Backdoor Roth IRA를 설정하는 것은 혼란스러울 수 있으므로 사람들이 이 과정을 거칠 때 참조할 수 있는 단계에 대한 튜토리얼을 작성해야겠다고 생각했습니다. 시작해 보겠습니다.

백도어 Roth IRA란 무엇인가요?

누가 백도어 Roth IRA를 해야 하나요?

백도어 Roth IRA는 언제 해야 하나요?

백도어 로스 IRA 장단점

백도어 Roth IRA 세금 관련

백도어 로스 IRA 단계

백도어 Roth IRA 실수를 수정하고 예방하는 방법

백도어 Roth IRA FAQ

이름에도 불구하고 Backdoor Roth IRA는 계정이 아닙니다. 이는 두 단계로 구성된 프로세스입니다:

이 두 단계의 규칙을 이해하고 있다면 이를 통합하는 것은 문제가 되지 않습니다.

저소득자라면 Roth IRA에 직접 적립하고 이 백도어 Roth IRA 절차를 건너뛸 수 있다는 점을 기억하세요.

저소득자는 2024년 $146,000~$161,000(공동 신고 $230,000~$240,000)의 단계적 폐지 범위에 따른 수정 조정 총소득(MAGI)으로 정의됩니다. 레지던트, 직원 치과의사, 시간제 직원, 심지어 비소득자와 결혼한 저임금 전문의 일부 의료인 등 일부 문서는 Roth IRA에 직접 기부할 수 있습니다.

최소 $7,000(50세 이상인 경우 $8,000)를 버는 사람은 누구나 IRA에 $7,000(50세 이상인 경우 $8,000)를 기부할 수 있습니다 [2024] . 귀하의 소득이 MAGI $146,000-$161,000(Married Filing Jointly $230,000-$240,000) 미만인 경우 Roth IRA에 직접 적립할 수 있습니다. 직장에서 제공하는 은퇴 계획이 있고 MAGI가 $77,000-$87,000(부부 공동 신고 $123,000-$143,000) 미만인 경우 기존 IRA 기여금을 공제할 수 있습니다. 이 블로그의 독자 대부분은 직업을 통해 은퇴 계획을 갖고 있고 $240,000가 넘는 MAGI를 보유하고 있거나 곧 갖게 될 것이므로 Roth IRA에 직접 기부하거나 기존 IRA 기부금을 공제할 수 없다는 사실을 알게 될 것입니다. 따라서 최고의 IRA 옵션은 Backdoor Roth IRA 프로세스, 즉 간접적인 Roth IRA 기부입니다.

기혼 의사는 개인 및 배우자 Roth IRA를 사용해야 하며 일반적으로 두 가지 모두 간접적으로(즉, 백도어를 통해) 자금을 조달해야 합니다. 이는 과세 연도당 세금 보호 및 (대부분의 주에서) 자산 보호 공간을 각각 $7,000(50세 이상의 배우자는 $8,000) 추가로 제공하며, 은퇴 시 세금을 더 다양화할 수 있습니다. 세금 다각화를 통해 세금 이연(전통) 계좌에서 얼마를 가져갈지, 비과세(Roth) 계좌에서 얼마를 가져갈지 결정하여 은퇴자로서 자신의 세율을 결정할 수 있습니다. IRA는 INDIVIDUAL Retirement Alignment(개인 은퇴 준비)를 의미하므로 비례 규칙(아래 설명)에 따라 Backdoor Roth IRA를 수행하지 못하더라도 반드시 배우자가 수행하지 못하는 것은 아닙니다. 각 배우자는 별도의 8606으로 Backdoor Roth IRA를 보고하므로 Backdoor Roth IRA를 수행하는 부부의 세금 신고서에는 항상 두 개의 Form 8606이 포함되어야 합니다.

결혼 별도 신고(MFS)로 세금을 신고하는 경우 기여금 및 공제 소득 한도가 특히 낮습니다. 귀하(또는 귀하의 배우자)가 $0에서 $10,000 사이에서 퇴직 계획을 단계적으로 폐지할 자격이 있는 경우 Roth IRA에 직접 기여할 수 있는 능력과 기존 IRA 기여금을 공제할 수 있는 능력이 모두 제공됩니다. 기본적으로 MFS 세금을 신고하는 사람을 위한 최선의 선택은 Backdoor Roth IRA 프로세스, 즉 간접 Roth IRA 기부입니다.

실제로 배우자와 함께 거주하지 않는 경우에는 이러한 규칙에 예외가 있습니다. 이 경우 Roth IRA에 직접 기여할 수 있는 능력은 2024년 MAGI $146,000-$161,000 사이에서 단계적으로 사라집니다. 별도로 거주하고 직장에서 은퇴 계획의 적용을 받지 않는 경우 소득에 관계없이 기존 IRA 기여금을 공제할 수 있습니다. IRA 기여금이 부분적으로 또는 완전히 공제 가능한 상황에서도 Backdoor Roth IRA 프로세스를 수행할 수 있습니다. 세금 계산서는 정확히 동일합니다. 제대로 완료되면 $0입니다. 그러나 기여금이나 전환에 대한 세금 비용이 없는 대신 기여금에 대한 공제액이 전환에 대한 세금 비용과 정확하게 동일하므로 전체 과정에 대해 동일한 $0 세금 청구서가 생성됩니다.

Mega Backdoor Roth IRA는 일반 Backdoor Roth IRA와 완전히 다릅니다. 이름에도 불구하고 실제로는 IRA가 아닌 401(k)로 Mega Backdoor Roth IRA를 수행합니다. 세후(Roth 아님) 직원 기여금을 모두 허용하고 근무 중 인출(Roth IRA로 전환) 또는 보다 일반적으로 계획 내 전환을 허용하는 401(k)가 필요합니다. Mega Backdoor Roth IRA 프로세스를 사용하면 최대 $69,000(50세 이상인 경우 $76,500)까지 넣을 수 있습니다. [2024] 매년 Roth 401(k)(또는 평소 기부금 $7,000-$8.000에 추가하여 Roth IRA)로 적립됩니다. 그러나 이 프로세스는 이 게시물에서 논의하고 있는 Backdoor Roth IRA 프로세스와는 아무런 관련이 없습니다.

많은 사람들이 Backdoor Roth IRA의 시기에 대해 궁금해합니다.

Backdoor Roth IRA 프로세스를 충족할 수 있는 마감일은 실제로 단 하나뿐입니다. 특정 과세 연도에 대한 IRA 기부금은 해당 과세 연도의 1월 1일부터 다음 연도의 4월 15일(연장을 신청한 경우에도) 사이에 이루어져야 합니다.

변환 단계는 언제든지 발생할 수 있습니다. 기부가 이루어진 다음 날 또는 심지어 당일에 이루어질 수도 있습니다. 권장하지는 않지만 기여와 전환 단계 사이에 몇 달, 몇 년, 심지어 수십 년을 기다릴 수 있습니다. Roth 전환에는 마감일이 없습니다. 비례 배분 규칙을 피하기 위해 롤오버 또는 기존, 롤오버, SEP 또는 SIMPLE IRA의 전환을 수행해야 하는 경우 해당 연도 12월 31일까지 전환 단계를 수행해야 합니다.

가능한 한 빨리 두 단계를 모두 수행해야 합니다. 많은 화이트 코트 투자자들은 매년 1월 첫째 주에 IRA 기부 단계와 Roth 전환 단계를 수행합니다. 이는 해당 달러에 발생할 수 있는 면세 복리의 양을 최대화합니다. 기여와 전환 사이의 시간을 최소화하고 연도 내에 두 단계를 모두 수행하는 것이 필수는 아니지만 서류 작업이 확실히 단순화됩니다.

