으로 장기적으로 투자하는 것을 잊지 마세요. 고급 와인의 가치가 평가되기까지는 수년이 걸리는 경우가 많습니다.

추천 도서: 비노베스트 리뷰

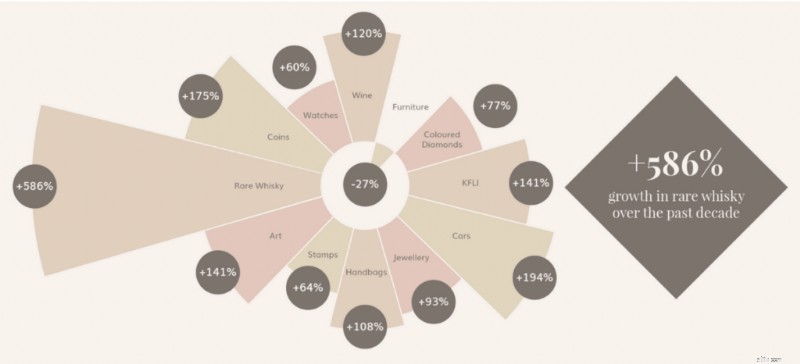

고급 와인 투자와 마찬가지로 복리를 창출하기 위해 희귀 위스키에 투자하는 것도 고려할 수 있습니다.

실제로 지난 10년 동안 희귀 위스키의 가치는 586%나 상승했습니다!

그리고 금, 석유 등 잘 확립된 다른 자산군에 비해 희귀 위스키는 지난 10년 동안 이러한 자산군보다 더 나은 성과를 거두었습니다.

고급 와인에 투자하는 것과 마찬가지로 Whiskyvest 플랫폼을 통해 희귀한 위스키에 투자할 수도 있습니다. .

Whiskyvest는 실제로 Vinovest의 새로운 파생 상품입니다.

온라인 플랫폼을 통해 세계에서 가장 희귀한 위스키에 투자할 수 있습니다.

Whiskyvest는 전문 지식을 활용하여 귀하의 투자 요구에 맞는 희귀 위스키 포트폴리오를 구성할 수 있도록 도와드립니다.

귀하는 희귀한 위스키가 담긴 실제 통을 구입하게 되며 Whiskyvest가 귀하를 위해 해당 통을 보관, 보험 및 운송해 드립니다.

여유 현금이 있다면 희귀한 위스키에만 투자하는 것을 잊지 마세요.

이는 장기 투자(최대 20년 이상)이며 비유동적입니다.

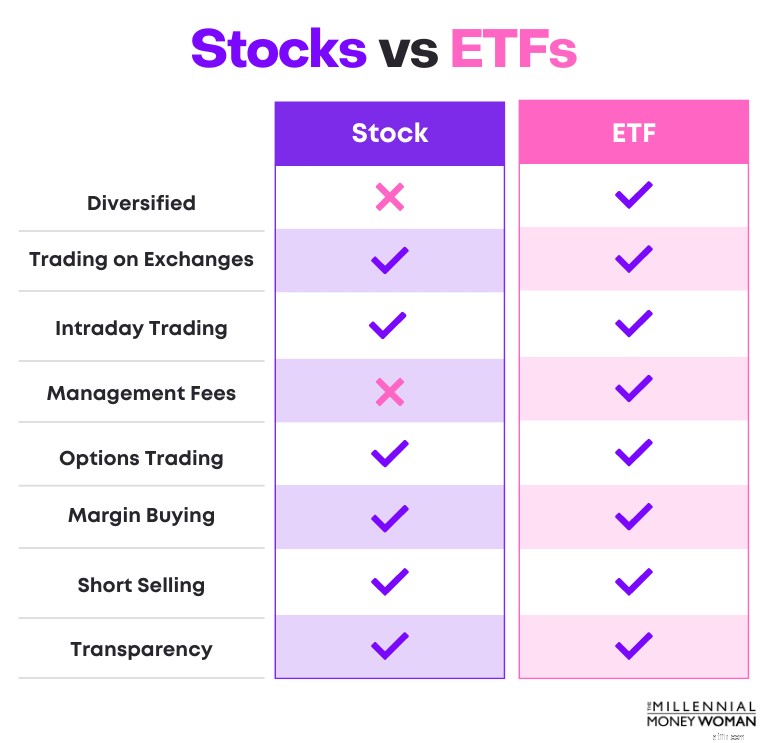

저렴한 비용으로 다양한 투자로 복리를 얻는 방법이 궁금하다면 ETF를 확인해 보세요.

상장지수펀드(ETF라고도 함)는 지수를 추적합니다(예:제가 가장 좋아하는 S&P 500).

ETF는 시장보다 나은 성과를 추구하지 않고 단지 시장을 따라갈 뿐입니다.

ETF는 다음과 같은 이유 때문에 최고의 복리 투자 중 하나입니다.

주식과 마찬가지로 ETF는 거래 시장 시간(오전 9시 30분부터 오후 4시(EST)) 동안 매수 또는 매도할 수 있습니다.

귀하의 포트폴리오에 선택하는 ETF 유형은 전적으로 귀하의 목표와 위험 허용 범위에 따라 달라집니다.

일부 ETF 유형은 다음과 같습니다:

Seeking Alpha에 가입하시면 선호하는 ETF에 대해 더욱 심층적인 조사(역사적 성과, 투자자 인사이트 등)를 하실 수 있습니다 👇

Seeking Alpha는 공정하고 정량적인 투자 정보를 원하는 투자자를 위한 투자 리서치 플랫폼입니다.

추천 도서: 알파 검토 요청

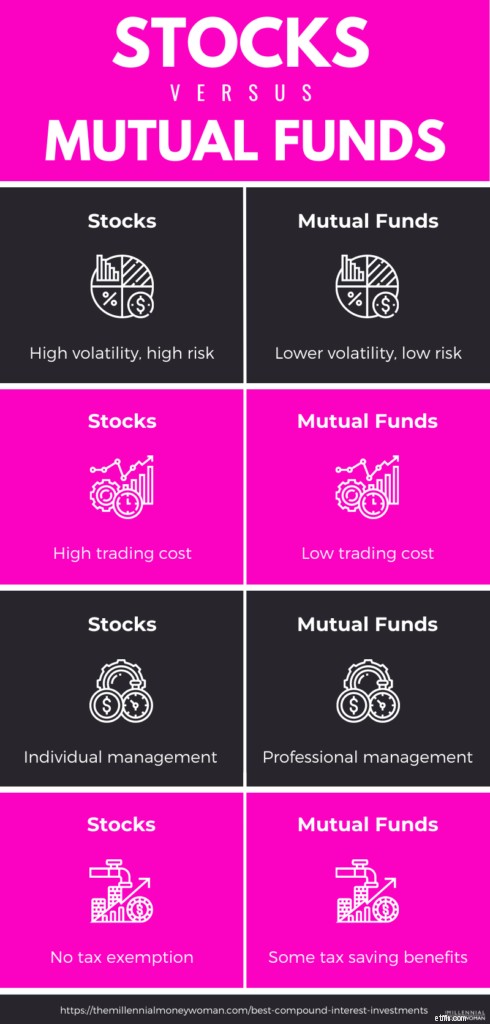

뮤추얼 펀드는 자산을 구매하기 위해 다양한 투자자가 전문적으로 관리하는 자금 풀을 의미합니다. 주식, 채권, 상품 등이 있습니다.

