부채—개인 금융과 이에 대한 끝없는 논쟁에 대해서는 더 이상 할 말이 없을 수도 있습니다. 그것은 때때로 (일반적으로 부적절하게) 노예 제도와 동일시됩니다. 또한 때로는 "재정적 자유" 및 "다른 사람의 돈"과 동일시되기도 합니다(부적절하게). 부채는 우리 금융 시스템의 중요한 부분이자 유용한 도구이지만 재정적 파탄을 가져올 수도 있고 빈곤을 유지할 수도 있습니다. 이번 글에서는 부채에 관한 모든 것을 이야기해보겠습니다. 새롭고 더욱 개방적인 관점, 새로운 전략, 그리고 선과 악에 대한 부채의 힘에 대한 새로운 존중을 갖고 떠나시기를 바랍니다.

부채의 이점

부채의 위험

일반 부채에 관한 지침

좋은 부채와 나쁜 부채

부채의 대체 가능성

학비를 지불하는 대체 방법

마이너스 채권으로서의 부채

마진 투자

부채를 갚거나 투자하세요

부채 없는 삶의 이점

부채의 가치

도구 또는 악마로서의 부채

부채는 세계의 훌륭한 종교 서적은 물론 대부분의 금융 매체와 블로그에서도 나쁜 평가를 받을 수 있습니다. 진실은 부채가 당신 주변 세계의 경이로움에 대한 책임이 크다는 것입니다. 세계 최고의 경제와 생활 방식은 대부분 부채로 인해 발생합니다. '소비자 문화'는 여러 면에서 미국의 강점입니다.

대부분의 경우 돈은 빚입니다. 정부가 화폐를 발행할 때 이는 단순히 정부의 과세 능력을 뒷받침하는 지폐일 뿐입니다. 그러나 대부분의 돈은 정부가 창출하지 않습니다. 은행에 의해 생성됩니다. 우리는 이것을 “부분지급준비은행”이라고 부릅니다. 은행에 돈을 넣으면 그 돈에 대해 0.6%의 이자를 받을 수 있습니다. 그런 다음 6%의 금리로 다른 사람에게 대출합니다. 말이 되네요, 그렇죠? 그 차이는 은행에 수입을 제공하여 모든 비용을 지불하고 이익을 창출할 수 있게 해줍니다. 하지만 당신을 위한 소식이 있어요. 단지 6%의 금리로 돈을 빌려주는 것이 아닙니다. 6%로 돈의 10배를 대출해줍니다. 본질적으로 은행은 돈을 창출했습니다. 그러나 한 사람의 돈은 다른 사람의 빚일 뿐입니다. 그래야 합니다. 어떤 빚이든 마찬가지다. 귀하의 국고채 투자는 정부의 부채입니다. 귀하의 Amazon 채권은 Amazon 주주의 부채입니다. 귀하의 모기지는 다른 사람의 투자입니다. 그것은 그들의 돈이다.

서유럽이라는 역사적 후퇴와 그 후손들이 지난 5세기 이상 동안 세계를 지배해 온 데에는 많은 역사적 이유가 있습니다. Jared Diamond는 주된 이유가 총, 세균, 강철이라고 주장합니다. 윌리엄 번스타인(William Bernstein)은 <풍요의 탄생>이 재산권, 과학적 합리주의, 자본 시장, 효과적인 교통 및 통신 수단에 기인한다고 주장합니다. 어떤 요소가 가장 중요한지는 누가 알지만, 이탈리아 북부에서 발전한 은행(부채) 시스템이 이후 네덜란드에서 개선되었고 결국 런던과 뉴욕이 이에 큰 역할을 했다는 것은 의심의 여지가 없습니다.

부채 및 파산 보호 덕분에 세계에서 가장 크고 가장 수익성이 높은 기업이 발전할 수 있었습니다. 그들은 종종 “작은 사람”을 박해한다고 조롱당하지만, 사실 기업은 우리 모두를 극적으로 부유하게 만들고 우리의 생활 방식을 극적으로 더 좋게 만들었습니다. 추측해 보세요. 대부분의 기업은 부채를 사용하여 현재 규모로 성장하고 현재 사업 운영을 유지했습니다. 시간에 따라 다르지만 S&P 500 기업 중 부채가 없는 기업은 5% 미만입니다.

좀 더 개인적인 차원에서(지구상의 수십억 명의 사람들을 곱하면 상당히 큰 금액입니다) 부채로 인해 우리 중 많은 사람들이 중요한 방식으로 삶을 더 나은 삶을 살 수 있게 되었습니다. 아마도 그것은 우리의 수입을 극적으로 증가시킬 수 있는 교육 비용을 지불했을 것입니다. 아마도 그것은 우리가 삶을 살아갈 수 있는 환상적인 장소를 살 수 있게 해 주었을 것입니다. 아니면 소규모 사업을 시작하거나 사업을 시작하게 되었을 수도 있습니다.

집을 구입하기 전에 집의 전체 비용을 저축해야 한다고 상상해 보십시오. 부유한 집안 출신이 아니면 학교에 가지 않는다고 상상해 보세요. 자신의 간판을 장식하는 데 필요한 자본에 접근할 수 없기 때문에 급여가 낮은 직원으로 갇혀 있다고 상상해 보십시오. 믿을 만한 중고차를 구입하기 위해 수천 달러를 빌릴 수 없어서 훌륭한 직장을 거절해야 한다고 상상해 보십시오. 부채는 우리가 사회로서 그리고 개인으로서 누리는 경제적 성공의 한 가지 이유입니다.

몇 세기 전에는(놀랍게도 소수) 부채 불이행의 결과가 훨씬 더 심각했습니다. 채무자의 감옥은 1840년대 미국에서도 실제로 존재했습니다. 빚을 갚지 않으면 당신이나 당신을 대신해 누군가가 빚을 갚을 때까지 말 그대로 감옥에 갇히게 됩니다. 기업과 개인 파산 보호는 세계 역사상 비교적 새로운 것입니다. 그러므로 세계의 위대한 종교 서적들이 부채에 대해 심오하게 경고하는 것은 놀라운 일이 아닙니다.

유대인과 기독교인 모두 이 책에서 지혜를 얻습니다. 대출과 대출에 대해 무엇을 말하는가? 꽤 많습니다.