서류 작업을 정말 복잡하게 만들고 싶나요? 매달 IRA에 기부하고 매달 전환하세요. 그런 다음 매년 추적할 12개의 기여와 12개의 전환이 있습니다. 하지만 Backdoor Roth IRA 프로세스를 통해 Roth IRA에 기부해야 할 만큼 충분한 돈을 벌면 매년 한 번만 기부해도 충분합니다.

그렇습니다. 제 아내와 저는 2010년부터 매년 한 번씩 해왔고 더 이상 근로 소득이 없을 때까지 중단할 계획이 없습니다. 이는 우리가 1년에 한 번 수행하는 투자 업무 중 하나일 뿐입니다.

Backdoor Roth IRA를 더 일찍 시작하게 만드는 요인 중 하나는 5년 규칙입니다. 이제 IRA와 관련된 5년 규칙이 최소 3개 이상 있는데, 여기서 가장 주목해야 할 것은 Roth 전환 후 5년 규칙입니다. 이 규칙은 59 1/2세 이전에 계좌에서 원금을 인출하는 경우 벌금이 면제되는지 여부를 결정합니다. 5년의 기간은 전환을 수행하는 해의 1월 1일에 시작되므로 5년이 조금 안 될 수 있습니다. Roth IRA 원금은 일반적으로 세금과 벌금이 면제되지만(과태료가 부과될 수 있는 소득만 해당), 이는 5년 규칙이 충족된 후에만 해당됩니다.

본질적으로, 51세에 Roth IRA를 전환하면 59 1/2세가 아닌 56세부터 세금 및 벌금 없이 원금을 인출할 수 있습니다. 이를 통해 조기퇴직자들의 생활비를 조달할 수 있다. 57세에 Roth 전환을 하면 59 1/2세가 되어도 세금 및 벌금 없이 해당 원금(및 수입)을 이용할 수 있습니다. 따라서 5세 또는 59 1/2세 중 먼저 도래하는 것이 적용됩니다.

IRA 기부금에 대해 완전히 별도의 5년 규칙이 있지만 이는 모든 기부가 아닌 첫 번째 IRA 기부를 할 때부터 시작되므로 대부분의 조기 퇴직자에게는 적용되어서는 안 됩니다.

Backdoor Roth IRA에는 좋은 점이 많이 있지만 복숭아와 크림만 있는 것은 아닙니다.

Backdoor Roth IRA의 주요 이점은 또 다른 은퇴 계좌를 제공한다는 것입니다. Backdoor Roth IRA 프로세스를 통해 수입이 Roth IRA 직접 기부에 대한 소득 한도를 초과한 후에도 Roth IRA에 계속 기부할 수 있습니다. 퇴직 계좌는 과세 대상 또는 부적격 계좌에 적용되는 세금 부담을 제거하여 세금을 줄이고 투자가 더 높은 비율로 증가하여 목표를 더 빨리 달성할 수 있도록 해줍니다.

과세 계정과 비교하여 해당 세금 보호의 가치는 얼마나 됩니까? 이는 기본 투자의 수익, 세금 효율성 및 자금이 계좌에 남아 있는 기간에 따라 달라집니다. 한계 세율로 50년 동안 세금이 비효율적인 투자로 8%의 수익을 올린 $10,000는 Roth IRA에서는 $469,000로 증가하지만 과세 계정에서는 $88,000에 불과합니다. 보다 현실적으로, 30년 이상 동안 세금 효율적인 투자를 위해 Roth IRA와 과세 계정을 사용하면 여전히 29% 더 많은 돈을 벌 수 있습니다.

퇴직 계좌는 간단한 자산 계획을 보장합니다. 수혜자를 이용하면 해당 자금이 검인 절차를 거치지 않으므로 상속인은 번거로움을 덜고 개인 정보 보호를 강화하며 비용 없이 더 빨리 자금을 얻을 수 있습니다. 그들은 계정을 상속받은 후 10년 동안 세금 보호 성장 혜택을 연장할 수도 있습니다. Roth IRA와 같은 퇴직 계좌는 대부분의 주에서 실질적인 자산 보호를 제공합니다. 즉, 매우 드물게 정책 제한을 초과하는 판결이 항소 시 감소되지 않는 경우 파산을 선언하고 퇴직 계좌에 있는 자산을 계속 유지할 수 있음을 의미합니다. 로스 머니는 영원히 세금이 면제되므로 매년 계속 기부하면 은퇴 시 세금 다각화를 늘릴 수 있습니다.

Roth IRA는 백도어 Roth IRA 프로세스를 통해 적립하더라도 여전히 모든 단점이 있는 은퇴 계좌입니다. 퇴직 계좌는 투자할 수 있는 투자를 제한하고 마진 투자의 사용을 금지합니다. 승인된 예외 없이 59 1/2세 이전에 Roth IRA 수입을 인출하는 경우 10%의 벌금이 부과됩니다.

비례 규칙(아래 참조)으로 인해 Backdoor Roth IRA 프로세스에서는 기존 IRA, SEP-IRA 및 SIMPLE IRA를 401(k)로 전환하거나 롤오버해야 합니다. 자영업 소득이 있는 경우 SEP-IRA 대신 단독 401(k)을 사용하여 해당 소득을 세금으로부터 보호해야 합니다. 매년 Backdoor Roth IRA를 수행하면 세금 신고서에 배우자당 하나의 양식(IRS 양식 8606)이 추가됩니다. 세금 소프트웨어를 사용하여 세금을 직접 준비하는 경우 소프트웨어가 프로세스를 올바르게 보고하는지 확인하는 것이 까다로울 수 있습니다. 최고 소득 연도 동안 세금 유예 계좌를 최대한 활용하는 대신(추가가 아닌) Backdoor Roth IRA를 수행하는 경우에도 돈이 덜 축적되는 실수가 될 수 있습니다.

아마도 가장 중요한 점은 매년 Roth IRA에 돈을 입금하는 데 단 한 단계가 아닌 두 단계가 있다는 것입니다. 나는 그 과정이 매우 간단하다고 생각하지만, 의사들이 그 과정을 망칠 수 있는 모든 독특한 방법에 계속해서 놀랐습니다. 이 기사 후반부에서 이러한 모든 문제를 해결하는 방법을 보여 드리겠습니다.

예! 대부분의 경우. 비례 배분 규칙을 피하기 위해 다른 IRA를 먼저 처리해야 하는 경우 첫 해에 약간의 추가 번거로움이 있을 수 있지만 실제로는 매년 수행하는 것이 약간 번거롭습니다. 누군가가 큰 전통적 IRA를 가지고 있는데 Roth IRA로 전환할 여력이 없고 401(k)가 전혀 없거나 401(k)가 높은 수수료를 부과하거나 IRA 자산이 401(k) 내에서 투자할 수 없는 것에 투자되었기 때문에 401(k)로 롤오버할 수 없는 경우가 있을 수 있습니다. 고용주가 제공한 퇴직 계좌가 SIMPLE IRA 또는 SEP-IRA인 경우 Backdoor Roth IRA 프로세스도 그만한 가치가 없을 것입니다. 마지막으로, 일부 억만장자들은 Roth 계좌에 연간 7,000~16,000달러를 추가로 벌어들이는 것만으로는 바늘을 움직일 수 없기 때문에 Backdoor Roth IRA 프로세스의 사소한 번거로움에도 신경쓰고 싶어하지 않습니다.

Roth IRA는 소득에 대한 과세를 피하는 것이 목적이므로 당연히 이 과정에는 많은 세금 관련 영향이 있습니다.