수동적으로 투자하는 ETF와 달리 뮤추얼 펀드는 실제로 높은 수익을 창출하기 위해 백그라운드에서 적극적으로 일하는 사람들이 있습니다.

뮤추얼 펀드는 전문적인 투자 관리를 제공하므로 일반적으로 초보자에게 적합한 복리 투자 수단입니다.

뮤추얼 펀드는 일반적으로 주식보다 더 다양한 복리 투자를 하기 때문에 뮤추얼 펀드는 주식보다 변동성이 적은 경우가 많습니다.

수천 개의 뮤추얼 펀드가 있으므로 Seeking Alpha와 같은 전문 투자 서비스에 가입하는 것이 좋습니다. .

Seeking Alpha는 투자 수단을 평가하는 데 공정한 접근 방식을 취하는 투자 플랫폼으로, S&P 500보다 90% 더 나은 성과를 냅니다.

따라서 어떤 뮤추얼 펀드가 자신에게 가장 적합한 선택인지 고민된다면 알파의 조언 찾기를 확인해 보세요.

특히 $1,000를 투자하려는 경우 그렇다면 뮤추얼 펀드는 다양한 투자 접근 방식을 취하므로 훌륭한 선택이 될 수 있습니다.

최고의 복리 투자 중 하나는 단연 배당주입니다.

배당주는 회사가 이익을 분배할 때 배당금의 형태로 주주들에게 수동적 소득을 제공합니다.

배당주는 복리 투자의 원투펀치와 같습니다.

이유는 다음과 같습니다:

배당금은 일반적으로 회사 자체의 성과에 따라 분기마다 지급됩니다.

실제로, 시장 변동성이 심한 기간(대공황 등) 동안 배당주는 실제로 회사가 망하지 않는다는 사실을 투자자들에게 확신시키기 위해 배당금 지급액을 늘립니다.

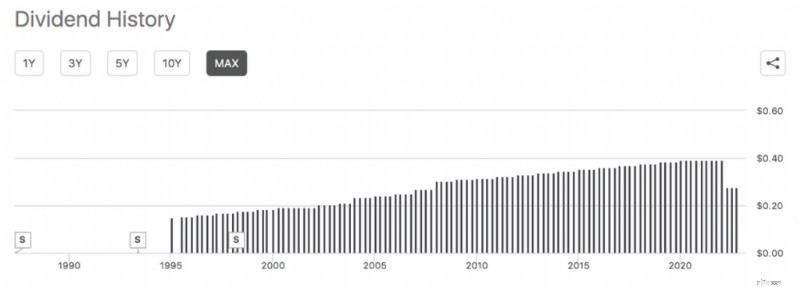

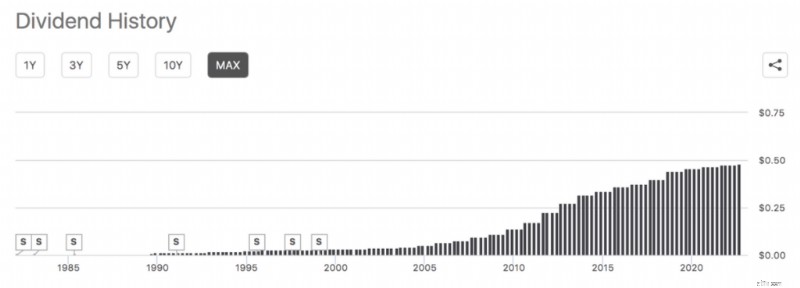

AT&T 배당 내역을 확인하세요. 예:

위 스크린샷에서 2008년 대불황 동안 AT&T가 실제로 배당금을 늘린 것을 볼 수 있습니다.

이는 우량 기업, 성숙 기업의 전형적인 배당 행위입니다.

왜요?

그들은 투자자를 유지하고 싶어하기 때문입니다.

Walgreens 배당 내역의 다른 스크린샷을 확인하세요:

다시 한 번, 2008년 대불황과 2020년 코로나 사태와 같은 주요 금융 위기 동안 Walgreens는 투자자를 유지하기 위해 배당금을 높였다는 것을 알 수 있습니다.

그러니 절대 배당수익률이 가장 높은 회사만 찾지 마세요.

다음을 포함하여 회사의 기본 원칙에 대해서도 조사해 보십시오.

시중에 배당금을 지급하는 주식이 1,000개는 아니더라도 사실상 100개가 있기 때문에 Seeking Alpha를 구독하는 것이 좋습니다. .

Seeking Alpha는 상위 배당주를 분석할 뿐만 아니라 각 배당주에 대한 정량적 데이터를 말 그대로 파헤쳐 볼 수 있습니다.

성장주와 달리 배당주는 다음과 같습니다.

배당금을 지급하는 주식을 구입하는 것은 경기 침체에 대비하는 좋은 방법입니다. .

배당주로 구성된 복리 계좌는 다음과 같은 잠재력을 가지고 있습니다:

배당주와 같은 복리 투자에 투자할 준비가 되셨나요?

M1 Finance에 가입하여 시작하세요 👇

M1 Finance는 무료 온라인 투자 앱입니다. 에서 6,000개 이상의 주식과 ETF에 액세스할 수 있습니다.

투자를 시작하려면 100달러만 있으면 됩니다.

배당주는 확실히 최고의 복리 투자 중 하나이지만 성장주도 잊어서는 안 됩니다.

성장주는 아직 성장 초기 단계에 있는 회사의 주식입니다. 이는 더 위험한 투자이지만 미래 이익에 대한 전망이 높습니다.

이름에서 알 수 있듯이 성장주는 많은 성장 잠재력을 가지고 있습니다...

…그러나 이는 성장주에는 그에 따른 위험이 따른다는 의미이기도 합니다.

일부 성장주 위험은 다음과 같습니다.

성장주는 성장 잠재력이 크기 때문에 일반적으로 성숙한 기업을 대표하는 배당주보다 가격이 더 비쌉니다.