부자는 가난한 사람을 주관하고, 빚진 사람은 채주의 종이 된다. (잠언 22:7)

보증을 서거나 빚을 담보로 삼는 사람이 되지 마십시오. 갚을 것이 없는데 어찌하여 네 침상을 네 밑에서 치워야 하겠느냐? (잠언 22:26-27)

악인은 꾸어도 갚지 아니하나 의인은 은혜를 베풀고 주는도다. (시편 37:21)

매 7년 끝에는 면제해 주십시오. 탕감의 방법은 이러하니라 모든 채권자는 자기 이웃에게 빌려준 것을 탕감할지니라 그는 그의 이웃과 형제에게 그것을 강요하지 말지니 이는 여호와의 해방이 선포되었음이니라 (신명기 15:1-2)

네가 많은 민족에게 꾸어줄지라도 꾸지 않을 것이니라. (신명기 15:6, 28:12)

너희와 함께한 내 백성 중 가난한 자에게 돈을 꾸어주면 너는 그에게 고리대금 같이 하지 말며 그에게 이자를 받지도 말지니라 네가 이웃의 옷을 전당 잡거든 해가 지기 전에 그에게 돌려보내라. (출애굽기 22:25-27)

낯선 사람을 위하여 보증을 서는 사람은 반드시 해를 입게 되지만, 손을 잡기를 싫어하는 사람은 안전합니다. (잠언 11:15)

지각 없는 사람은 이웃 앞에서 보증을 서며 보증을 서게 됩니다. (잠언 17;18)

외국인에게 이자를 받을 수는 있어도 형제에게 이자를 받을 수는 없습니다. (신명기 23:20)

기독교인들은 신약성경도 부채 방지 책임을 발견합니다. 대출보다는 차용에 더 중점을 두지만 대출을 통해 이익을 얻는 것도 반대합니다.

서로 사랑하는 것 외에는 아무에게든지 아무 빚도 지지 말라 남을 사랑하는 자는 율법을 다 이루었느니라 (로마서 13:8)

너희 중에 누가 망대를 쌓고자 할 때 자기의 가진 것이 그것을 완성하기에 충분한지 먼저 앉아서 그 비용을 계산하지 아니하겠느냐? (누가복음 14:28)

네게 구하는 자에게 주고 네게 꾸고자 하는 자에게 거절하지 말라. (마태복음 5:42)

그리고 네가 받기를 기대하는 사람들에게 꾸어 준다면, 네게 무슨 영예가 있겠느냐? 죄인이라도 같은 액수를 받으려고 죄인에게 빌려줍니다. 오직 너희는 원수를 사랑하고 선대하며 아무 것도 바라지 말고 꾸어 주라 그리하면 너희 상이 클 것이니라 (누가복음 6:34)

오늘 우리에게 일용할 양식을 주시고, 우리가 우리에게 빚진 자를 용서한 것 같이 우리 빚을 용서해 주십시오. (마태복음 6:12)

경전과 예수 그리스도 후기 성도 교회의 지도자들은 대출에 대해 강력하게 경고합니다.

누구든지 이웃에게 꾸는 사람은 빌린 것을 돌려주어야 합니다. (모사이야서 4:28)

빚을 갚고 속박에서 벗어나십시오. (교리와 성약 19:35)

적에게 빚을 지는 것은 금지되어 있습니다. (교리와 성약 64:27)

빚을 모두 갚으세요. (교리와 성약 104:78)

주님의 집을 건축하기 위해 빚을 지지 마십시오. (교리와 성약 115:13)

현대 교회 지도자들은 그다지 극단적이지는 않지만 여전히 확실히 부채 반대 입장을 취하고 있습니다. J. Reuben Clark은 대공황 시절에 다음과 같이 말했습니다(조금 바꿔서 설명합니다):

J. Reuben Clark Jr. 회장은 1938년에 "할부로 구입한다는 것은 미래의 수입을 담보로 잡는 것을 의미합니다. 질병이나 사망 또는 실직으로 인해 수입이 중단되면 구입한 재산과 투입한 자산을 모두 잃게 됩니다. 한 가지 제안을 드리고 싶습니다. 일반 가족은 실제 생활 필수품만 분할 구입하고 사치품은 구입할 때 지불할 수 있는 대로 구입하는 것이 좋을 것입니다. 나는 선을 긋지 않겠습니다. 필수품과 사치품 사이에서, [혼다 시빅을 타고] 출근할 수 있는 [의사]가 그런 목적으로 할부 계획에서 [터무니없는 속도의 테슬라 모델 S]를 구입하는 것은 거의 정당화되지 않을 것이라고 말할 수 있습니다.”

그리고 제가 이전에 사용한 더 유명한 인용문은 다음과 같습니다:

"이자는 잠들지도 아프지도 죽지도 않고 병원에 가지도 않고 일요일과 공휴일에도 일하지 않고 휴가도 가지 않고 방문하거나 여행도 가지 않고... 사랑도 없고 동정심도 없고 화강암 벼랑처럼 단단하고 영혼이 없다. 일단 빚을 지면 이자는 밤낮으로 매 순간 당신의 동반자가 되고, 피하거나 빠져나갈 수도 없고, 해산할 수도 없고, 간청이나 요구나 명령에 굴복하지 않고, 그 일을 할 때마다 방향을 바꾸거나 방향을 벗어나거나 요구 사항을 충족하지 못하면 당신은 무너질 것입니다.”

최근에는 고든 B. 힝클리(Gordon B. Hinckley)가 다음과 같이 말했습니다:

"나는 우리 국민을 포함해 전국민에게 걸려 있는 막대한 소비자 할부 부채로 인해 고민하고 있습니다...물론 집을 구입하기 위해 돈을 빌려야 할 수도 있다는 것을 알고 있습니다. 그러나 우리가 감당할 수 있는 집을 구입하여 30년 동안 무자비하거나 쉬지 않고 끊임없이 우리 머리에 맴돌게 될 지불금을 완화합시다. ... 재정 상태를 살펴보십시오. 지출을 절제하고, 부채를 피하기 위해 구매에 자제할 것을 촉구합니다. 가능한 한 빨리 빚을 갚고 속박에서 벗어나십시오.

가계에 심각한 빚이 있으면 자립을 이룰 수 없습니다. 다른 사람에게 의무를 지고 있는 사람은 속박으로부터의 독립도 자유도 없습니다.

어떤 상황에서는 대출이 필요합니다. 아마도 일부 대학생들은 교육을 마치기 위해 돈을 빌려야 할 수도 있습니다. 그렇다면 갚으십시오. 그리고 다른 방법으로 누릴 수 있는 안락함을 희생하더라도 즉시 그렇게 하십시오. 대부분의 사람들은 집을 확보하기 위해 대출을 받아야 합니다. 물론 신중한 차입은 사업 관리에 필요하고 적절할 수 있습니다. 하지만 현명하게 생각하시고 지불 능력 이상으로 돈을 지불하지 마십시오.

적당한 가격의 주택 구입과 기타 몇 가지 필수품 구입을 위한 합리적인 부채는 허용됩니다. 그러나 내가 앉아 있는 자리에서 나는 정말로 필요하지 않은 것을 현명하지 않게 빌린 많은 사람들의 끔찍한 비극을 매우 생생하게 봅니다.”

토마스 S. 몬슨은 다음과 같이 말했습니다:

“우리는 모든 후기 성도들이 계획을 세울 때 신중하고, 생활을 보수적으로 하며, 과도하거나 불필요한 빚을 피하도록 촉구합니다.”