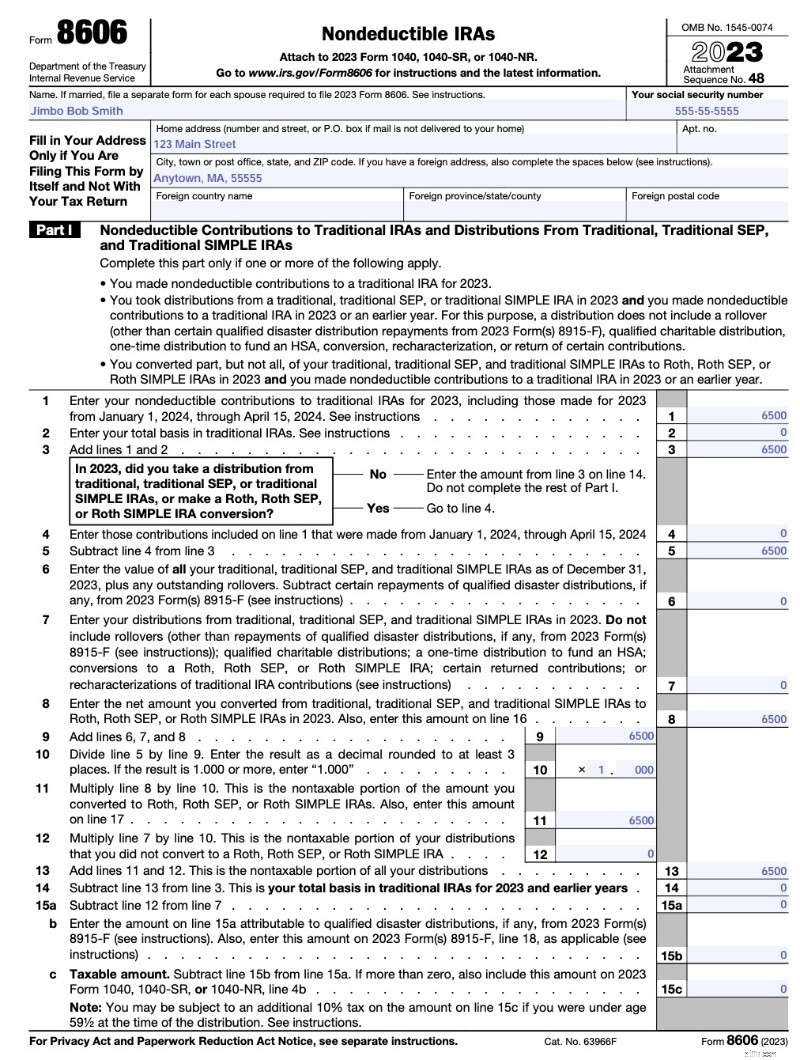

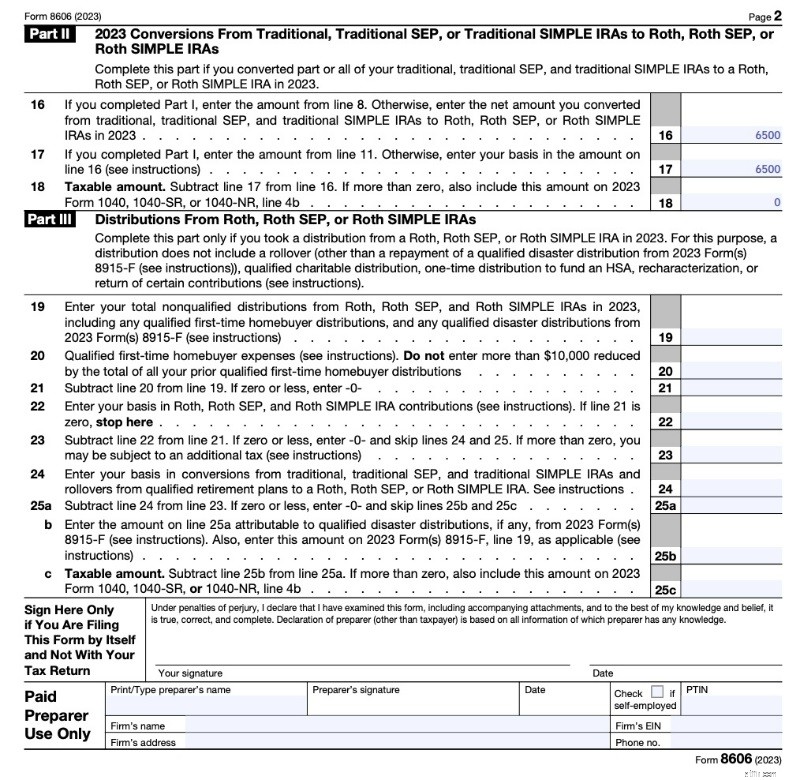

알아야 할 가장 중요한 세금 관련 사항은 비례 규칙입니다. 나는 Backdoor Roth IRA 문제의 90% 이상이 투자자의 전환을 비례 배분하는 것과 관련이 있다고 추정합니다. IRS 양식 8606(아래 참조)으로 Roth IRA 전환을 보고할 때 비례 계산이 이루어집니다. 분자는 환산된 금액입니다. 분모는 모든 Traditional, Rollover, SEP 및 SIMPLE IRA의 합계이지만 401(k), 403(b), 457(b), Roth IRA 또는 상속된 IRA는 아닙니다. 따라서 세후 금액을 Roth로 전환하는 해의 12월 31일 이전에 보유하고 있는 IRA 잔액으로 무언가를 하는 것이 중요합니다. 이 기사 후반부에서 이 돈을 어떻게 사용할 것인지에 대한 정확한 옵션을 설명하겠습니다.

올바르게 수행하면 Backdoor Roth IRA 전환에 세금이 부과되지 않습니다. 영. 나다. 제로. Roth IRA에 넣은 돈(이 경우 백도어를 통해 간접적으로)은 돈을 벌 때 과세되지만 Roth IRA에 직접 기부하거나 공제 불가능한 IRA 전환으로 기부하거나 나중에 해당 돈을 Roth IRA로 전환하는 경우에는 과세되지 않습니다. 실제로 다시는 세금이 부과되지 않습니다.

Step Transaction Doctrine이라는 IRS 규정으로 인해 IRS가 Backdoor Roth에 문제를 일으킬 것이라는 우려가 있었습니다. 이 규칙은 기본적으로 여러 법적 단계의 합이 불법이라면 그렇게 할 수 없다는 것을 의미합니다. 어떤 사람들은 Traditional IRA에서 Roth로의 백도어 전환이 이 원칙을 고려한 합법적인 거래인지 궁금해했습니다. 타당하든 그렇지 않든 이러한 우려는 더 이상 문제가 되지 않습니다. IRS는 2018년 초 Backdoor Roth IRA의 기부 단계와 전환 단계 사이에 대기 기간이 필요하지 않다고 밝혔습니다. 그것은 본질적으로 전체 과정에 축복을 주었습니다. Pennies와 Backdoor Roth IRA에서 논의한 것처럼 기다리는 것은 8606의 상황을 더욱 복잡하게 만듭니다.

TurboTax에서 Backdoor Roth IRA를 올바르게 신고하는 것은 불행하게도 양식 8606을 직접 작성하는 것보다 훨씬 더 복잡합니다. 이를 올바르게 수행하는 열쇠는 소득 섹션에서 전환 단계를 보고하지만 공제 및 세액공제 섹션에서 기여 단계를 보고한다는 것을 인식하는 것입니다. 일반적으로 소득구간을 먼저 하기 때문에 실제로 전환 이전에 기부를 하였더라도 기여신고를 하기 전에 전환신고를 하게 됩니다. 마지막에는 회계사가 작성한 양식을 확인하는 것처럼 TurboTax가 생성하는 양식 8606을 살펴보고 싶을 것입니다.