일반적으로 성장주의 예는 다음과 같습니다:

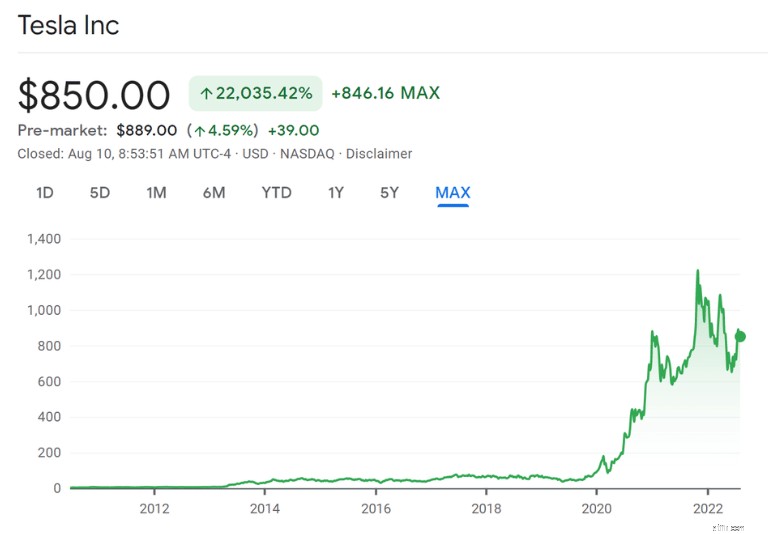

Tesla 주식의 성장을 확인하세요:

보시다시피 테슬라의 주가가 급등했습니다!

하지만 주가가 상승하는 데 얼마나 오랜 시간이 걸렸는지 주목하세요…

따라서 성장주 투자자가 되고 싶다면 일반적으로 장기적으로 투자 상태를 유지해야 합니다.

성장 기업은 주주에게 급여를 지급하는 대신 자본을 사용하여 사업에 투자하는 것을 선호하므로 주식을 매각할 때까지 배당금이나 수익을 받을 수 없습니다.

복리를 창출하고 포트폴리오를 다양화할 수 있는 간단한 방법을 찾고 있다면 채권 투자를 고려해 보세요.

채권은 고정 수입원(이자)을 얻고 초기 투자금을 전액 상환하는 대가로 제공하는 대출입니다.

채권은 일반적으로 다음과 같은 자금을 조달하기 위해 투자자에게 발행됩니다.

발행자(채권을 발행한 주체)는 일정 기간 동안 귀하의 투자금과 이자를 전액 상환할 것을 약속합니다.

채권 만기가 중요한 이유가 바로 여기에 있습니다.

채권 만기는 채권 투자에 대해 이자를 지급받는 기간을 정의합니다.

채권이 만기일에 도달하면 상환되고 계약이 완료됩니다.

다음과 같은 다양한 유형의 채권이 있습니다:

채권에 대한 이자율은 채권의 위험에 따라 달라집니다.

채권 유형(예:회사채)의 위험성이 높을수록 이자율은 높아집니다.

채권은 일반적으로 현금을 제외하고 가장 보수적인 투자입니다.

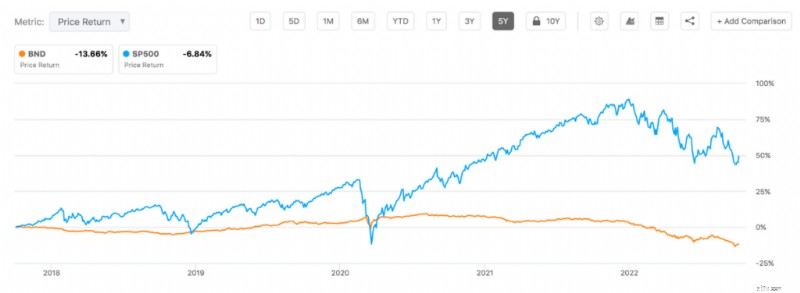

S&P 500 대비 채권 실적을 확인하세요:

채권이 일반적으로 주식 시장을 능가하는 유일한 때는 변동성이 극심한 시기뿐입니다.

이것이 바로 채권이 다각화된 훌륭한 포트폴리오인 이유입니다.

다양한 유형의 채권에 대해 자세히 알아보고 싶다면 Seeking Alpha에 가입해 보세요. .

Seeking Alpha는 투자 전문가의 연구 기사, 과거 데이터, 차트 등을 제공합니다.

투자하기 전에 데이터를 조사하는 것을 좋아한다면 Seeking Alpha가 아마도 최고의 투자 조사 플랫폼일 것입니다!

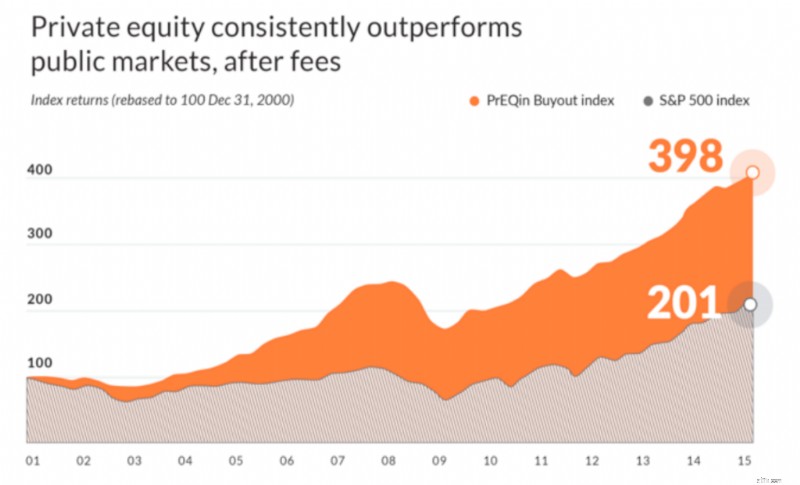

막대한 연간 수익을 얻는 데 도움이 될 수 있는 또 다른 복리 계좌는 사모 펀드 투자입니다.

사모 펀드(PE) 투자는 사모 펀드 회사가 민간 기업을 매각하거나 IPO(기업공개)를 통해 기업을 공개하기 전에 이를 매입하고 관리하는 대체 투자 형태입니다.

회사의 "지분"을 매입한 후 사모펀드 회사는 일반적으로 지분을 매각하기 전에 회사 성장을 목표로 이러한 회사를 운영하고 관리합니다.

