나는 빚 없이 학부 교육을 마치는 것이 전적으로 가능하다고 생각하지만, 의사, 치과의사, 변호사 및 기타 고소득 전문직 종사자들에게는 그럴 가능성이 점점 줄어들고 있습니다. 이 긴 게시물에서는 학자금 대출 용서 프로그램부터 학자금 대출 재융자에 대한 최고의 거래까지 성가신 학자금 대출 관리에 대해 알아야 할 모든 것을 다룰 것입니다. 이 학자금 대출 101을 고려하십시오. 저는 게시물을 교육 수준별로 나누었는데, 이를 통해 귀하에게 적용되는 부분으로 건너뛸 수 있기를 바랍니다. 이 게시물이 의과대학 빚의 부담으로 어려움을 겪고 있는 사람들에게 작은 희망이 되기를 바랍니다.

학자금대출은 학생들의 교육비와 그에 따른 생활비를 지불하기 위해 학생들에게 발행되는 대출입니다. 따라서 다른 목적으로 이를 획득하거나 사용하는 것은 사기로 간주됩니다. 모기지나 자동차 대출과 달리 이러한 대출은 압류될 수 없습니다. 비용을 지불하지 않으면 누구도 개두술을 받으러 오지 않습니다. 그러나 그 사실 대신에 그들은 그들을 다소 부담스럽게 만드는 두 가지 조건을 가지고 있습니다:

학교에 필요한 것보다 더 많은 돈을 빌리지 마십시오. 일부 재정 지원 사무소에서는 생활비를 충당하기 위해 추가 대출을 권장합니다. 생활비를 충당하는 데 필요한 최소한의 금액을 꺼내십시오. 어떤 사람들은 대출금으로 호화로운 생활을 하는 데 필요한 것보다 더 많이 빌릴 수도 있습니다. 이것은 결코 좋은 생각이 아닙니다. 학자금 대출을 받는 방법에 대해 자세히 알아보려면 의과대학에서 부채를 사용하는 올바른 방법을 확인하세요.

학자금 대출로 내리는 결정은 쉽게 수만 달러, 심지어 수십만 달러의 가치가 있을 수 있습니다. 그러나 빠르게 변화하는 연방 상환 프로그램으로 인해 이를 관리하는 것이 매년 점점 더 복잡해지고 있습니다. 이 게시물을 학습 도구 및 가이드로 사용하는 것이 좋지만 권장 학자금 대출 상담사 중 한 명을 방문하여 귀하의 고유한 상황에 맞는 계획을 세우십시오. 그들은 이러한 프로그램에 대해 잘 알고 있으며 최신 정보로 최신 정보를 제공해 귀하의 비용을 최대한 절약해 드립니다.

연방 학자금 지원(FASFA) 무료 신청서를 작성하여 연방 학자금 대출을 신청하세요. 귀하의 결과에 따라 귀하의 재정 지원 제안이 결정됩니다.

학자금 대출을 받기 전에 대출 상환 의무를 이해하고 대출 조건에 동의하는 구속력 있는 계약서인 기본 약속어음에 서명하기 위해 입학 상담을 받아야 합니다. 자세한 내용은 학교 재정 지원 사무실에 문의하세요.

개인 학자금 대출 신청 절차는 다양할 수 있지만 대부분의 개인 대출 신청은 웹사이트를 통해 접속할 수 있습니다.

연방 및 민간 학자금 대출은 일반적으로 모기지나 자동차 대출과 같은 다른 할부 대출과 동일하게 취급됩니다. 각 결제를 제때에 완료하면 신용 기록이 쌓이고 신용 점수도 높아질 수 있습니다. 학자금 대출을 연체하거나 연체하면 신용 점수가 타격을 받을 수 있습니다. 연체 또는 채무 불이행에 가까워지기 전에 적절한 소득 기반 상환(IDR) 계획에 등록하여 지불 비용을 감당할 수 있는지 확인하십시오.

집을 구입하려는 학자금 대출이 많은 의사는 소득 대비 부채 비율이 높아 모기지 확보가 어려울 수 있습니다. 고려해야 할 옵션은 의사 모기지 대출(의사 모기지라고도 함)을 사용하는 것입니다. 의사모기지론은 학자금 대출 부채비율이 높은 고소득자에게 특혜를 주는 대출 프로그램이다. 의사 모기지는 치과의사, 수의사, CRNA, PA, 변호사 등이 이용할 수도 있습니다.