자세한 내용은 여기를 참조하세요.

TurboTax에서 백도어 Roth IRA를 신고하는 방법

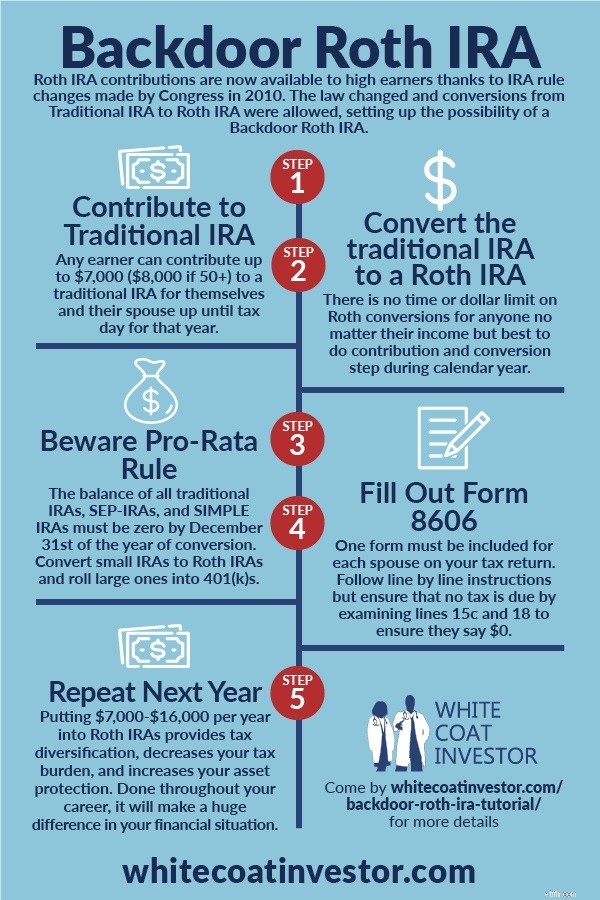

이 섹션에서는 Backdoor Roth IRA 프로세스를 수행하는 방법과 종이로 제출하든 세금 소프트웨어를 사용하든 세금 신고서에 보고하는 방법을 정확하게 설명합니다. Vanguard에서 Backdoor Roth IRA 단계를 쉽게 거치거나, Fidelity에서 Backdoor Roth를 완료하거나, 가장 인기 있는 중개/뮤추얼 펀드 회사 세 곳인 Schwab에서 Backdoor Roth IRA를 완료할 수 있습니다.

실제로는 2단계 프로세스에 불과하지만 6단계 프로세스로 생각하는 것이 가장 좋습니다. 이 단계를 모두 순서대로 수행할 필요는 없지만(1단계 전에 3단계를 수행하는 것이 더 쉬울 수 있음), 모두 수행해야 합니다.

본인과 배우자를 위해 $7,000(50세 이상인 경우 $8,000)의 비공제 전통 IRA 기여금을 만드십시오. 매년 동일한 기존 IRA 계좌를 사용할 수 있습니다. 대부분의 시간을 $0으로 보냅니다. 뱅가드를 비롯한 대부분의 펀드회사는 계좌에 아무것도 없다고 해서 계좌를 폐쇄하지 않습니다. 저는 매년 1월 2일에 이 일을 합니다.

물론 전통적인 IRA와 같은 계좌는 투자가 아닙니다. 여행가방이 옷이 아닌 것처럼요. 전통적인 IRA에 돈을 넣을 때 IRA 제공자에게 투자 방법도 알려야 합니다. 이런 경우에는 머니마켓펀드든 결제펀드든 현금으로 남겨두시면 됩니다. Vanguard에서 결제 기금은 Federal Money Market Fund입니다. 기부와 전환 단계 사이에 이익(또는 특히 손실)이 발생하는 것을 원하지 않는 이유는 서류 작업이 더 복잡해지기 때문입니다. 이익을 최소화하는 가장 좋은 방법은 현금으로 남겨두는 것입니다(물론 기부 후 가능한 한 빨리 전환을 수행하여 '페니' 문제를 최소화하는 것).

다음으로, 동일한 펀드 회사에서 기존 IRA의 돈을 Roth IRA로 이체하여 공제가 불가능한 기존 IRA를 Roth IRA로 전환하세요. Roth IRA가 아직 없다면 개설해야 합니다. 이는 Vanguard에서 온라인으로 1~2분 안에 완료할 수 있으며 기본적으로 기존 IRA를 개설하는 것과 동일한 프로세스입니다. 저는 기부를 한 다음 날 바로 이 일을 합니다. 매우 간단합니다. 돈을 이체하면 웹사이트에 “이것은 과세 대상 이벤트입니다”라는 무서운 배너가 표시됩니다. 그건 사실이에요. 과세 대상입니다. 하지만 이미 $7,000에 대해 세금을 납부했고 돈을 너무 많이 벌기 때문에 기부금 공제를 청구할 수 없었기 때문에 세금 계산서가 0이 됩니다. 기본적으로 1단계 직후에 3단계를 수행할 수 있습니다. 일부 회사에서는 당일에 수행하도록 허용합니다. 다른 회사에서는 다음 날 또는 일주일 정도 기다리게 합니다. 하지만 이를 위해 몇 달을 기다릴 이유가 없습니다.

이제 Roth IRA에 투자할 자금을 선택해야 합니다. 이미 투자한 금액이 있다면 7,000달러만 추가하면 됩니다. 그렇지 않은 경우 서면 투자 계획에 따라 투자를 선택해야 합니다. 아직 서면 투자 계획이 없다면 재정 계획의 일부가 이루어질 때까지 돈을 현금으로 남겨두거나 Target Retirement 2050 펀드나 다른 라이프사이클 펀드에 넣어두세요.

SEP-IRA, SIMPLE IRA, 기존 IRA 또는 롤오버 IRA 금액을 없애세요. Backdoor Roth IRA의 혜택을 대부분 제거할 수 있는 "일할 계산"(양식 8606의 6행 참조)을 피하기 위해 전환 단계(2단계)를 수행한 해 12월 31일에 해당 계좌의 총 합계는 0이어야 합니다.

이러한 IRA 계좌는 세 가지 방법으로 제거할 수 있습니다:

Backdoor Roth IRA의 다음 부분은 몇 달 후 귀하(또는 귀하의 회계사)가 세금에 대한 IRS 양식 8606을 작성할 때 완료됩니다. 잊지 마세요. 그렇지 않으면 $50의 벌금이 부과됩니다. 각 배우자에 대해 개별 은퇴 준비 양식이 필요하다는 점을 기억하십시오. 이 부분을 망치는 것을 피하기 위해 전문가를 고용하더라도 제대로 수행되었는지 다시 확인해야 합니다. 고문들은 세금 대리인이 부적절하게 수행한 수십 가지 문제를 고객이 해결하도록 도와야 한다고 말했습니다. 제대로 하지 않으면 Backdoor Roth IRA 기부금에 대해 세금을 두 번 납부하게 됩니다.