그리고 사모 펀드는 확실히 배당금을 지급할 수 있습니다(말장난 의도는 아닙니다!). 확인해 보세요:

사모 펀드 시장은 (특히 2008년 대침체와 같은 시장 침체 기간 동안) 지속적으로 공개 시장보다 우수한 성과를 보였으며 이는 수수료 이후입니다!

사모 펀드 투자의 주요 단점 중 하나는 높은 수수료입니다. 수수료는 대개 2%에서 시작하여 최대 20% 이상까지 올라갈 수 있습니다.

비교해 보면, 인덱스 펀드에 투자하면 아마도 0.1% 이하의 수수료를 지불하게 될 것입니다.

그러나 아마도 수익도 줄어들 것입니다.

다음과 같은 경우 사모펀드에 투자해야 합니다:

PE는 투기적이기 때문에 사모펀드 투자는 위험할 수 있다는 점을 기억하세요.

Yieldstreet와 같은 플랫폼을 통해 사모펀드 투자를 시작할 수 있습니다. .

복리 투자에는 해양 금융과 같은 대체 투자도 포함될 수 있습니다.

해양 금융은 장기적으로 해양 선박 활동에 자금을 조달하는 데 중점을 둡니다.

해양 금융의 몇 가지 예는 다음과 같습니다.

엠파이어 스테이트 빌딩의 높이만큼 선박의 길이가 긴 경우가 많으며, 400,000톤의 화물을 운반하려면 선박을 건조해야 한다는 점을 명심하세요.

우리가 소비하는 것의 90% 이상이 선박을 통해 우리에게 들어온다는 사실만 알면 해양 금융을 통해 상당한 수익을 창출할 수 있습니다.

실제로 해상 무역 산업은 궁극적으로 대륙에서 대륙으로 물품을 운송함으로써 세계의 다른 모든 산업을 지원합니다.

그리고 2017년 해상 무역 산업의 가치는 미화 약 12조 달러에 달했습니다.

2003년 이후 세계 해운산업은 주로 중국의 산업화에 힘입어 5년 슈퍼사이클을 겪었다.

2008년 대불황으로 인해 세계 무역이 거의 정지되었고, 이로 인해 해운 산업이 거의 붕괴되었습니다.

그러나 해운업이 반등하면서 Yieldstreet와 같은 대체 투자 플랫폼을 통해 해양 금융 벤처에 투자하여 잠재적으로 높은 수익을 얻을 수 있습니다 👇

공인 투자자라면 해양 금융 기회(및 기타 민간 시장 배치)에 투자할 수 있습니다.

Yieldstreet에서 대부분의 해양 금융 기회는 단기(일반적으로 1~3년)이며 자산(선박 자체)으로 뒷받침됩니다.

추천 도서: YieldStreet 리뷰

복리이자 투자는 합법적인 자금 조달과 같은 대체 경로를 택할 수도 있습니다.

법률 자금 조달은 소송 자금을 조달하기 위해 법률 회사에 돈을 대출하는 것입니다.

누군가의 소송에 자금을 지원하는 대가로 귀하는 최종 합의금의 일부를 받게 됩니다.

물론 합의가 이루어지지 않으면 돈을 잃게 됩니다.

법적 자금 조달은 위험한 노력이지만 참여한다면 상당한 돈을 벌 수 있습니다.

관심이 있고 공인 투자자 자격이 있다면 Yieldstreet의 Legal Finance Fund를 확인하세요 👇

귀하의 자금이 소요될 일반적인 소송 유형은 다음과 같습니다.

이러한 대규모 소송에 참여하려면 연구 비용, 컨설턴트, 전문가 증인 및 법률 회사 간접비로 수백만 달러가 필요한 경우가 많습니다.

원고가 지불해야 하는 1,000,000달러 이상의 선불 법률 비용을 줄이기 위해 법률 회사는 비상 비용 조정에 참여했습니다.

비상 수수료 조정은 법률 회사가 초기 비용을 부담하는 경우가 많다는 것을 의미합니다.

그러나 법률 자금 조달 계약을 통해 로펌은 잠재적으로 수백만 달러에 달하는 소송을 해결하는 데 도움이 되는 대체 자금 조달 방법을 찾을 수 있습니다.

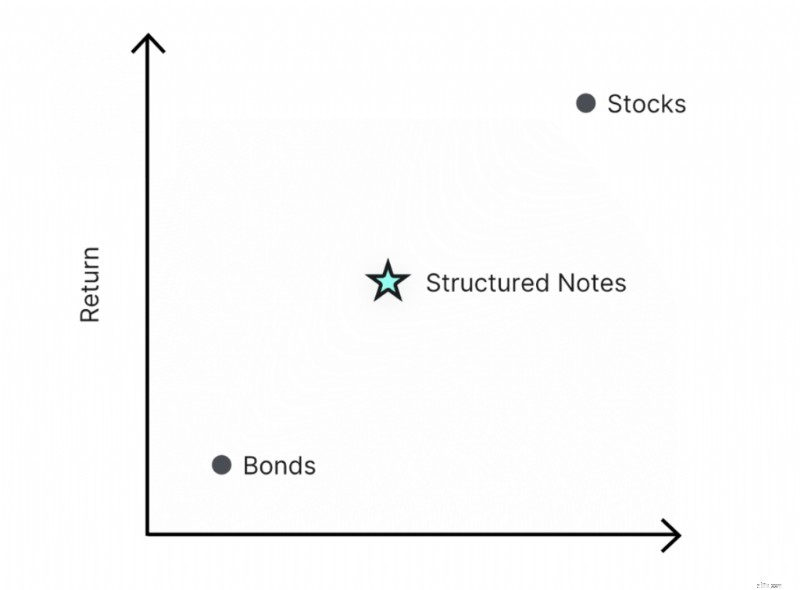

포트폴리오에 추가할 수 있는 또 다른 복리 투자는 구조화 노트입니다.

구조화 채권은 수익이 기초 주식의 성과와 연계되어 있는 다양한 금융 부채 투자를 의미합니다.

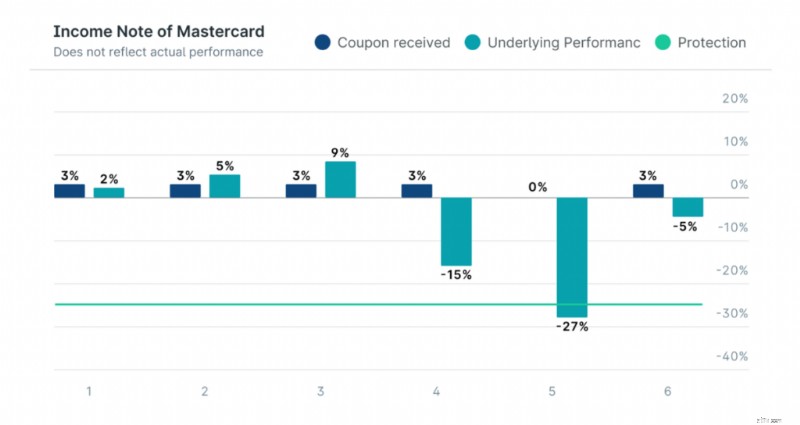

예를 들어, 채권의 성과는 마스터카드 주식처럼 기본 주식의 가치에 따라 결정됩니다.