제임스 E. 파우스트:

"부채 없는 주택을 소유하는 것은 검소한 생활의 중요한 목표입니다. 모기지와 유치권이 없는 주택은 압류될 수 없습니다. 독립이란... 개인 부채와 이자가 없고 전 세계의 부채로 인해 부과되는 비용을 부담하지 않는 것을 의미합니다."

무뚝뚝한 것으로 유명한 스펜서 W. 킴볼(Spencer W. Kimball)은 다음과 같이 말했습니다:

“빚에서 벗어나 빚에서 벗어나세요.”

히버 J. 그랜트(Heber J. Grant)는 다음과 같이 설명했습니다:

"인간의 마음과 가족에게 평화와 만족을 가져다 줄 수 있는 것이 있다면 그것은 우리의 수입 범위 내에서 생활하는 것입니다. 그리고 괴롭게 하고 낙담하게 하고 낙담하게 하는 것이 있다면 그것은 감당할 수 없는 빚과 의무를 갖는 것입니다."

꾸란에서 가장 긴 구절은 빚에 관한 것이며 그 중 일부는 다음과 같습니다:

일정 기간 동안 빚을 갚으려면 문서로 기록하십시오… 빚진 사람이 지시하게 하고, 자기 주님이신 하나님을 경외하고 조금도 감하지 마십시오. 두 사람을 증인으로 불러... 빚을 갚을 때까지 기한과 함께 적거나 적거나 적는 것을 멸시하지 마십시오. 이 방법은 하나님 보시기에 더 공평하고 증언하기에 더 확실하며, 여러분 사이에 일어나는 의심을 더 많이 막아 줄 것입니다. (2:282)

또 다른 사람은 이렇게 말합니다:

알라께서는 고리대금에서 모든 축복을 빼앗으시겠지만 자선 행위에 대해서는 늘려주실 것입니다. (2:276)

더욱 중요한 것은 선지자 무함마드가 다음과 같이 말했습니다:

“알라를 위해 전투에서 죽은 사람이 다시 살아나 빚을 졌다면, 그는 빚을 갚을 때까지 천국에 들어가지 못할 것입니다.”

“남자가 고의로 빼앗은 리바 디르함(이자)은 지나(음행)를 36번 저지르는 것보다 더 나쁜 죄입니다.”

독실한 무슬림들은 대출과 차입 측면 모두에서 이 문제를 매우 심각하게 받아들입니다. 매달 나는 무슬림으로부터 차입금이 없는 부동산 투자나 이자를 받지 않는 뮤추얼 펀드에 대해 문의하는 이메일을 받습니다. 그들은 확실히 채권이나 CD에는 관심이 없습니다. "샤리아를 준수"하는 것으로 간주되는 뮤추얼 펀드가 몇 개 있는데, 저는 보통 그 펀드를 그 펀드로 유도합니다.

아마도 비종교인이 이해하기 더 쉬운 것은 부채가 우리 사회에 미치는 영향일 것입니다. 다음 2021년 통계를 고려해 보세요:

우리 대부분은 재정적 부채로 인해 인생이 망가진 사람을 알고 있습니다. 부채가 이룩한 모든 좋은 점에도 불구하고, 그 여파로 많은 사람들의 삶이 파괴되었습니다. 이는 현재 우리 사회에서 제공되는 모든 소비자 보호 및 파산 보호에 적용됩니다.

업계 관계자와 이야기를 나누다 보면 놀라운 그림이 나타납니다. 은행은 고객이 빚을 갚지 않고 더 많은 돈을 빌릴 수 있는 방법을 알아내기 위해 말 그대로 지속적으로 고객을 대상으로 실험을 진행하고 있습니다. 금융 업계에는 빚을 지고 부를 축적하는 것을 막는 일을 하는 사람들이 있다는 것을 인식해야 합니다.

벤저민 프랭클린은 다음과 같은 유명한 말을 했습니다:

“빚이 늘어나느니 저녁도 안 먹고 잠자리에 드는 편이 낫다.”

따라서 부채를 방지하기 위해 지나치게 종교적일 필요는 없습니다.

분명히, 당신이 재정적인 삶 전체에 걸쳐 부채에 대해 어떤 종류의 온건한 방향을 계획할 것으로 예상한다면, 위의 현명한 사람들이 수천 년 동안 우리에게 경고해 온 문제를 피하기 위해 엄청난 주의를 기울여야 합니다. 수학적 가능성이 무엇이든 관계없이 어떤 목적으로든 돈을 빌리지 않으면 사회의 대다수가 더 나아질 것입니다.

어떤 사람들은 다양한 목적으로 얼마를 빌릴 수 있는지에 대한 실용적인 지침을 갖는 것이 도움이 될 수 있습니다. 제 생각은 이렇습니다. 하지만 일부 사람들은 제 생각에 동의하지 않을 수도 있습니다.

신용카드는 이름에도 불구하고 신용카드가 아닙니다. 그들은 끔찍한 신용원입니다. 이자율은 높으며(때로는 가변적), 지불 누락으로 인한 결과는 심각할 수 있으며, 지불 계획은 실제로 부채를 갚도록 설계되지 않았습니다. "편의카드"라고 불러야 합니다. 그게 훨씬 더 정확한 이름이에요. 현금을 인출하고 매장으로 돌아가기 위해 은행이나 ATM에 가는 것은 편리하지 않습니다. 녹색 지폐 뭉치를 들고 돌아다니는 것은 불편합니다. 카운터에서 항공권을 구매하는 것은 편리하지 않습니다.

신용카드를 입력하세요. 사용하기가 더 쉽고, 여러 가지 방법으로 사용하기에 더 안전하며, 월말에 지불하기만 하면 이 모든 편리함을 누리는데도 비용이 전혀 들지 않습니다. 실제로 일부 신용카드 보상 프로그램으로 인해 현금 대신 카드 사용 대가를 받을 수도 있습니다.

하지만 농담하지 말자. 은행은 바보가 아니다. 그들은 잘 지내고 있어요. 미국인의 45%는 실제로 카드에 잔액을 가지고 있습니다. 게다가 신용카드를 사용하는 회사에서는 수수료를 지불하고 있습니다. 이러한 수수료는 일반적으로 은행이 지급하는 보상보다 높습니다. 기업(The White Coat Investor 포함)이 신용카드를 허용하는 이유는 무엇입니까? 우리는 소비자인 당신이 카드를 사용하도록 허용하면 더 많이 사고 더 많이 구매할 가능성이 훨씬 더 높다는 것을 알고 있기 때문입니다. 그런데 신용카드 발급 비용은 누가 지불하는지 아시나요? 맞습니다, 당신, 소비자. 일반적으로 신용카드로 구매하기 때문에 구입하는 모든 제품의 가격은 2~3%가 너무 높습니다.