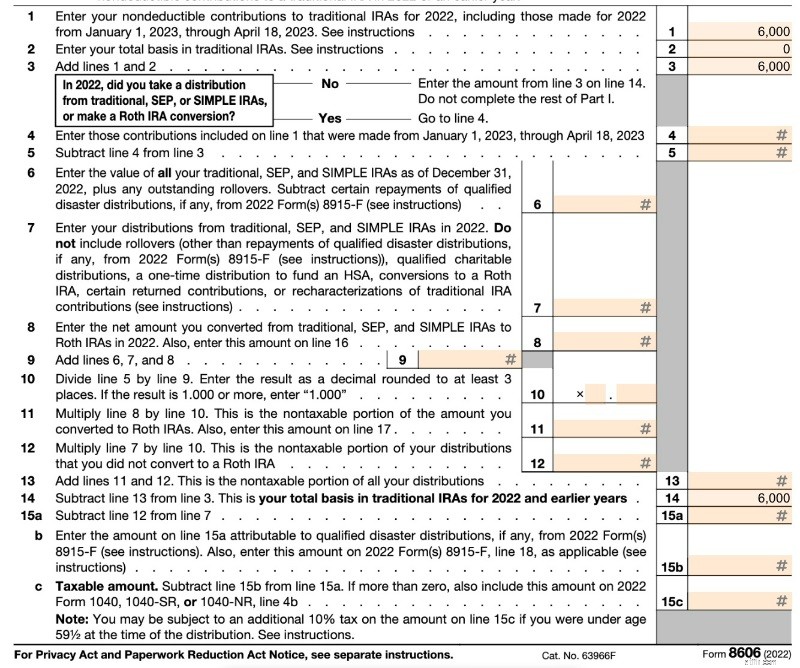

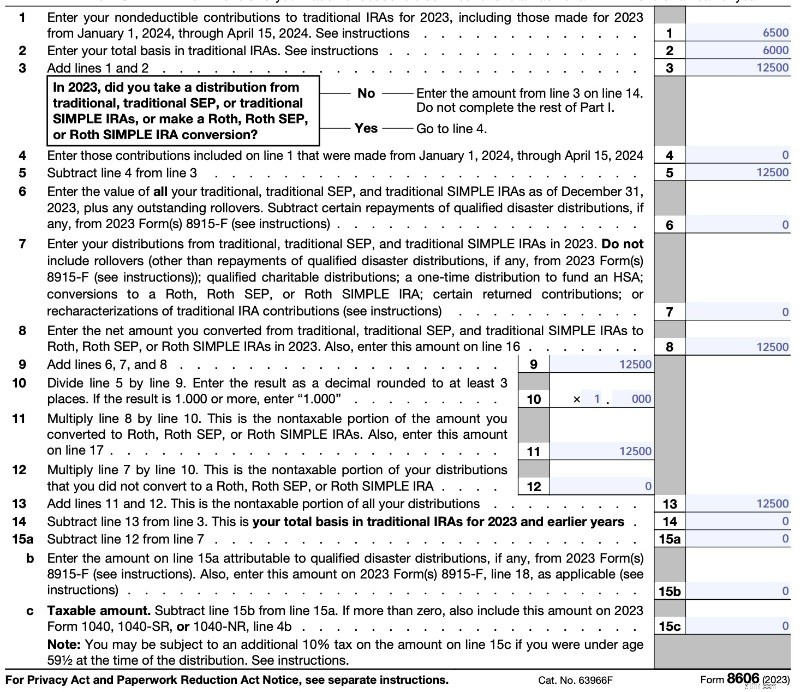

1페이지(아래)에는 공제되지 않는 IRA의 "분배액"이 나와 있습니다. 해당 금액에 이미 세금이 부과되었으므로 분배금에 대한 과세 금액은 0입니다. 1행은 귀하의 공제되지 않는 기여금입니다. 2행에서는 작년 12월 31일에 기존 IRA에 돈이 없었기 때문에 귀하의 기준은 0입니다(수년간 비공제 IRA를 보유하고 있었다면 이는 0이 아닐 수 있습니다). 6행은 일반적인 연도에 0입니다. TurboTax가 이를 약간 다르게 채울 수 있지만(6-12행을 비워 둘 수 있음) 결과는 동일합니다. 13행은 3행과 동일하므로 납부해야 할 세금은 0입니다.

다음은 양식 8606의 2023년 버전의 예입니다.

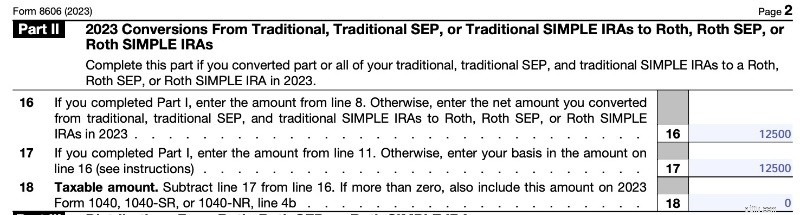

2페이지(아래)에는 Roth 변환이 표시되어 있습니다. 왜 이 작업을 두 번 수행해야 하는지 잘 모르겠습니다(8행과 11행의 금액을 이체한 다음 빼기 때문입니다). 그러나 이것이 양식에서 요구하는 것입니다. 보시다시피, 이익 없이 공제가 불가능한 기존 IRA 기여금을 Roth로 전환하는 것은 과세 대상입니다. 단지 세금 계산서가 0일 뿐입니다.

세무 대리인의 작업을 다시 확인할 때 2행, 14행, 15c행 및 18행에 집중하여 0과 같이 매우 적은 금액이고 $7,000와 같이 너무 큰 금액이 아닌지 확인하는 것이 좋습니다. 동시에 다른 Roth 변환을 수행하거나 전년도에 기여한 경우(예:2022년 기여를 2023년에 기여한 경우) 양식이 더 복잡해질 수 있습니다. 자세한 내용은 아래를 참조하세요.

양식에 기여한 날짜나 전환한 날짜를 입력할 공간이 없다는 점에 유의하십시오. IRA 관리인이 IRS(1099-R)에 보내는 양식에도 없습니다.

기여와 전환 사이에 일정 기간을 기다릴 필요가 없습니다. 매년 1월 2일에 Traditional IRA에 기부한 후 다음 날 또는 며칠 내에 Roth IRA로 전환합니다. 그러면 투자 자금이 최대한 빨리 작동하고 기록 보관이 단순화됩니다. Vanguard에서는 당일에 하도록 허용하지 않으므로(때때로 다른 제공업체에서는 허용함) 어쨌든 하루 기다려야 합니다. 때로는 최대 일주일까지 기다리게 만드는 경우도 있습니다. 계좌에 몇 센트가 남아 있고 비례 배분을 받을까 봐 걱정된다면 다음 게시물을 살펴보세요:Pennies and the Backdoor Roth IRA.

자세한 내용은 여기를 참조하세요.

Vanguard와 함께 백도어 Roth IRA를 수행하는 방법

Fidelity에서 백도어 Roth IRA를 수행하는 방법

이 섹션에서는 Backdoor Roth IRA 프로세스에서 흔히 발생하는 실수를 수정하고 예방하는 방법에 대해 설명하겠습니다. 이러한 실수를 더 잘 정리하기 위해 프로세스를 위에서 사용된 6가지 매우 명확한 단계로 분류한 다음 각 단계에서 발생할 수 있는 오류와 이에 대한 조치를 설명할 것입니다.

진지하게. 그게 다야. 담낭절제술을 할 수 있다면 이렇게 해도 됩니다. 폐색전증을 적절하게 치료할 수 있다면 이렇게 할 수 있습니다. 고혈압을 잘 관리할 수 있다면 이렇게 할 수 있습니다. 구멍을 채울 수 있다면 이렇게 할 수 있습니다. 아주 쉽습니다.

그러나 사람들은 여전히 이 6단계 각각을 망쳐버리고 있습니다. 사람들이 저지르는 실수를 단계별로 살펴보겠습니다.

첫 번째 백도어 Roth IRA에서 흔히 발생하는 오류는 사람들이 자신의 소득이 Roth IRA에 직접 기부하기에는 너무 높다는 사실을 깨닫지 못한다는 것입니다. 한도 미만이더라도 별 문제가 되지 않는 간접적인 방법(예:백도어 통과) 대신 Roth IRA에 직접 기여합니다. 그런 다음 그들은 수정 조정 총소득(MAGI)이 2024년 $146,000-$161,000(공동 부부 신고 합산 $230,000-$240,000) 이상이라는 것을 알게 됩니다. 이제 어떻게 될까요?