구조화된 노트는 "섹시한" 느낌을 줄 수 있지만 약간 더 위험한 경향이 있습니다.

구조화된 노트는 하락세에 대한 보호 가치도 제공합니다.

예를 들어, 하방 보호 가치가 25%이고 소득 수익률이 3%인 경우 기본 주식의 가치는 채권을 구입한 날의 가치에서 25% 하락할 수 있으며 영향을 받지 않습니다.

기초 주식의 가치가 채권 구매일의 가치보다 25% 미만으로 떨어지면 원금, 소득 등이 영향을 받게 됩니다.

아래 예시를 확인해 보세요.

You’ll see that your 3% income yield will not be impacted UNTIL the underlying stock performance drops below the 25% threshold.

Structured notes can either be:

Structured notes give you an income stream and they typically protect you from the downside of market volatility.

If you want to take the risk and invest in structured notes, then check out Yieldstreet 👇

Yieldstreet is an online alternative asset investing platform for accredited investors.

As a reminder, accredited investors:

So, if you want to diversify your portfolio a little more and take a little extra risk, you might want to dabble in structured notes (although I suggest investing only what you can afford to lose).

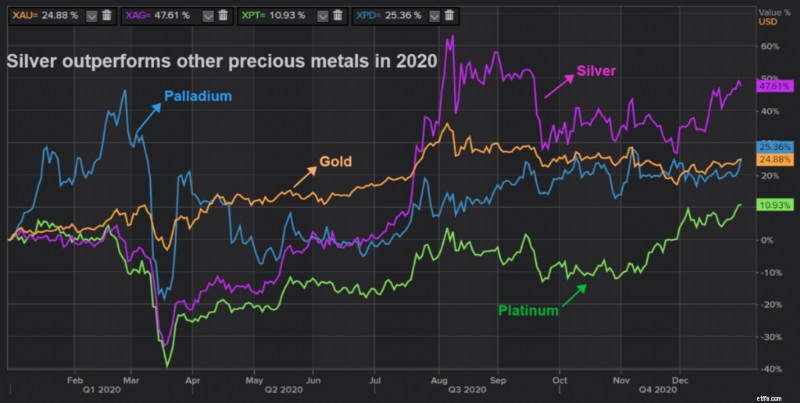

Another one of my favorite compounding interest investments is precious metals such as gold, silver, and platinum.

Each precious metal type performs differently, depending on market conditions.

Check out how silver, gold, and platinum performed back in 2020:

Based on the chart above, silver proved to be the top-performing precious metal.

Especially during difficult economic times, precious metals often aren’t as impacted by the market.

In fact, top financial professionals recommend their ultra-wealthy clients invest up to 10% of their net worth in precious metals.

Precious metals can help you:

Gold prices have also consistently outperformed inflation over the past almost 2 decades:

So if you’re looking to invest in precious metals like gold for as little as $1, now you can with OneGold 👇

OneGold is an online precious metals investment platform, where you can buy gold, silver, and platinum directly.

The precious metals are:

OneGold shared that in the past 50 years, gold has averaged a 10.9% return, while silver has averaged a 13.4% annual return.

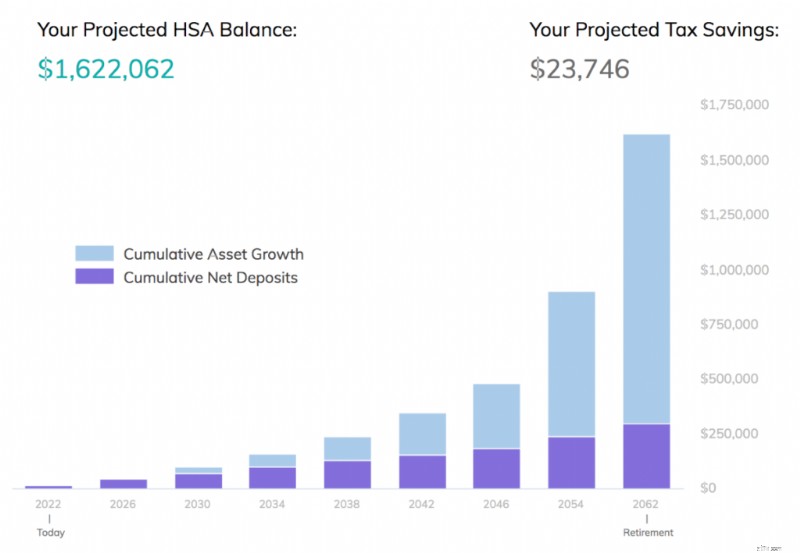

If you’re wondering how to earn compound interest, then you should also consider investing in your Health Savings Account.

A health savings account (aka HSA) is an investment account where you can set money aside, invest it, and use it for qualified medical expenses.

You want to use your HSA like another investment account and grow it for your retirement.

Check out how much money you could save in your HSA if you started contributing at 25 to age 65, earning an average 7% annual return:

That’s right – you could have over $1.6 MILLION saved in your HSA – and 100% of that could also be tax-free.

Ready to set up your own HSA?

(And no, you don’t need your employer to set up an HSA for you!).

Check out Lively’s award-winning HSA platform 👇

With Lively, you pay $0 to open your account – and you can choose how you want to invest:

HSAs are one of the best compound interest investments for the long term.

The earlier you start investing in your own retirement, the earlier you can become financially independent .

Not everyone gets this memo, however.

In fact, 1 in 3 of Americans reported they have $0 in retirement savings accounts.

Especially with 4-decade high inflation and wage stagnation, it’s more important than ever to start saving for retirement.

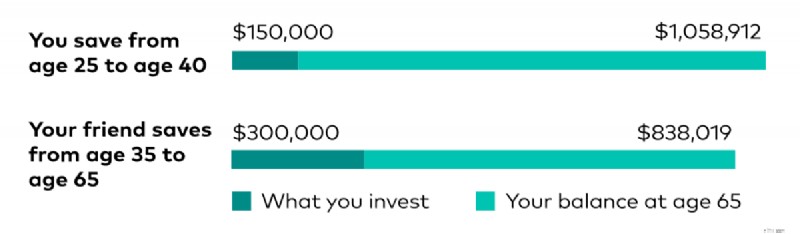

The key to building a successful retirement savings account is saving as early as possible.