그것은 행동 금융 측면을 고려하지도 않습니다. 여러 연구에 따르면 우리가 카드를 사용할 때 더 많은 돈을 지출한다는 사실이 밝혀졌습니다. 편리함과 실질적인 신용 외에도, 녹색 물건의 큰 더미와 이별하는 것보다 심리적으로 덜 고통스럽습니다. 저축률을 20%까지 높이는 데 어려움이 있는 경우 문제를 해결하는 가장 좋은 방법 중 하나는 신용 카드를 줄이는 것입니다.

어쨌든, 구매 시 카드를 사용하기로 결정하더라도 신용 카드가 아닌 단지 편의를 위한 카드라는 점은 의심할 여지가 없습니다. 따라서 신용카드 회전부채의 허용 비율은 0.0입니다. 제로. 나다. 신용 카드 잔고가 남아 있다면 이 금융 게임에 실패한 것이므로 신용 카드를 전혀 사용해서는 안 됩니다. 적.

나는 자동차에 대한 나의 태도와 생각에 대해 많은 반발을 받습니다. 사람들은 내가 지난 6개월 동안 팔리지 않은 자동차 근처에 접근한 것에 대해 미친 사람이라고 생각합니다. 나는 가족이나 지구에 관심이 없다는 말을 들었습니다. 하지만 자동차를 빌릴 수 있는 최대 금액에 대한 조언을 원한다면 내 대답은 $10,000 미만이며 차라리 $5,000에 가깝다고 보고 싶습니다. 네, 2% 대출이라 해도 그렇습니다. 네, 0% 대출이더라도 그렇습니다. 부채 애호가들은 자동차를 빌리는 것이 재정적 성공의 비결이라는 것을 나에게 설득하려 했으나 실패했습니다. 제가 가장 좋아하는 것 중 하나는 다음과 같습니다. 한 의사가 신용으로 자동차를 구입한 다음 이를 담보로 여러 번 빌리는 것이 현명하다고 나에게 설득하려고 했습니다. 그 의사는 나에게 "이국적인" 자동차를 사도록 설득하기까지 했습니다.

부를 쌓고 자선 단체를 지원하려는 계획이 이국적인 자동차를 구입하는 것이라면 우선 순위가 약간 헷갈릴 수 있습니다. 부동산에 투자하기 위해 250,000달러를 원했다면 먼저 자동차를 구입한 다음 차를 빌리지 마십시오. 그냥 부동산에 투자하세요. 부동산에 투자하고 자선단체에 기부할 수 있는 금액이 더 많을 것이라고 장담하지만, 트랙 외에 인맥을 쌓을 수 있는 다른 곳을 찾아야 합니다.

$10,000 이상의 현금이 있고 자동차가 필요한 경우 자동차 구입을 현금으로 지불하고 보유하고 있는 현금 한도 내에서 구매하십시오. $10,000가 없고 안정적인 교통수단이 필요하다면, 그럴 때까지 $10,000 미만의 자동차를 운전하세요.

많은 사람들이 내 자동차 조언을 싫어하고 그것을 따르지 않았음에도 불구하고 성공했다고 지적합니다. 글쎄요. 당신은 일년에 30만 달러를 벌어요. 그런 종류의 소득은 많은 재정적 실수를 덮을 수 있습니다. 그렇다고 해서 실수가 줄어들지는 않습니다. 그러나 의사의 수입이 감당할 수 없는 실수 중 하나는 미래 수입에 비해 엄청난 양의 학자금 대출을 받는 것입니다. 너무 많은 사람들이 학비가 매우 비싼 학교에서 교육비를 전액 빌릴 수 있고, 급여가 낮은 전문 분야를 선택하고, 해당 전문 분야 내에서 형편없는 급여를 받는 개인 직업을 가질 수 있다고 믿으면서도 여전히 모든 것이 잘 될 것이라고 생각합니다. 추측해 보세요. 당신은 수학에 합격할 수 없습니다.

당신의 마음이 얼마나 멋진지는 중요하지 않습니다. 재정적/직업적 결정을 잘못하면 재정적으로 안전하지 못할 뿐더러 성공도 훨씬 더 어려워질 것입니다. 가족이 학비를 지불할 돈이 없으면 가정의나 소아 내분비학자가 될 수 없다는 말은 아닙니다. 그것이 당신의 직업 목표라면, 그 직업 목표에 맞는 학자금 대출 계획이 필요하다는 뜻입니다. 그 계획은 매우 검소하게 생활한 다음, 교육을 받은 후 5년 동안 거주지처럼 생활하는 것과 낮은 생활비 지역에서 특히 고임금 직업을 결합하여 대출금을 갚는 것일 수 있습니다. 그 계획은 훈련 후 학업에 시간을 투자하여 PSLF 자격을 얻을 수 있습니다. 그 계획은 20년 동안 PAYE 지불을 하는 동시에 세금 폭탄 자금을 절약하는 것일 수도 있습니다. 하지만 모래 속에 머리를 박고 최선을 다할 수는 없습니다.

다음은 교육에 대해 제가 일반적으로 제시하는 몇 가지 비율입니다. 비율의 첫 번째 부분은 훈련을 마친 시점의 학자금 대출 규모입니다. 비율의 두 번째 부분은 훈련을 마친 후 2년 이내의 총 수입입니다.

1:1 이하라면 좋은 투자를 하신 겁니다. 우리는 학자금 대출이 $250,000이고 연봉이 $250,000인 직업에 대해 이야기하고 있습니다. 주민처럼 생활하면 단 2~3년 안에 이 빚을 갚고 평생 동안 그 큰 수입을 누릴 수 있습니다.

2:1의 거래는 여전히 수용 가능하지만 실제로는 좋은 거래가 아니라고 주장합니다. 이것이 제가 추천하는 최대 부채 수준입니다. 수의사가 되고 싶고 회사를 나와 $75,000를 벌 것으로 예상한다면 학교에 가기 위해 $300,000를 빌리지 않는 것이 좋습니다. 비율을 2로 제한하더라도 거주자처럼 생활하면 빚을 갚을 수 있습니다. 좀 더 오래 해야만 합니다. 연간 $300,000를 벌고 $600,000를 빚지고 있는 의사를 생각해 보십시오. 세금($75,000)을 제하고 거주자($75,000)보다 조금 더 나은 삶을 살고 있다면 연간 $150,000의 빚을 갚을 수 있습니다. 5년 안에 없애야 합니다.

3-4+:1에서는 더 이상 좋은 투자를 하지 않았습니다. 501(c)(3)에 대해 10년 동안 풀타임으로 일함으로써 PSLF를 통해 면세를 받거나 20년 동안 PAYE 지불(또는 25년 동안 REPAYE)을 함으로써 IDR 용서를 통해 과세(세금 폭탄에 대비해 절약)함으로써 부채를 탕감함으로써 구원을 받을 수 있습니다. 하지만 입법적 위험이 너무 큰 진로를 추천하는 것은 매우 어렵습니다. 비율을 맞춰야 합니다. 많이 빌리지 않거나 (아마도 더 가능성이 높지만) 더 나은 직업을 얻으십시오. 이러한 종류의 비율을 가진 대부분의 의사는 전문 분야에서 가장 낮은 사분위수 소득을 가지고 있습니다. 소득이 높을수록 비율은 2:1 또는 그보다 더 좋을 수 있습니다. 이들은 대개 부채 문제보다 소득 문제가 더 큰 경우가 많습니다.