자세한 내용은 여기를 참조하세요.

의사 담보 대출

학자금 대출은 연방 대출이라는 두 가지 주요 유형으로 나뉩니다. (직접 대출이라고도 함) 및 개인 대출 .

교육을 위해 대출하는 방법을 결정할 때 사립 대출보다 연방 대출을 먼저 선택하세요. 연방 대출은 초기에 더 낮은 이자율을 제공할 수 있으며 개인 학자금 대출은 제공하지 않는 풍부한 연방 보호를 제공합니다. 개인 대출은 소득 기반 상환, 공공 서비스 대출 용서 또는 IDR 용서를 제공하지 않습니다. 사망 또는 완전한 장애 시 항상 탕감되는 연방 학자금 대출과 달리, 민간 학자금 대출 탕감 정책은 덜 표준화되어 있으며 대출 기관에 따라 다릅니다.

연방 대출은 일반적으로 이자가 낮으며 특별 소득 기반 지불 계획 및 용서 계획도 있습니다. 일반적인 규칙은 개인 대출을 받기 전에 연방 대출 프로그램에서 빌릴 수 있는 금액을 최대한 활용하는 것입니다.

그러나 일부 외국 의과대학은 연방 대출 자격을 갖추고 일부는 그렇지 않습니다. 외국 의과대학에 지원하고 등록하기 전에 이 페이지의 목록을 꼭 참고하세요. 카리브해 의과대학은 연방 대출 자격이 없는 것으로 악명 높지만, 일치율이 가장 높은 학교(세인트 조지스, 사바, 캐리비안 아메리칸 대학교, 로스)는 자격을 갖추는 경향이 있습니다.

연방 학자금 대출은 통합될 수 있습니다. 이 과정에서 수많은 대출을 하나의 대출로 묶어서 이자율을 평균한 후 1/8포인트 단위로 반올림합니다. 이는 일반적으로 이자율이 낮아지는 재융자 과정(민간 대출 기관에서만 가능)과 다릅니다.

자격 요건은 다음과 같습니다:

보조금 대출은 교육부가 학부 과정에 대한 이자를 지불하는 대출입니다. 자격을 갖춘 대출자는 재정적 필요를 입증해야 하며 학교에 다니는 동안 발생한 이자를 지불할 필요가 없습니다. 대학원 및 전문 학위 프로그램은 더 이상 보조금 대출을 제공하지 않습니다. 보조금이 없는 대출은 귀하가 이를 받는 순간부터 이자가 발생하기 시작합니다. PLUS 대출(졸업생 또는 학부모)은 보조금이 없는 대출입니다. 보조금을 받지 않은 대출을 받기 전에 보조금을 받은 옵션을 모두 소진하는 것이 좋습니다.

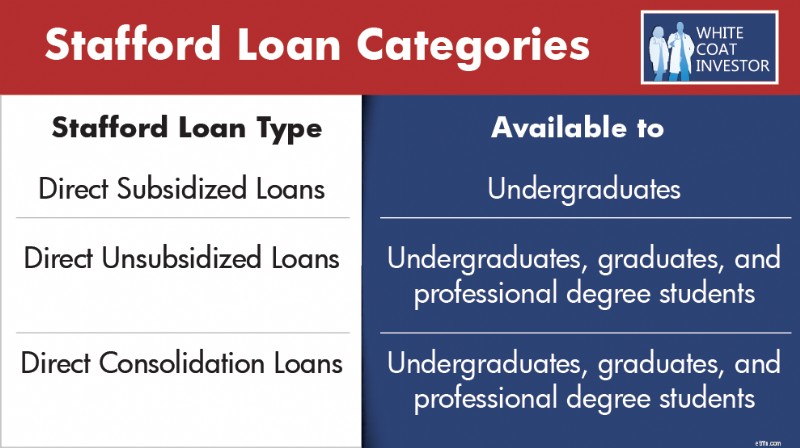

Stafford 대출은 Direct Stafford 대출로도 알려져 있으며 William D. Ford 연방 직접 대출(직접 대출) 프로그램에서 제공됩니다. 스태포드 직접 대출은 가장 일반적인 학자금 대출이며 현재 고등 교육 비용을 충당하기 위해 발행되고 있습니다.