이 오류를 범했다면 이제 Roth IRA 기부금을 기존 IRA 기부금으로 다시 특성화해야 합니다. 이는 기본적으로 Roth IRA에 기여한 적이 없지만 대신 전통적인 IRA에 기여한 것처럼 만듭니다. 이 작업을 수행하려면 일반적으로 IRA 제공업체에 전화해야 하지만 큰 문제는 아닙니다. 이 섹션에서는 자세한 방법을 안내해 드리겠습니다.

세금 신고 마감일까지 이 작업을 수행해야 합니다(연장 포함). 따라서 2023년 과세 연도에 대해 2023년 1월에 IRA 기부금을 납부한 경우 2024년 10월 15일까지 재특성화를 수행해야 합니다. 패널티나 할 일이 없습니다. 기존 IRA에 기부했지만 Roth IRA에 직접 기부할 예정이라면 반대의 경우도 가능합니다.

2018년부터 더 이상 Roth CONVERSIONS(기여 아님)의 재특성화를 수행할 수 없다는 점을 명심하세요. 이로 인해 세금 감면을 위한 "Roth IRA 전환 경마" 기술이 제거되었습니다.

불과 몇 년 전까지만 해도 저는 성격 변경 후 그 돈을 Roth IRA로 다시 전환하기까지 대기 기간이 있다고 생각했습니다. 그러나 해당 규칙은 기여가 아닌 전환의 재특성화에만 적용되었습니다. 특성 변경을 기다리는 기간은 한 번도 없었습니다.

물론 최종 전환 이전에 발생한 모든 이득은 최종 전환 연도의 일반 소득세율로 전액 과세됩니다.

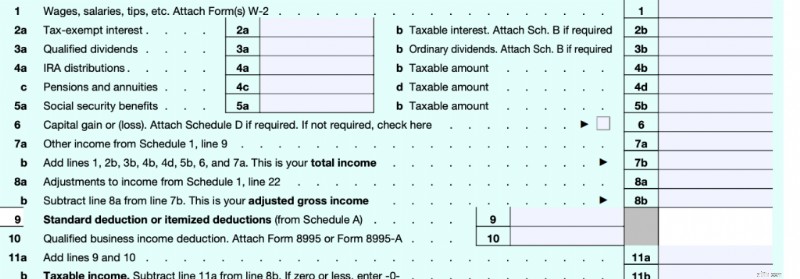

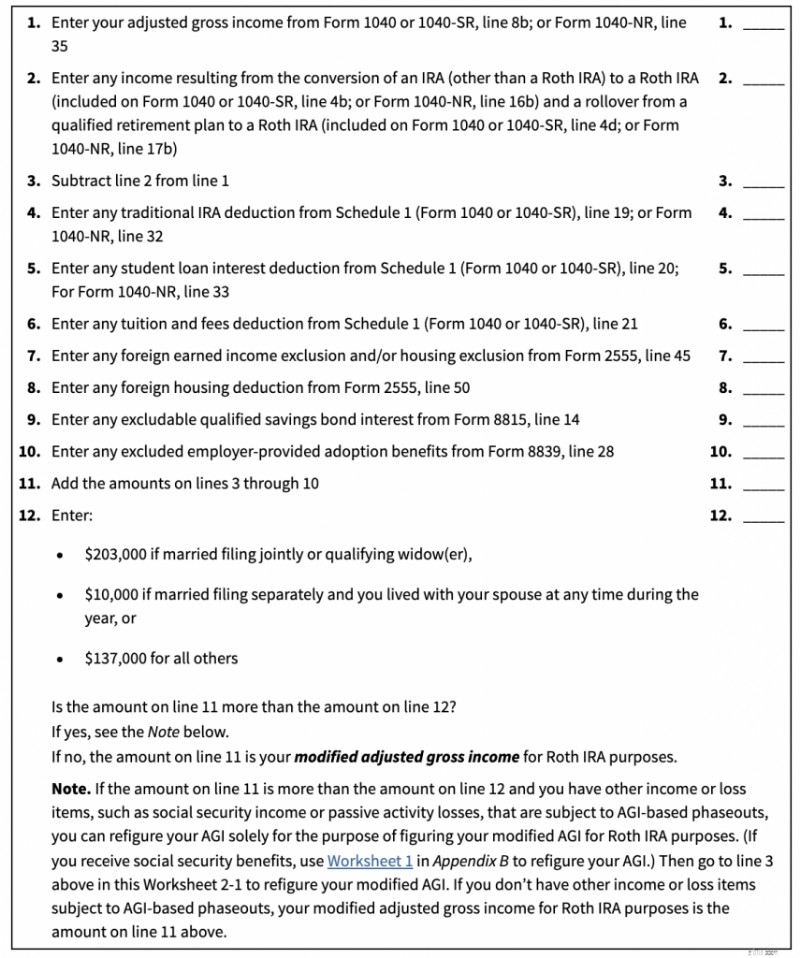

가장 먼저 결정해야 할 것은 이 게시물이 귀하에게도 적용되는지 여부입니다. 소득이 일정 금액 미만인 경우 Roth IRA에 직접 적립할 수 있습니다. 그 금액은 여러 가지에 따라 달라집니다. 첫째, 수정 조정 총소득(MAGI)입니다. 이 수치는 조정 총소득(AGI)과 매우 유사합니다. 세금 양식 1040이 어떻게 작동하는지 기억하세요.

첫 번째 소득 라인은 7b행, 즉 “총 소득”입니다. 사람들이 소득에 대해 생각할 때, 일반적으로 이것이 그들이 생각하는 것입니다. 양식의 세 번째 소득 항목은 11b행입니다. 이것이 귀하의 “과세 소득”입니다. 이것이 실제로 세금 계산서가 계산되는 내용입니다. 기본적으로 총 수입에서 모든 공제액을 뺀 금액입니다. 이 둘 사이의 8b행에는 또 다른 소득, 즉 “조정 총소득”이 있습니다. 사람들이 '선 위 공제', '선 이하 공제'라는 표현을 쓸 때 말하는 '선'이 바로 이것이다. AGI가 계산되기 전에 나오는 경우에는 최고 수준의 공제입니다. 여기에는 자영업 세금, 자영업 퇴직 계획, 자영업 건강 보험료, HSA 기여금, 학자금 대출 이자, 위자료, 수업료 및 IRA 공제와 같은 공제가 포함됩니다. AGI를 계산한 후에 나오면 최저선 이하 공제입니다. 이는 표준 공제 또는 모기지 이자, 주/지방/재산세 및 자선 기부금과 같은 항목별 공제입니다. MAGI는 AGI를 약간만 조정한 것일 뿐입니다.

다음은 Roth IRA 직접 기부에 대한 MAGI 한도입니다. [2024] . MAGI가 첫 번째 숫자보다 낮으면 Roth IRA에 직접 기부할 수 있습니다. MAGI가 두 번째 숫자를 초과하면 전혀 기여할 수 없습니다. 귀하의 MAGI가 두 숫자 사이에 있다면 부분적으로 직접 기여할 수 있습니다(대부분은 이 일에 신경쓰지 말고 백도어를 통해 모두 하십시오).

첫 번째 숫자에 가까운 위치에 있을 것이라고 생각한다면, 백도어를 통해 간접적으로 Roth IRA 기여를 하십시오(기존 IRA에 기여한 다음 해당 기여를 Roth IRA로 전환). 2010년 이후 Roth 전환에는 소득 제한이 없었으며 기존 IRA 기부금에도 소득 제한이 없었습니다. 단지 공제 가능 여부만 다를 뿐입니다.