몇 가지 지침이 필요한 분들을 위해 모기지에 관한 두 가지 일반 규칙을 제시합니다.

아주 간단하죠? 그리고 그것은 목표가 아니라 최대치라는 것을 기억하세요. 따라서 $800,000 집을 갖고 싶지만 $300,000만 벌면 $200,000를 저축해야 합니다. 의사 대출을 이용하고 $10,000만 저축한다면 더 저렴한 집을 찾으세요.

생활비가 매우 높은 지역에 살고 있다면 아마도 그러한 조언이 우울할 것입니다. 당신이 베이 지역에서 $180,000를 버는 의사라면 기본적으로 직장에서 차로 3시간 이내에는 집을 사지 못할 것이라고 말했습니다. 이러한 종류의 영역에서는 해당 비율을 2X에서 3X-4X로 늘리는 것이 허용되지만 10X로는 확장할 수 없다고 생각합니다. 비록 그 도박이 때때로 누군가에게 성공하더라도 당신은 집에서 가난한 사람이 되고 싶지 않습니다. 그렇게까지 한다면 부를 쌓는 능력에 재정적으로 심각한 영향을 미치며, 사립 학교를 다니지 않고, 휴가를 덜 자주 보내고, 자동차를 덜 타며, 더 늦거나 덜 사치스러운 은퇴 등 재정적 생활의 다른 부분을 보충해야 한다는 점을 깨달으십시오.

레이크 홈이나 스키 콘도 등 세컨드 홈의 경우 현금으로 지불해 주셨으면 좋겠지만 비용의 일부를 빌리는 것도 괜찮다고 생각합니다. 중요한 것은 이 집을 본채처럼 투자가 아닌 소비재로 보는 것입니다. 두 번째 주택에 드는 비용을 모두 감당할 수 있고 여전히 목표 달성에 필요한 만큼 저축을 할 수 있다면 구입해도 괜찮습니다. 하지만 원래 집에 입주했을 때보다 더 큰 계약금을 내는 것이 적절해 보입니다. 시장이 변하면(그리고 휴가용 부동산이 어려워질 수 있음) 물속에 빠지고 싶지 않을 것입니다. 당신은 그것을 팔고, 대출금을 갚고, 떠날 수 있기를 원합니다.

개조 비용도 매우 비쌀 수 있으며 일반적으로 부채로 부분적으로 비용을 지불합니다. 여기서 나의 지침은 개조로 인해 집의 가치가 상승한 금액 이상을 빌리지 않는 것입니다. 이는 지출 금액의 50% 이하일 가능성이 높습니다. 주방과 욕실이 조금 더 좋아졌습니다. 조경, 차고 및 "독특한" 개조 공사의 수익은 훨씬 적습니다. 일부 개조 공사(수영장 등)는 향후 구매자의 관점에서 부담이 될 수도 있습니다.

주택은 인생에서 가장 비싼 구매일 가능성이 높습니다. 특히 빌린 돈을 사용하는 경우에는 너무 많은 비용을 지출하지 마십시오.

나는 보트, 스노모빌, 사륜차, 가구, 양탄자, 그림 등 다른 물건을 사기 위해 전혀 빌려서는 안 된다고 생각합니다. 나는 그 품목을 단 한 번만 지불하고 그 대가가 지불되었음을 알 수 있을 때 그 품목을 구매하는 것이 훨씬 더 즐겁다고 생각합니다. 그 물건들은 아마도 가치가 떨어지겠지만, 문제가 생기면 이제 저주(내 현금 흐름에서 지속적인 지불이 필요하기 때문에)가 아니라 실제로 내 인생에서 축복(무언가로 팔 수 있기 때문에)이 됩니다.

개인 금융에는 좋은 부채와 나쁜 부채가 있다는 생각이 널리 퍼져 있습니다. 기본 개념은 소득을 늘리거나(학자금 대출, 사업 부채, 실무 대출) 가치가 높은 자산(집, 연습실, 이국적인 자동차(?))을 구입할 수 있게 해주는 부채는 어쨌든 좋은 부채이고 서비스나 소모품 또는 감가상각 자산(신용 카드, 자동차 대출, 가구 대출)을 구매하는 데 사용되는 모든 것은 악성 부채라는 것입니다. 이것은 부채에 대한 매우 피상적인 이해입니다. 예를 들어, 어느 것이 부실채권인지:

내가 어느 것을 더 갖고 싶은지 말씀드릴 수 있지만, 학자금 대출은 어쩐지 항상 "좋은 부채" 범주에 속합니다. 일부 부채가 다른 부채보다 품질이 더 높다는 의미는 아니지만 이에 대해서는 잠시 후에 살펴보겠습니다.

진실은 돈과 마찬가지로 부채도 대체 가능하다는 것입니다. 원래 부채가 자동차, 학교, 집 또는 아이스크림 콘 비용을 지불하기 위해 인출되었는지 여부는 실제로 중요하지 않습니다. 일단 가지면 빚입니다. 그리고 빚이 있는 경우, 빚을 갚는 대신 무엇이든 구입하는 것은 이미 가지고 있는 최고 이자 부채와 동일한 조건으로 해당 서비스나 제품을 구입하는 것과 똑같습니다.

와! 정말 놀랍습니다!

맞습니다. 빚을 지고 있다면 구입하는 모든 것이 신용으로 되어 있습니다. 식료품, 휴대폰 요금, 휴가, 자동차… 모든 것. 그러한 사고방식은 귀하가 좀 더 빨리 빚에서 벗어나는 데 도움이 될 수 있습니다.

"이것을 위해 3.5%로 빌릴 수 있을까요? 아마도 아닐 것이므로 구매하지 않겠습니다."

우리 사회의 대부분의 사람들은 빚을 갖고 있기 때문에 우리 사회의 대부분은 모든 것을 빌리고 있습니다. 꼭 나쁜 것은 아니지만 세상을 보는 흥미로운 방법이라고 생각합니다.

위에서 언급했듯이, 기본적으로 어떤 빚도 있어서는 안 된다고 생각할 정도로 빚을 반대하는 사람들이 있습니다. 하지만 실제로 눌러보면 그것이 그렇다는 것을 알게 됩니다. 빚을지고. 그들은 단지 그것을 다른 것으로 부르고 있을 뿐입니다. 제가 가장 좋아하는 해결 방법 중 하나는 이슬람 모기지 개념입니다. 독실한 무슬림들은 빌릴 수 없는데 어떻게 집을 사나요? 그들은 "이슬람 모기지"를 받습니다. 세 가지 유형이 있습니다:

이자라: 은행은 부동산을 구입하여 고정된 월별 가격으로 고정된 기간 동안 임대합니다. 그런 다음 은행은 귀하에게 부동산을 제공하고 귀하가 대출 기관에 상환한 후 귀하의 이름으로 집을 배정합니다.