In fact, the earlier you start saving, the more money you’ll have to spend during retirement. Check out this graph:

If you save $10,000 per year for just 15 years (and invest it with a 6% return), then you could have over $1 million dollars by the time you presumably retire at 65.

Compare that to starting your retirement journey at 35, saving $10,000 per year for 30 years, then you’d have just under $840,000.

That is the power of compound interest investments.

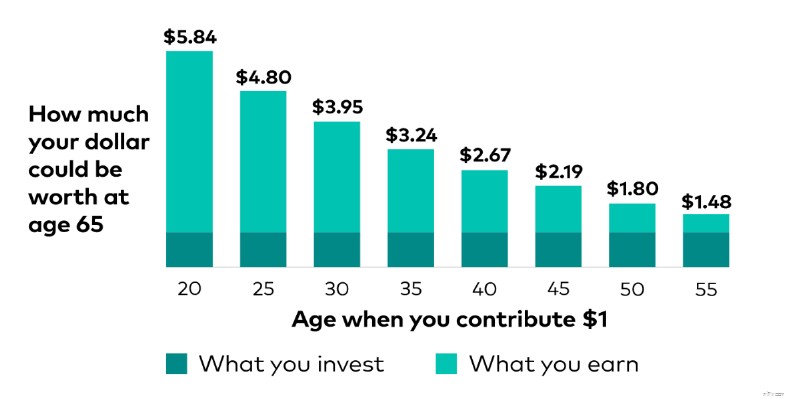

Now check out how much $1 could be worth by the time you retire – and it ALL depends on when you invest:

Compound interest is literally the eighth wonder of the world – just like Albert Einstein once said.

Are YOU ready to start investing for retirement?

Here’s how to get started:

Your retirement is no joke. Start preparing for it – now.

A self directed IRA (aka SDIRA) is an individual retirement account that can hold alternative investments that a typical IRA cannot.

An SDIRA could hold alternative assets like:

목록은 계속됩니다. So, if you like dabbling in alternative investments and earning a tax benefit, an SDIRA might be the right fit for you.

Ready to open an SDIRA? Then check out RocketDollar 👇

Opening an SDIRA with Rocket Dollar is actually pretty easy.

Just keep in mind that the same annual investment limit applies to SDIRAs as it does to traditional/Roth IRAs:

Another neat thing is that you can open a Roth SDIRA (so after-tax) or a Traditional SDIRA (pre-tax).

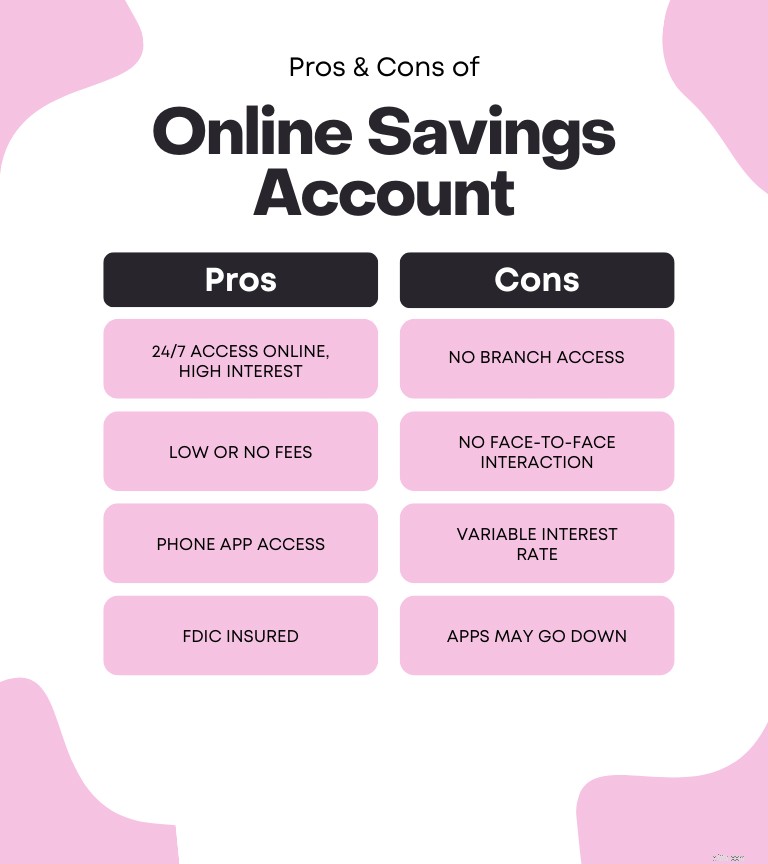

Learning how to get compound interest doesn’t have to be complicated. In fact, one of the best compound interest investments is a high yield savings account!

A high yield savings account (aka HYSA) gives you a much higher interest rate than your regular savings accounts.

One thing to note for this compound interest investment, however, is that most HYSAs are found online versus your brick-and-mortar stores.

The most important thing to remember is that the interest rates on the HYSA are variable.

Especially if you’re saving up (or already have) an emergency savings account, a HYSA can be a perfect fit.

So for example, if you need $3,000 to live per month, then your emergency savings fund should probably range between $9,000 to $18,000.

Especially if you’re saving up your first $10,000 in a year, then make sure to choose an HYSA to get the biggest bang for your buck.

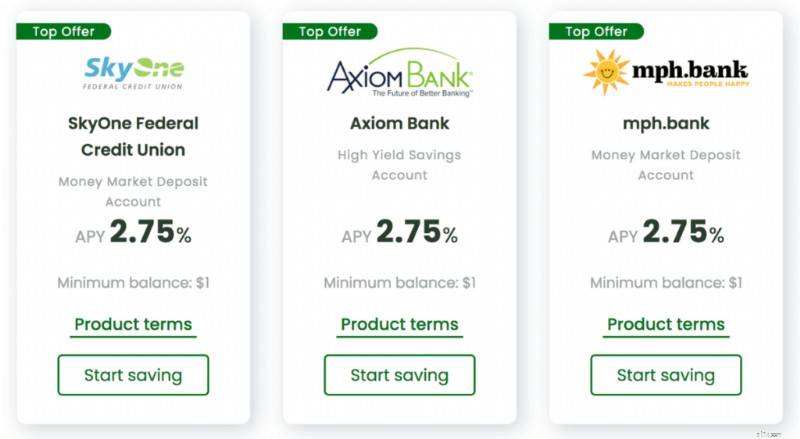

If you’re ready to put more money in your wallet, then I highly recommend checking out SaveBetter 👇

SaveBetter is a website that curates the highest-interest compound investment vehicles at the time of your search.