MAGI는 AGI와 어떻게 다른가요? 아주 약간의 차이입니다. 밖에는 다른 MAGI도 있다는 점을 명심하세요. 여기서는 Roth IRA 기여에 영향을 미치는 것에 대해서만 이야기하고 있습니다. 그러나 MAGI를 얻으려면 AGI에서 수입을 뺀 다음 다른 수입을 다시 추가하면 됩니다. 이를 수행하는 방법을 보여주는 워크시트는 간행물 590의 워크시트 2-1입니다.

기본적으로 Roth 전환에서 소득을 빼고 IRA 공제(이것이 있는지 확실하지 않음), 학자금 대출 이자(이 워크시트를 사용하는 경우 아마도 이 항목이 없을 것임), 수업료 공제(아마도 없을 것임), 해외 소득/공제에 대한 몇 가지 드문 공제(아마도 없을 수도 있음), 저축 채권 이자 및 고용주가 제공하는 입양 혜택을 추가합니다. For most people, your MAGI =your AGI since all of these deductions are pretty rare for the folks worried about this limit for direct Roth IRA contributions. So, focus on your AGI. That means if you contributed directly to a Roth IRA but late in the year realized you probably should not have, one easy fix is to get your AGI below that limit by contributing to an HSA or a self-employed retirement plan like an individual 401(k) or SEP-IRA. Note that giving a bunch of money to charity is NOT a solution to this problem because that is a below-the-line deduction.

If you can't get your MAGI low enough, you will have to do an IRA recharacterization. As far as the IRS is concerned, a recharacterization is as though you never made the Roth IRA contribution at all but made a traditional IRA contribution instead. You don't report a recharacterization separately; you just report a traditional IRA contribution. Keep in mind as you read on the internet about recharacterizations that there used to be two types of them—a recharacterization of a Roth IRA CONTRIBUTION and a recharacterization of a Roth IRA CONVERSION. The second type was outlawed in 2018, but the first one, the one we're talking about today, is still perfectly legal. If you decide you want to undo a Roth conversion these days, you're simply out of luck. Here is how you do a recharacterization of a Roth IRA contribution:

응. 그게 다야. The brokerage takes care of the rest. You can read all about all of the rules in Publication 590 Chapter 1 if you want, but that's basically what they say. 나를 믿지 못합니까? 괜찮은. Here are the IRS instructions:

How Do You Recharacterize a Contribution?

To recharacterize a contribution, you must notify both the trustee of the first IRA (the one to which the contribution was actually made) and the trustee of the second IRA (the one to which the contribution is being moved) that you have elected to treat the contribution as having been made to the second IRA rather than the first. You must make the notifications by the date of the transfer. Only one notification is required if both IRAs are maintained by the same trustee. The notification(s) must include all of the following information:

In most cases, the net income you must transfer is determined by your IRA trustee or custodian.

무슨 말인지 알겠어요? It's just a phone call. Any earnings that the account had in between the contribution and the recharacterization just go over with the contribution. No big deal.

You have until your tax filing date to do this. Most of the time, that's April 15 of the next year. However, the IRS is even more lenient than that. You actually can do this for an extra six months after your tax filing date, but you will have to refile your return.

If you hire somebody else to prepare your taxes, you can skip this section. If you do it yourself, you'll need to make sure you report this correctly. According to Pub 590, you report it on our old friend Form 8606.

Pub 590 says this:

Actually, that's really misleading. If you read Form 8606, you will see that the only time it ever mentions a recharacterization is to tell you NOT to put it on the form.

So, what is Pub 590 talking about? They're talking about this section in the 8606 instructions:

Reporting recharacterizations.

Treat any recharacterized IRA contribution as though the amount of the contribution was originally contributed to the second IRA, not the first IRA. For the recharacterization, you must transfer the amount of the original contribution plus any related earnings or less any related loss. In most cases, your IRA trustee or custodian figures the amount of the related earnings you must transfer. If you need to figure the related earnings, see How Do You Recharacterize a Contribution? in chapter 1 of Pub. 590-A. Treat any earnings or loss that occurred in the first IRA as having occurred in the second IRA. You can’t deduct any loss that occurred while the funds were in the first IRA . . . Report the nondeductible traditional IRA portion of the recharacterized contribution, if any, on Form 8606, Part I. Don’t report the Roth IRA contribution (whether or not you recharacterized all or part of it) on Form 8606. Attach a statement to your return explaining the recharacterization. If the recharacterization occurred in 2023, include the amount transferred from the traditional IRA on 2023 Form 1040, 1040-SR, or 1040-NR, line 4a. If the recharacterization occurred in 2024, report the amount transferred only in the attached statement, and not on your 2023 or 2024 tax return.

The bottom line is that you just report this recharacterized contribution on Form 8606 as if it were the regular old non-deductible traditional IRA contribution that you should have made in the first place. You also need to include a statement. What should your statement look like? I would write something like this:

“To whom it may concern:

I made a 2024 Roth IRA contribution of $7,000 on March 13, 2024, because I didn't know about the whole MAGI limit thing when I made the contribution. After becoming smarter, I recharacterized $7,137.14 (original contribution plus earnings) to a traditional IRA on November 4, 2024. Thank you for helping our country fund its government. You're the best.

Hugs and kisses from your favorite taxpayer,

James Dahle”

Seriously, it doesn't say what has to be on the statement, just that there is one “explaining the recharacterization.” You don't even have to tell them why you did the recharacterization. If you had a loss in the account between contribution and recharacterization, no big deal. It's still as though you made a $7,000 contribution to a traditional IRA and THEN it lost money. If you were able to deduct the contribution (you probably can't) you would get a $7,000 deduction. The IRA provider may also send you a Form 5498 (which has the recharacterized amount on line 4), but you don't actually do anything with it when you file your taxes. It's just an informational return.

Here is where it gets interesting. You've now fixed your mistake in the eyes of the IRS, going from an illegal Roth IRA contribution to a legal traditional IRA contribution (that is probably not deductible for you). But you aren't done with what you meant to do, which is put money into a Roth IRA. You now need to do a Roth conversion. You do it just like you normally would as if you had contributed originally to the Traditional IRA. You can do it the very next day if you like. You can probably even do it the same day; just make sure there is a paper trail showing the money was actually in the traditional IRA at some point. There used to be a waiting period after a recharacterization before you could do a Roth conversion on that money. But that waiting period only ever applied to the recharacterization of a Roth CONVERSION (which was no longer allowed starting in 2018) and NOT the recharacterization of a Roth CONTRIBUTION. So, there is no waiting period. Just reconvert convert it and go on your merry way.

I hope this information helps you fix your mistake. Just do your Roth IRA contributions through the Backdoor going forward, and you won't have this problem again.

What happens if you LOSE money in between the contribution and conversion step? This problem is easily avoided by using an investment like a money market fund that does not go down in value for that time period. But some people fail to do so and end up losing money. When they work their way through their IRS Form 8606, they discover they have basis left over that they can then carry forward indefinitely for years! No big deal; it just makes your paperwork more complicated. Perhaps at some point in the future, you'll do a Roth conversion of tax-deferred money and this carry-forward basis will reduce the tax on that event.

What if you MADE money in the account between contribution and conversion? This actually happens most of the time, so I wrote an entire post on it called Pennies and the Backdoor Roth IRA. Technically, any money earned between the contribution and conversion step is fully taxable at ordinary income tax rates in the year of the conversion. If it is less than 50 cents, you just ignore it. If it's more, you report it on your 8606 and pay taxes on it.