무샤라카: 귀하와 은행은 각각 재산의 별도 부분을 소유합니다. 대금을 지불할 때 일부는 자본금이고 일부는 임대료이며, 은행은 귀하에게 부동산 지분 중 조금 더 많은 금액을 지급합니다. 임대료는 지불금의 이자 부분과 마찬가지로 기간이 지나면서 점차적으로 낮아집니다.

무라바하: 은행이 부동산을 구입합니다. 그런 다음 고정된 기간 동안 할부로 지불하게 될 더 높은 가격으로 귀하에게 판매합니다. 기본적으로 이자/이익이 구매 가격에 반영됩니다.

독실한 무슬림만큼 빚에 반대하는 사람이 있다면 라디오 토크쇼 진행자 데이브 램지(Dave Ramsey)일 것입니다. 그가 괜찮다고 생각하는 유일한 부채(권장하지는 않지만)는 월 지불금이 집으로 가져가는 급여의 25% 미만인 20% 계약금이 있는 15년 고정 모기지입니다. 데이브는 교육을 위해 돈을 빌려서는 안 된다고 생각합니다. 사실 저는 돈을 빌리지 않고 학부 교육을 받는 것이 꽤 합리적이라고 생각합니다. 신중한 학교 선택, 장학금 신청, 여름방학 동안 열심히 공부하고 아르바이트를 하고, 부모님의 약간의 도움만 있다면 학자금 대출 없이도 학부 교육을 받을 수 있다고 생각합니다.

그러나 일반적으로 출석 비용이 연간 $50,000-$100,000에 이르는 의학 및 치과와 같은 값비싼 전문 학교의 경우 모든 것이 달라집니다. 학생이 아르바이트로 그런 일을 하리라 기대할 수는 없습니다. 게다가 여름방학도 (거의) 없고 장학금도 훨씬 적습니다.

의과대학에 가기 위해 돈을 저축하는 것은 별로 현명하지 않습니다. 쓸 돈을 모으기 위해 15년 동안 일하다가 하고 싶은 일을 하지 못하는 인생의 큰 부분은 말할 것도 없고, 15년 동안 의사의 수입을 놓칠 수도 있습니다. 그것을 빌리는 것이 훨씬 더 현명합니다. 합리적인 금액만 빌리고 있는지 확인하고 나중에 합리적인 기간 내에 이를 처리할 계획을 세우면 됩니다. Yes, there will still be a few students who are really hosed when they do not match repeatedly, but for the most part, it's a pretty smart investment, even with borrowed dollars.

Dave's proposed solution for paying for medical school is to do what I did—sign a contract instead of borrowing money. However, like an Islamic Mortgage, this is just debt by another name. The three main contracts that people sign are:

With each of these programs, your tuition, books, and fees are covered, and you are provided a living stipend. 엄청난! A “scholarship” right? 설마. All you have done is signed an indentured servitude agreement. Centuries ago, people came to America as indentured servants. Their employer paid the costs for them to emigrate, and then they were obligated to work for that employer—usually very hard and for not much money—for seven years. That sounds an awful lot like these programs.

With the HPSP program—in exchange for paying for you to get an MD, DO, DDS, or DMD—you have to go through the military match, live where they tell you to live, and be deployed wherever they tell you to go for four years. The pay is significantly less than the average for most specialties. In essence, they just gave you part of your salary upfront. Now the deal is better for some people than others (more expensive school, lower-paying specialty) but it's rare for someone to come out dramatically ahead financially for taking this deal. You certainly do not finish school “debt-free”, except by the narrowest definition of debt. Most doctors, if they live and work similarly to how they must live and work in the military, could retire substantial medical school loans in less time than it took to pay off their military commitment.

The deal with NHSC is similar. While there is no NHSC match or deployments, they certainly limit the specialties you can practice and the physical location and type of practice for four years afterward. The pay is also relatively poor (about $160,000 these days).

With an MD/Ph.D, you take the first two years of medical school, and then you hit pause to earn a Ph.D. That Ph.D may take anywhere from 3-7 years before you start your third year of medical school. Yes, school is paid for and you earn a stipend, but your opportunity cost is a half-decade of attending physician income. In essence, you're getting part of your pay upfront in the form of waived tuition.

The bottom line with each of these programs is that if you're going to do any of these things (military service, work in a rural or underserved community, or get a PhD) anyway, you should enroll in these contract programs. But you should not do any of them just to avoid medical school loans.

When building a portfolio, debt functions as a negative bond. Just like a bond provides a low-risk fixed return, so does paying off debt. While bonds do lower overall portfolio volatility and perhaps assist investors in staying the course in a market downturn, there is no mathematical reason to hold a bond paying 2% while you have a 4% mortgage or a 7% student loan you could pay off instead.

On a similar note, many people advocate for a 100% stock portfolio—no bonds. They argue that it provides the highest return. My question for them is, “Why stop at 100%? If 100% is good, why isn't 120% or even 150% better?” How do you get to stock percentages greater than 100%? Well, since debt is a negative bond, you get there by borrowing money and investing it. Many brokerages will let you borrow against your portfolio, sometimes at surprisingly low but typically variable rates. You can borrow up to 50% of the value of your portfolio. Most would recommend against a ratio that high, since when you are that highly leveraged, any drop in the value of the stocks will trigger a margin call. But if you borrowed 20% of the value of your portfolio, you could get to 120% stock portfolio pretty easily.

Frankly, since money is fungible, if you have any debt at all, it's like you're investing on margin already. While investing in stocks on a 2% margin might seem somewhat wise, investing at an 8% margin using some crummy student loan or a 15% margin using a credit card does not.

It's pretty easy to understand how borrowing at 2% and investing at 10% works out well in your favor. Imagine you borrow $10,000 at 2%. Each year you owe $200 (2%) in interest. But you may earn $1,000 in interest (10%). Before taxes, you've made $800. After taxes (let's assume a 35% marginal tax rate), you've made $520. It seems pretty good to get a “free” $520. However, remember that you don't get 10% from a risk-free investment. If that investment had lost 10% of its value instead of earning 10%, instead of gaining $520 after-tax, you would have lost $1,200 ($780 after-tax).

None of that really seems worth all the hassle of dealing with a loan, but what if we made the loan a lot bigger? What if we borrowed $1 million instead of just $10,000? Now we're looking at a possible $59,000 gain with a 10% gain and a $78,000 loss with a 10% loss on the investment. More money doesn't make someone a different person. It just makes them more of what they already are. In the same way, more leverage doesn't change an investment, it just makes it more of what it already is. If it was going to perform well before, it is now going to perform really well and vice versa. However, when you don't really know in advance how something will do—and with the added concern of margin calls—it seems an ounce of caution is in order.