For example, in late 2022, Save Better displayed the top high yield savings investments:

And the best part about signing up to high yield savings accounts?

Almost all are 100% free to sign-up (and most don’t even charge maintenance fees). Just make sure you read the fine print!

If you’re ready to get the biggest bang for your buck, then check out SaveBetter now.

A money market account (aka MMA) is an interest-bearing account that is very similar to a high yield savings account.

However, there are 2 major differences between an MMA and an HYSA:

So in essence, an MMA combines checking and savings account characteristics.

The reason why MMAs are one of the best compound interest investments is that they offer higher interest rates than what you would earn in a regular savings account.

While MMA’s offer similar variable interest rates as do high yield savings accounts, there are 2 main downsides:

So, the best thing I can tell you is to read the fine print before you open an MMA.

You can find the best MMA accounts by going to SaveBetter .

A certificate of deposit (aka CD) is an account where you save money for a fixed period of time. During this time, you cannot withdraw the money and in return you earn a fixed interest rate.

The period of time in which your money is locked up in a CD varies, but typically is:

Typically, the longer you hold your money in a CD, the higher the interest rate. However, you’ll be sacrificing liquidity with a CD.

You might also give up your money’s purchasing power by sashing it as cash (meaning your money could be eaten up by inflation) versus investing the cash and earning returns higher than those offered by CDs.

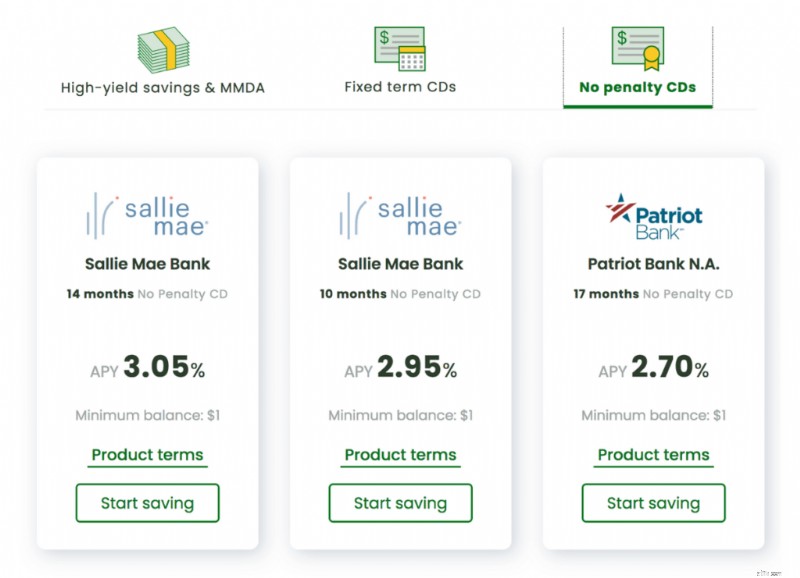

To get around the liquidity factor for CDs, you could always check out “no penalty CDs:”

Notice, however, that no penalty CDs offer much lower interest rates than traditional CDs… so at that point, it might just make sense to check out High Yield Savings Accounts (HYSAs), instead.

Here’s a good illustration of how a CD compares to an MMA and an HYSA:

Another one of my favorite compound interest investments is sports collectibles.

Thanks to alternative investment platforms like Collectable literally anyone can start investing in sports collectibles for as little as $5!

It’s possible to buy collectibles so cheaply thanks to fractional investing.

So, instead of owning the full card – or shoe, or belt, or picture, etc. – you’ll own a very small fraction of it.

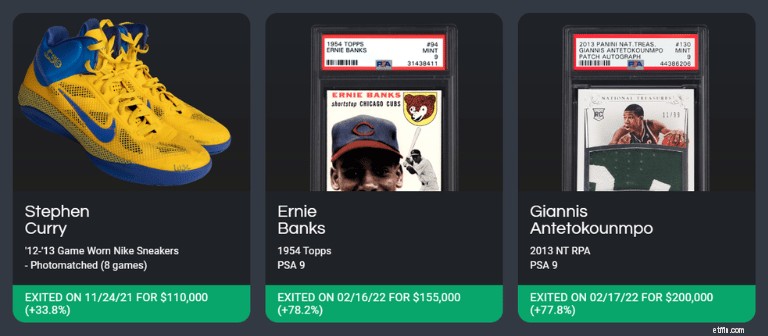

Here are some examples of sports collectibles you could own:

And here’s why sports collectibles could be a great compound interest investment:

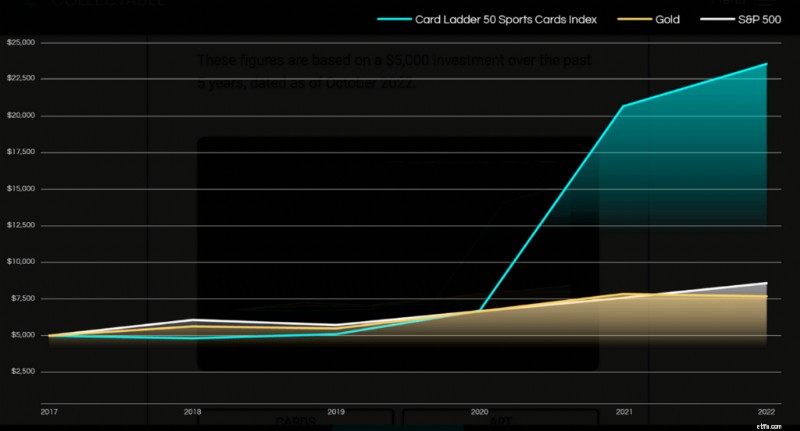

For example, sports collectibles (specifically sports cards) have massively outperformed both gold and the S&P, especially in the past few years:

The Collectable investment platform has, on average, exited sports collectibles with an average 60% ROI.

Compare the 60% return on investment to the average 7% to 9% average return on investment that you’d likely get with the stock market.

Another compound interest investment that could earn you potentially high returns and a passive income stream is peer-to-peer lending.

Peer-to-peer lending (aka P2P) is when you, along with hundreds of other private investors, lend money in exchange for repayment of your loan plus interest.

With P2P, you’re basically the bank:

With popular P2P platforms like Groundfloor , you can actually start lending with as little as $10.

Your loan would be borrowed by home flippers across the country.

As of the date of this article, you could make loans across 31 states in America:

The home flippers would use your money to:

Assuming all goes well, you should be repaid your initial loan plus interest. Typically, you could earn returns between 7% to 26%.

The loans you make are given “grades” ranging from A to G. Here’s an example of a loan that’s graded a “C.”