스태포드 대출에는 3가지 카테고리가 있습니다:

통합 전 Stafford Loans의 자격은 다음과 같습니다.

Grad PLUS 대출이라고도 알려진 PLUS 대출은 Direct 및 FFEL 대출 프로그램에서 제공됩니다. 차용인은 수업료를 충당하기 위해 Stafford Loans를 소진한 후 이러한 대출을 받습니다. Grad PLUS 대출은 중단됩니다 2026년 6월 30일 이후 프로그램 대출을 시작하는 사람들을 위한 것입니다.

통합 이전에는 Direct PLUS Loans를 이용할 수 있습니다. :

통합 이전에는 FFEL PLUS 대출이 가능합니다. :

통합 후 FFEL PLUS Loans는 다음 혜택을 누릴 수 있습니다.

Parent PLUS Loans는 자녀의 교육비를 조달하기 위해 부모에게 발행됩니다. 학부생, 대학원생 및 전문 학위 학생에게 제공됩니다. 기존에는 Parent PLUS 대출의 경우 대출 한도가 없었습니다. 그러나 OBBBA는 자녀 1인당 최대 65,000달러, 연간 최대 20,000달러의 대출 한도를 시행했습니다.

통합 이전에 Parent PLUS Loans는 다음에만 적합합니다:

통합 후 Parent PLUS Loans는 다음 혜택을 받을 수 있습니다.

OBBBA에 따라 IDR 프로그램 자격을 유지하려면 상위 PLUS 대출을 2026년 7월 1일 이전에 통합해야 합니다. 즉, IDR 계획에 대한 자격을 얻으려면 올해 최대한 빨리 부모 PLUS 대출을 통합해야 합니다. 해당 날짜 이후에 통합되거나 빌린 대출은 현재 IDR 계획에 적합하지 않습니다. ICR(소득 조건부 상환) 계획은 역사적으로 상위 차용인이 사용할 수 있는 유일한 IDR 계획이었습니다. 과거에는 차용인이 보다 넉넉한 IDR 계획을 이용하기 위해 복잡하고 번거로운 이중 통합 프로세스를 거쳐야 하는 경우가 많았습니다. 이제 상위 PLUS 대출이 2026년 7월 1일 이전에 통합되는 한 ICR 계획에서 한 번 지불한 후 더 관대한 소득 기반 상환 계획의 자격을 얻게 됩니다. 이중 통합 허점은 더 이상 상위 대출자에게 문제가 되지 않습니다.

2010년 이전에는 FFEL(Family Federal Education Loans) 프로그램이 연방 학자금 대출의 주요 원천이었습니다. 프로그램은 2010년에 종료되었습니다 이제 모든 대출은 위에 언급된 직접 대출 프로그램에 따라 발행됩니다.

통합 전 FFEL 대출은 다음과 같은 혜택을 받을 수 있습니다.

통합 후 FFEL 대출은 다음과 같은 혜택을 받을 수 있습니다.

연방 퍼킨스 학자금 대출 프로그램은 특별한 재정적 필요가 있는 학생들에게 대학 학자금을 제공하기 위해 만들어졌습니다. 프로그램은 2017년 9월 30일에 종료되었습니다. .

Perkins Loans는 통합될 때까지 소득 기반 상환(IDR) 또는 공공 서비스 대출 면제(PSLF)와 같은 여러 연방 프로그램의 적용을 받을 수 없습니다.

통합 후 Perkins 대출은 다음 혜택을 받을 수 있습니다.

대부분의 연방 학자금 대출은 지급 시 대출 수수료가 부과됩니다. 수수료는 학교에 등록하는 동안 받는 각 대출금에서 비례적으로 공제됩니다. 이는 실제로 받는 돈이 빌린 금액보다 적다는 뜻입니다. 그리고 귀하는 받은 금액뿐만 아니라 빌린 금액 전체를 상환할 책임이 있습니다.

과거에는 개인 학자금 대출이 일반적으로 대출자가 최대 연방 대출 한도에 도달한 후에만 사용되었으며 Grad PLUS 대출은 대부분의 나머지 자금 요구를 충족했습니다. 2026년 가을부터 대출을 시작하는 학생들의 경우 Grad PLUS 대출은 더 이상 선택 사항이 아니며, 이는 개인 대출이 대출 절차 초기에 사용될 가능성이 높다는 것을 의미합니다. 연방 대출을 받을 자격이 전혀 없는 특정 국제 의과대학에 다니는 학생에게는 예외가 남아 있으며, 민간 대출이 유일한 선택일 수 있습니다.