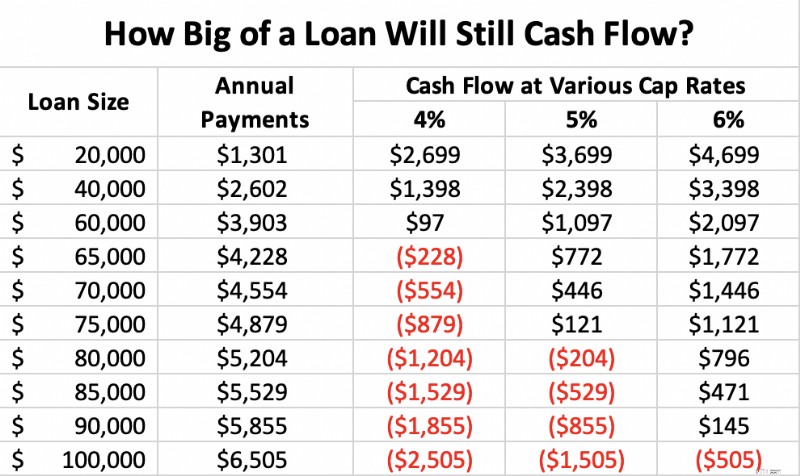

While we're on the subject of investing on margin, it's worthwhile to point out that most real estate equity investments are purchased on margin. Leverage, i.e. the use of debt to buy the investment, is routinely used, primarily to facilitate the raising of capital but also to boost returns. In our example above, we just looked at $10,000 and $1 million in borrowed money. But with most real estate investments, the purchase is only partially completed with borrowed money. Many investors wonder how much they should borrow. They want to be protected and to get out of the investment without bringing money to the table if it all goes bad, but perhaps more importantly, they want the investment to be cash flow positive so they can hold on to it long-term even if its value drops temporarily.

No matter how much money you make at your day job, you can only carry so many negative cash flow properties for so long before you go bankrupt. But you can carry an infinite number of cash flow positive properties.

You can figure out your required “cash flow positive down payment” by running the numbers on your investment, but most of the time, you're going to come up with a number that suggests you put down 25-35% of the investment on any halfway decent deal. With that size of a down payment, a decent property should be cash flow positive. You will also notice that most private real estate syndications and funds use about the same amount of leverage.

Consider a $100,000, cap rate 4-6 property (meaning if it were paid off, it would provide a $4,000-$6,000, 4%-6% cash-on-cash return to the investor). If, after all of its costs, it can generate $4,000-6,000 in cash, then it suggests you could pay up to $4,000-6,000 in mortgage costs and still avoid a negative cash flow situation. If you get a 30-year fixed mortgage at 5%, your annual payments would be as follows at the various cap rates:

As you can see, whether a property cash flows depends on three factors:interest rate, cap rate, and down payment. With a 5% interest rate and a 4% cap rate, you need to put down a lot of money, 40% in this case, to ensure positive cash flow. When the interest rate and cap rate are equal (5% in this case), the property cash flows with a 25% down payment. When the cap rate is higher than the interest rate, you can put down as little as 10% and still have positive cash flow. As I write this [2021] , cap rates in various cities across the country average at most 3%-4%, and investment property interest rates are in the 3.5%-4.5% range, suggesting you'd better plan to put down at least 25%-33% as a down payment to stay cash flow positive—and a whole lot more than that in Miami or Naples, Florida.

This is the most common question I get, particularly from new attendings who have more great uses for cash than they have cash. I have written about it many times, but this particular question does not lend itself to easy answers. It always depends, and there are a lot of variables:

Here is a priority list that may help guide you that no one will argue with too strenuously:

Honestly, the most important thing is not exactly what your money goes toward. Paying down debt is a good thing. Investing is a good thing. Both build your net worth. The most important thing is how much of your income goes toward building wealth either by paying down debt or investing. Concentrate on that.

I find it interesting to talk to wealthy people about how they did it. The same drive that leads the wealthy to save money in order to invest it also drives them to save money in order to pay down debt. In my experience, rich people do both, middle-class folks try to decide whether to pay down debt or invest, and the poor do neither. There's probably a mindset lesson there.

My family chose to be debt-free. We paid off our mortgage in 2017 and haven't looked back. In some ways, it's just a status symbol. By doing it, we get to make videos like this one:

There are some benefits of being debt-free besides just a status symbol. These include:

Some people consciously and deliberately choose not to seek the debt-free life for financial reasons that have nothing to do with overspending. They note that debt has a substantial number of financial benefits including increased investment returns, less overall risk, and lower taxes. In this section, I'll explain how that can be, as well as provide some guidelines as to how you can profitably incorporate debt into your financial plan without taking unsafe risks.

As we discuss debt and its uses, it is important to understand the characteristics of any given debt before you decide to incorporate it into your plan.

As you can see, the ideal loan to carry to invest is with a long-term, fixed-interest rate, unsecured, deductible, non-callable debt. Unfortunately, there is no debt that meets all of those characteristics. The usual choices are:

We've talked about how investing on leverage can raise returns, but investing is not just about returns. It is also about risk control. When you take on debt, you introduce leverage risk into your portfolio. Investing is a single-player game:you against your goals. You should ask yourself, “How much leverage risk do I need to take in order to reach my goals?” Many high-income professionals like doctors will appropriately conclude that they don't need to take any leverage risk at all, but some do because they had a late start, don't want to save much money, or simply have particularly aggressive goals.

However, what if you could take less overall risk by introducing leverage risk to the portfolio? There are other risks in investing, such as market risk, sequence of returns risk, liquidity risk, and inflation risk.

Thomas J. Anderson points out in his Value of Debt books that there are two ways to get to a 9% return. The first is to invest in assets that return 9%. The second is to invest in assets that return 6% but leverage them with debt. It is possible that you can have a lower volatility portfolio with debt than without. So while you have introduced leverage risk, you have reduced market risk.

One of the biggest risks in retirement is sequence of returns risk. This is the risk that despite having adequate average returns over the investment period, the retiree runs out of money because all of the crummy returns came first and decimated the portfolio while the retiree was withdrawing from it to live. This risk is highest right around the time of retirement, perhaps the last two or three years before you retire, and the first 5 years afterward, because that is when the portfolio is largest. By using debt earlier in the accumulation phase and perhaps later in the decumulation phase, you can spread out the amount of time that such a large part of the portfolio is exposed to market risk.

Rather than decreasing your asset allocation around the time of retirement, you simply reduce your leverage risk around that time. Alternatively, rather than selling low if stocks plummet shortly after you retire, you simply take out a margin loan against the remaining assets and spend that, so you do not sell your stocks low. Later, when the portfolio recovers, you can sell the stocks and pay off the loan.

Sometimes people run into liquidity risk. They simply need cash now and despite being wealthy, they have no cash. It might be tied up in long-term, illiquid investments or perhaps it is just in volatile investments, like stocks, they do not wish to sell while they are down in a bear market. Cash obtained from borrowing can provide cash and liquidity in these times.