The closer the loans are graded to a “G” level, the higher the risk (and thus, the higher the potential return).

The closer the loans are graded to an “A” level, the lower the risk.

Just keep in mind that the biggest risk with P2P compound interest investments is that the people who borrow your money are much more likely to default on paying back your loan.

So make sure you only invest as much as you are willing to lose.

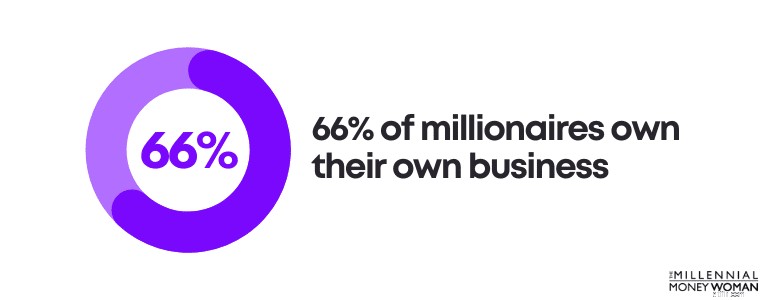

Investing in your business is arguably one of the best compounding investments.

Especially if you want to make money in the long run, becoming a business owner is your best bet.

And, it shouldn’t be a surprise that most millionaires are business owners.

In fact, about 66% of millionaires are business owners.

Building a business is like investing in a compounding interest account:

Here’s the best news:You don’t have to go to college and get an MBA for $100,000s to learn the ins and outs of business.

In fact, you can get an entire MBA packed in just 1 course from online platforms like Udemy 👇

Professor Chris Haroun, the creator of this course, taught at renowned schools like Stanford.

Now, in this MBA course , he gives you his knowledge from experiences including:

Here are some of the things you’d learn with the MBA course:

And the best part?

Instead of spending hundreds of thousands of dollars for an MBA, you can grab the course between $24 to $130.

While you might not be physically investing in a compounding interest vehicle, you can never go wrong in investing in your business and in yourself .

If you’re wondering how to invest with compound interest, then it’s also worth approaching this question from an “out-of-the-box” point of view.

Specifically, instead of opening an actual investment account, you should consider investing in yourself.

Undoubtedly, investing in yourself is one of the best long-term investments you can make, with virtually a 100% guaranteed return.

Do you feel stuck in your career?

Do you want to learn a new skill to make more money?

Then check out resources like Udemy 👇

Udemy is an online platform that offers courses to students worldwide.

For example, if you’re looking to switch to coding and make 6-figures, you might just want to check out some of Udemy’s top coding courses – with some starting at just $14.99.

The Bottom Line:

You can never go wrong with investing in yourself. The ROI you’ll get will be 10X the amount of money that you invested.

Do you want to be an early investor in the AI revolution?

Investing in AI startups before they go public could give you significant returns.

AI startups can also provide:

가장 좋은 점은 무엇인가요?

You don’t need $100,000s to start investing in AI startups.

With the Fundrise Innovation Fund , you can start investing in less than 5 minutes and with as little as $10.

(Most venture capital funds have a $200,000+ minimum).

The Innovation Fund invests in some of the world’s best tech companies.

Including those leading the AI revolution, before they go public.

Compounding interest investments can absolutely make you rich. In fact, the famous Albert Einstein once said “Compound interest is the eighth wonder of the world.”

Here’s how you can harness the power of compound interest:

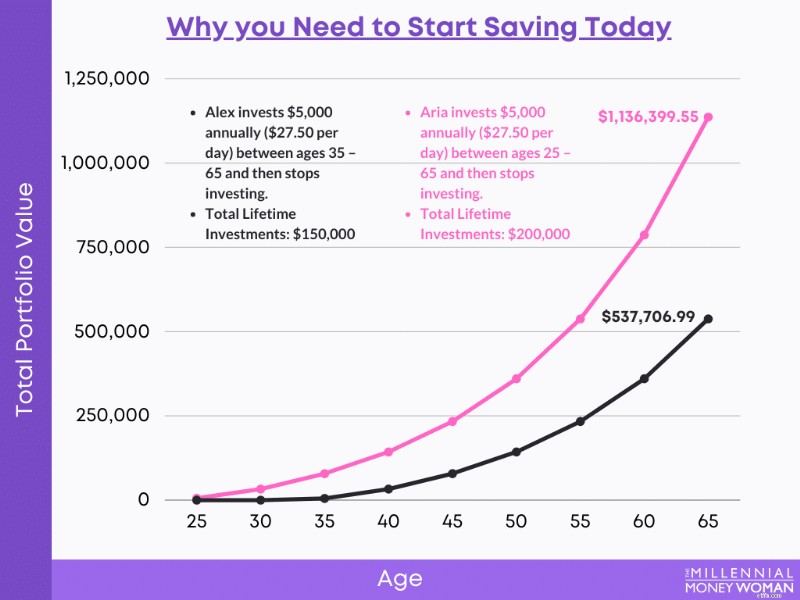

The key to getting rich from compound interest comes down to one thing:Time.

That’s why you need to invest when you are in your 20s – even if it’s just $100.

In fact, check out this chart below.

Aria’s 10 extra years of investing means that she has about $598,692.56 more than Alex.

Ultimately, learning how to invest in compound interest from an early age can lead to exponential growth in your wealth over time.

Investments that earn compound interest range in returns between 1% to 20% and higher. Examples of compound interest investments include a checking account, high yield savings account, certificate of deposit (CD), investment account, real estate investment account, and a small business investing account.

You can start building your compounding interest investments by opening a high yield savings account online or by starting an investment account. As soon as you put money into these accounts, compounding interest will start building your wealth over time.

Yes, compound interest is an investment that can grow your wealth exponentially in the future. However, if you decide to rack up debt (like credit card debt), then compound interest could work against you as well, because the interest will be applied to your unpaid loan balance.

Yes, banks offer compound interest accounts in many different forms. For example, you could open a high yield savings account, money market account, or a certificate of deposit (CD) which can compound daily.

One of the major disadvantages of compound interest is that it takes a very long time to see the benefit. In fact, it can take up to 10 years or longer before you start seeing the powerful impact of compounding interest, so maintaining a long-term mindset and accepting delayed gratification is key.

Investing money into the best compounding interest accounts can help you build a financial empire.

That’s because a compound interest account can make you money for free.

Hopefully this article gave you a peek into the best compounding interest investments such as:

Honestly, out of all the compound interest investments, my favorite is investing in index funds .

Of course, there is no right or wrong answer on how to invest in compound interest investments – you just have to consider your own personal situation and make a decision that works for you.