공동 서명자는 사립 학자금 대출을 받을 때 필요하지 않지만 대출자가 대출을 확보하고 더 나은 조건을 얻는 데 도움이 될 수 있습니다. 공동 서명자에 대한 몇 가지 기준은 다음과 같습니다:

맨 처음부터 시작합시다. 학자금 대출로 얼마를 받아야합니까? 사실은 학부 과정에서 돈을 빌릴 필요가 없으며, 돈을 빌려야 하는 사람도 거의 없다고 생각합니다. 학부 교육기관의 출석 비용에는 매우 넓은 범위가 있으며, 실제 교육 품질의 범위보다 훨씬 더 넓습니다. 몇 가지 현명한 결정을 내리고 학부생으로서 열심히 노력함으로써, 결국 의사가 될 대부분의 사람들은 학부 빚을 전혀 지는 것을 피할 수 있습니다. 학사 학위를 부채 없이 마치기 위해 취할 수 있고 취해야 할 단계는 다음과 같습니다:

학사 학위를 위해 대출을 받게 된다면 보조금을 받는 부채만 감당하도록 노력하세요. 그렇게 하면 의과대학과 레지던트 기간 동안 관심이 쌓이지 않을 것입니다. 의과대학을 위해 대출을 받을 예정이라면, 해당 목적을 위해 학부 4학년 말에 대출을 받는 것을 고려해 보십시오. 이자율이 낮아질 뿐만 아니라(2025-2026 학년도의 경우 6.39% 대 7.94%) 첫 $5,500도 보조금을 받게 됩니다.

자세한 내용은 여기를 참조하세요.

빚 없이 학부생을 탈출하세요!

의과대학에 입학하는 방법

최고의 학자금 대출은 절대 받지 않는 대출입니다. 학교에 짊어져야 할 빚을 줄이는 방법에는 여러 가지가 있습니다.

의과대학 및 치과대학 학생을 위한 연방 학자금 대출이 대대적인 변화를 거쳤습니다. One Big Beautiful Bill Act가 2025년 7월에 법으로 제정된 이후로 연방 대학원 PLUS 프로그램은 2026년 6월 30일 이후 대출을 시작하는 사람들에 대해 제거됩니다. 거의 20년 동안 Grad PLUS 대출을 통해 대학원 및 전문 학위 학생들은 출석 비용 전액과 표준 직접 보조금 한도를 넘어 대출을 받을 수 있었습니다. 이제 2026년 가을 이후에 시작하는 프로그램에는 해당 옵션이 더 이상 존재하지 않습니다. 프로그램 날짜 이전에 대출을 시작한 경우 이전 대출 규정이 적용됩니다.

대학원 및 전문 교육(의과/치과 대학)을 위한 연방 대출은 보조금이 없는 직접 대출로 제한됩니다. 보조금 없는 대출 한도는 연간 최대 $50,000이며, 의과대학이나 치과대학의 경우 평생 한도는 $200,000입니다. 대학원 등록금은 연간 $20,500로 평생 한도는 $100,000입니다. 모든 연방 대출(학부/대학원/전문직)에 대한 평생 한도는 $257,500입니다. 많은 학생들은 더 낮은 연방 상한선을 적용하여 기관 및 사립 학자금 대출을 통해 교육 비용을 보충해야 합니다.

자세한 내용은 여기를 참조하세요.

의과대학 등록금을 지불하려면 군대에 가야 하나요?

의예과 및 의과대학생을 위한 재정적 조언

인턴으로서 순자산 0달러 달성

의과대학을 졸업하면 학자금 대출 관리를 개인 대출이라는 두 가지 범주로 나누는 것이 가장 좋습니다. 및 연방 대출 .