If it is still in the traditional IRA, either do another tiny Roth conversion or leave it there until you do next year's Backdoor Roth IRA process. Either is fine. If you were smart and just used a money market fund and did the conversion as soon as your IRA provider allowed it (usually less than a week and sometimes as early as the next day), this won't be much money and there won't be much tax due.

If you forgot to do the conversion step for eight months afterward, it could be a huge gain on which you're unnecessarily paying taxes. No way to fix this one, just pay your “stupid tax” and move on.

Even worse than paying taxes on a huge gain is not getting the gain in the first place because you left the money sitting in cash for months. No way to fix this one either. Your “stupid tax” this time comes in the form of opportunity cost. Just get the money invested ASAP to stop the cash drag. Maybe you even got lucky and the market went down in between contribution and investment so now you get to buy low.

Some of the most common questions I get are from people who make a late contribution to a Backdoor Roth IRA. What do I mean by late? You are allowed to make an IRA contribution AFTER the calendar year ends. In fact, you have until Tax Day, usually April 15 unless you get an extension of up to six months. While it is to your advantage to contribute to retirement accounts as quickly as possible so that money can start compounding in a tax-protected way, I understand that we all have lots of good things to do with our money and sometimes this gets pushed back into the next calendar year. All it really does is complicate your paperwork a bit.

For example:if you made your 2023 IRA contribution in April 2024, instead of reporting both the contribution and the conversion on your 2023 taxes, you would report only the contribution there. The conversion would be reported on the taxes for the year you did the conversion, i.e., your 2024 tax return due in April 2025. Your 2023 IRS Form 8606 becomes a little simpler and your 2024 IRS Form 8606 becomes a little more complicated. Not a big deal if you can follow the simple instructions.

What confuses people, however, is the pro-rata rule. This is the rule that says you need to empty your traditional IRA by December 31 of the year you do the conversion. Since these folks have never filled out a Form 8606 (or apparently read the instructions), they assume that for a 2023 contribution they need to have a balance of $0 at the end of 2023, even if they didn't do the conversion step until 2024. That's simply not the case. The pro-rata rule isn't applied until the year of the conversion, i.e., December 31, 2024.

How do you empty those IRAs? You usually have two choices.

How large is large and how small is small? It's going to vary by the person and how much disposable cash they have. Most would consider an IRA under $10,000 to be small and an IRA over $100,000 to be large. In between, it's a personal decision as to which would be better for you.

What if you screwed this one up? Your Backdoor Roth IRA conversion step just got pro-rata'd. There is a tax bill associated with that because most of your conversion was of tax-deferred money rather than post-tax money like it was supposed to be.

The fix for this is going to vary by the individual, but the easiest fix is to simply convert the entire IRA to a Roth IRA now, so you end up getting all your post-tax money into that Roth IRA. Another possible fix is to figure out a way to separate your basis in that IRA, roll the tax-deferred money into a 401(k), and then convert the basis left behind in the IRA.

Do yourself a favor and just empty the darn IRA by December 31. Keep in mind that this is usually not an instantaneous process, so don't put it off until you're on holiday break at the end of the year.

Both individual taxpayers and professional tax preparers screw up IRS Form 8606 all the time. In fact, some of them haven't even heard of a Backdoor Roth IRA. (Incidentally, this is one of the best questions to ask while interviewing a potential tax professional—”How many Backdoor Roth IRAs did you help last year?”)

The usual fix to this error is to file a 1040X (Amended Tax Return) and a new Form 8606. You can do this for the last three years if necessary. If you didn't file Form 8606 at all, you'll definitely want to do this. The key is to check lines 15c and 18 on Form 8606. They should both be a number very close to zero if the form is being completed correctly.

The tax preparer should NOT be filing Form 5439. If you did Steps 1-5 right, this form probably doesn't belong in your tax return.

A lot of people wonder about the 1099-R sent to them by their IRA provider and worry that it was done wrong and that it will cause them to pay taxes they shouldn't have to pay. Sometimes the form was filled out wrong, but mostly this is just a lot of anxiety. What gets people anxious is finding something on Line 2a “Taxable amount.” As long as the box on Line 2b is also checked “Taxable amount not determined,” you're golden. 걱정하지 마세요. If it is not, have the IRA provider send you a new, correct form—either with $0 in 2a or the box in 2b checked (usually the latter). Here's what mine from a few years back looked like from Vanguard:

Note that Box 2b is checked, even though a taxable amount of $5,500.07 is being reported to the IRS.

Again, if you're not sure how to enter this into TurboTax, check out my TurboTax tutorial.

Need more help with a Backdoor Roth IRA? I wish Congress would just lift the rule against direct Roth IRA contributions for high earners and save us all this hassle, but who knows if that will ever happen.

While it is “cleaner” to make your contribution and your conversion all in the same calendar tax year, you can make your contribution up until your tax filing date of the next year. The key to filling out the 8606 correctly when you make a contribution after the calendar year is to recognize that the contribution step is reported for the tax year and the conversion step is reported for the calendar year. So imagine you did the following during the calendar year 2023:

Your forms would look like this:

Note that all this serves to do is report basis for the next year. No tax is due. Since no conversion step was done during the calendar year 2022, you only have to fill out lines 1-3 and 14.

Note that you've got to do all of Part I plus Part II for this year because you did the conversion step, unlike last year (2022). Let's go through this line by line.

You have until tax day (generally April 15, but as late as October 15 if you file an extension) of the following year to make your traditional IRA contribution. There is no deadline for the Roth conversion step; it can be done at anytime. Make sure you fill out the paperwork properly according to the section above about late contributions.

그렇습니다. Just remember to report last year's contribution on last year's Form 8606 and this year's contribution and the conversion on this year's Form 8606.

No. Only traditional IRAs, rollover IRAs, SEP-IRAs, and SIMPLE IRAs count. See line 6 of Form 8606 for details.

그렇습니다. All IRAs count toward the pro-rata calculation.

If it is small, convert it to a Roth IRA along with this year's traditional IRA contribution and pay the tax due on it. If large, try to roll it into your employer's 401(k) or if you have self-employment income, into your individual 401(k).

The easiest solution is to convert the entire IRA, SEP-IRA, or SIMPLE IRA that caused the pro-ration and is now composed of both pre-tax and after-tax money. That is also the most expensive solution. A harder solution that may save you some taxes involves isolating the basis in that IRA by rolling the rest of the account into a 401(k) and then convert just the basis to a Roth IRA.

If you put it into a traditional IRA it is going to cause any future Backdoor Roths to be pro-rated. Better options include leaving it where it is; rolling it into your new employer's 401(k) or 403(b); rolling it into your individual 401(k); or, if it is small, just converting the whole thing to a Roth IRA.

In 2024, you are allowed to contribute $7,000 ($8,000 if 50+) per year for you and $7,000 ($8,000 if 50+) for your spouse. This includes all contributions to traditional and Roth IRAs. Rollovers/transfers do not count toward the annual contribution limit. [Visit our annual numbers page to get the most up-to-date figures.]

While in the traditional IRA for a day or two, leave it in cash. Once it is in the Roth IRA, invest it according to your written investing plan. If you don't have one, get one, but in the meantime it would be a good idea to put it into a lifecycle fund such as a Vanguard Target Retirement Fund.

You can use the same ones each year.

The Backdoor Roth IRA process leads to more tax-free retirement account money for doctors and other high-income professionals. If you follow the simple steps outlined above, you will pay less in taxes, boost your returns, facilitate your estate planning, and increase your asset protection. Most members of The White Coat Investor community do these every year, and you should too.

어떻게 생각하시나요? Are you doing Backdoor Roth IRAs? 왜 아니면 안되나요? Any questions about it?

[This updated post was originally published in 2014.]