Another big risk retirees face is inflation risk. This risk is much lower for accumulators, because they have jobs with wages that tend to rise with inflation and because they also have fixed debt that becomes easier to pay off in the event of high inflation. Retirees can also protect their nest egg with long-term, non-callable, fixed low-interest rate debt. It works exactly the same way. There is obviously a cost to this protection (the interest), but that can be offset or even superseded by additional investment earnings from the borrowed but invested money.

Most of us also face substantial liability risk. Debt can also improve our asset protection. For example, in some states very little home equity is protected. If you have another place to put that money that has better asset protection (retirement accounts or, in some states, a whole life policy), you could “equity-strip” that home equity out with a mortgage or HELOC and move it into the better-protected vehicle. Likewise, you could maintain loans against investment properties inside LLCs to limit the amount of money available to a creditor of the LLC. A margin loan against a taxable account could work similarly.

Thus, there are a number of strategies and circumstances where additional debt could actually lower your overall risk instead of increasing it.

A really cool aspect of debt is that it provides spendable cash without any tax consequences. You can borrow against your house, your car, your investment account, your rental properties, or your whole life insurance policy and get a lump sum of non-taxable cash. It isn't income. It's debt. So, you don't have to pay taxes on it. In fact, when combined with the step-up in basis at death on your house, investment account, or rental properties, or the tax-free death benefit of a whole life policy, there are no taxes due for you or your heirs for the use of that money.

Essentially, one can elect to pay interest instead of taxes. People accuse the wealthy of doing this to avoid paying “their share” of taxes, but in reality, it is a tax strategy available to all of us with anything to borrow against. It isn't always the right strategy—particularly if the interest rate on your debt is high, life expectancy is long, and the basis on your asset is also high. But it is silly for someone on hospice to sell low basis investments instead of just borrowing against them.

In retirement, you don't really need income. What you need is spendable money. The things you pay for do not care where the money to pay for them came from. It can be borrowed money, it can be tax-free Roth IRA money, it can be partially taxable withdrawals from your non-qualified account or Social Security, it can be tax-sheltered income from investment properties, or it can be fully taxable withdrawals from a tax-deferred account. The choice is yours, but there can certainly be times where the right option is borrowed money.

If you subscribe to this idea that borrowed money can boost your returns, lower your risk, and decrease your taxes, you will eventually come around to two questions. The first is what debt you should actually carry. There are lots of options here, including auto loans, RV loans, parental student loans, and more, but most people settle into some combination of

As I mentioned before, money and debt are fungible, so it doesn't really matter what secures the loan so much as the characteristics of the loan—term, interest rate, security, deductibility, and callability. You can even take out debt on stuff that your kids are using as a method of transferring money to them during your life.

The second question you will run into is how much debt you should take on. I briefly mentioned Thomas J. Anderson above, who has spent far more time thinking about this question than I have. He basically advocates that individuals act like corporations do and take on an optimal amount of debt. His conclusion? That your debt should get to within 15-35% of your total assets by the time you are within 20 years of retirement. Then you should maintain that “optimal ratio” throughout retirement as best you can through spending, taking out additional loans, and trying not to pay down the loans you have by using interest-only mortgages.

So if you have a $600,000 house, $1 million in retirement accounts, a $400,000 rental property, and a $1 million taxable account ($3 million total), he recommends you have somewhere between $450,000 and $1.05 million in attractive debt. Not too much, not too little. Adjust to your own taste, debt tolerance, and debt availability.

But Anderson is advocating for “enriching debt”—debt that helps you get richer. He's not talking about working debt (needed student loans, practice loan, needed mortgage, needed small car loan) or oppressive debt (that 29% credit card and fat 8% car loan keeping you poor). Plus, his books are so full of cautions about who should actually attempt this that it leaves you wondering whether you're even in that elusive group. Should you be like Katie and me, pay off your debts, and live the debt-free life? Or should you seek a moderate path and carry substantial debt to the grave in hopes of boosting returns, lowering risk, and decreasing your taxes? I cannot say, because the answer depends too much on you. Different strokes for different folks. Here are some considerations as you decide, however.

I will use some of Thomas's rules and some of my own.

Are you a devout Muslim, evangelical Christian, or a member of The Church of Jesus Christ of Latter-day Saints? Carrying debt into retirement probably isn't compatible with your religious beliefs, nor is it required for success for most high-income professionals. This approach probably isn't for you.

The vast majority of people clearly are not capable of handling debt well. I mean, 45% of Americans are carrying credit card debt month to month. This is not a good plan for them. If you're used to borrowing to buy cars, boats, and other consumer goods, this may not be a good idea for you, either.

In my experience, most doctors are way too comfortable with debt. Most young doctors have ratios that are way over what Thomas would recommend already. Consider a dentist with a $500,000 practice loan, a $500,000 student loan, a $500,000 mortgage, and a $500,000 house. What's that ratio? At least 150%, five times as much as that 15-35% ratio. Even if the dentist buys into the “keep an optimal amount of debt forever” philosophy, they need to really attack that debt and build assets to drop that ratio rapidly.

Maybe you're in a situation where debt is not going to be easy to get. Maybe you're 60, retired with inexpensive cars, a $2 million IRA, a $300,000 paid-for house, no kids, and no taxable account. Where are you going to get a $300,000-$600,000 debt with good terms? 당신은 그렇지 않습니다. This strategy really isn't an option for you.

Leverage risk is real and sends people to bankruptcy court all the time, even previously successful real estate investors. What happens if you lose your job and the stock market drops 75% and the value of your home drops 40%? Are you still OK? Can you still pay all of your living expenses? Can you still make your debt payments? If not, your debt ratio is too high, even if it is in the 15%-35% range.

We're all human. We get tempted to buy stuff we shouldn't buy with money we don't have. You might have an opportunity to take on a high-quality debt. But you might already be at your goal of a 20% debt ratio. Therefore, you should not take on this new debt. You don't want to just collect investments and you don't want to just collect debts. They all need to be part of the plan. You need to make sure the other side of the plan is smart, too. Are you borrowing all this money just to put it into Bitcoin, Tesla stock, and inverse leveraged ETFs, or are the investments you are purchasing sensible, long-term investments such as index funds and appropriately priced rental real estate?

The object is to get rid of low-quality (high-interest rate, short-term, non-deductible) debt while building an optimal debt ratio of high-quality debt. It can make sense to borrow against your portfolio or house to pay off credit card debt in order to save on interest rate, but you have to stay within your ratios or you could get in trouble. It would be terrible to lose the ability to service the debt right after converting an unsecured debt to a secured one!

The bottom line is:

If the answer to any of those is no, I would instead recommend the pathway I have taken—pay off your debts rapidly but in a methodical, rational way and live debt-free for the rest of your life.

What do you think about debt? How have you used debt in your investing life? How have you gotten in trouble with it? Do you plan to pay off your debts in a rapid fashion, in a moderate fashion, or continue to use debt strategically throughout your life?