원칙적으로 의사들은 학자금 대출을 갚기 때문에 발생하는 이자를 최소화하는 것이 중요합니다. 가장 좋은 방법은 의과대학을 졸업하자마자 학자금 대출을 재융자하는 것입니다. 이자율을 낮추고 다른 방법보다 낮은 지불금(월 $0-$100)을 즐길 수 있는 "레지던트 프로그램"을 제공하는 몇몇 회사가 있습니다. 해당 지불금은 대출에 대해 발생하는 이자를 충당하지 않지만, 이자율을 6%-10%에서 3%-6%로 낮추게 되므로 전체적으로 더 적은 이자를 지불하게 됩니다. 다음 WCI 파트너는 특별 상주 학자금 대출 재융자 프로그램을 제공합니다:

Laurel Road 월 $100 지불

SoFi $100/월 결제

스플래시 $100/월 결제

사립 학자금 대출 기관은 일반적으로 거주 기간 동안 대출금을 상환하는 네 가지 주요 방법을 제공합니다. 일부 프로그램에서는 학교에 재학 중인 동안 다양한 수준으로 지불을 연기할 수 있지만 귀하 또는 귀하의 학교가 대출금을 받은 날부터 이자가 계속 발생한다는 점을 기억하십시오.

재학 중에도 대출금 지급부터 즉시 지급이 시작됩니다. 이는 네 가지 지불 옵션 중 가장 낮은 비용으로 첫날부터 원금과 이자를 모두 지불할 수 있습니다.

이 프로그램에서는 학교에 등록되어 있는 동안에만 이자를 지불하게 됩니다. 대출금 잔액이 상환되지 않더라도 이자를 계속 지불할 수 있으며 더 큰 혜택을 누리지는 못할 것입니다. 학업이 끝나면 대출 잔액을 확인하세요.

이 옵션을 선택하면 학교에 등록하는 동안 낮은 고정 금액을 납부해야 합니다. 거주 기간이 끝나면 더 많은 대출 잔액을 가지게 되지만 전체 부채 금액을 줄이는 방향으로 나아갈 것입니다.

완전히 연기하기로 선택한 경우 졸업 후 6개월의 유예 기간을 포함하여 학교 기간 동안 필요한 비용을 지불할 필요가 없습니다. 이는 네 가지 결제 옵션 중 가장 비쌉니다.

많은 연방 학자금 대출 대출자는 대출 상환을 위해 표준 10년 지불 프로그램에 등록합니다. 즉, 10년에 걸쳐 120회의 고정 지불금으로 대출금을 상환합니다. 대출 금액과 이자율을 기준으로 한 이러한 월별 지불액은 6자릿수 부채를 가진 일반적인 저소득층 거주자가 감당할 수 있는 것보다 훨씬 높습니다. 그러나 소득 기반 상환(IDR) 프로그램은 대출자가 소득 및 가족 규모에 따라 대출금을 상환할 수 있는 다른 옵션을 허용하는 지불 계획입니다.

IDR 프로그램은 말 그대로 학자금 대출에 대한 표준 지불금을 지불할 여유가 없는 거주자에게 매우 유익합니다. 재량 소득의 일정 비율을 기준으로 지급하는 경우 월 납부액은 최저 $0이지만 $100-$400 범위일 가능성이 높습니다. 1년에 한 번 IDR 계획을 준수하기 위해 소득을 증명해야 합니다(일반적으로 세금 신고서 또는 급여명세서 제출).

또한 IDR 프로그램은 PSLF(공공 서비스 대출 탕감) 및 장기 소득 기반 상환 탕감과 같은 연방 대출 탕감 프로그램에 대한 적격 상환 프로그램입니다.

일부 IDR 계획의 주요 단점은 발생한 이자를 감당할 수 없다는 것입니다. $200,000, 6% 학자금 대출의 이자가 매월 $1,000가 발생한다는 점을 감안할 때 IDR 지불은 일반적으로 발생하는 이자를 충당할 수 있는 수준에도 미치지 못하므로 거주 기간 동안 대출 규모는 계속해서 커질 것입니다. 나중에 이자를 지원하는 상환 지원 계획(RAP)이라는 IDR 계획을 소개할 예정입니다.

IDR 프로그램은 연방 학자금 대출 관리에 엄청난 복잡성을 추가합니다. 차용인은 최소한의 이자를 받고 최대한의 탕감 수준으로 가장 저렴한 지불금을 찾을 수 있는 옵션을 이해하는 것이 중요합니다. 연방 정부는 소득 기반 상환(IDR) 계획을 주기적으로 변경하며, 가장 최근에는 2025년 7월에 법으로 제정된 OBBBA를 통해 변경합니다.

IDR 프로그램을 이용하면 소득이 없더라도 의과대학 마지막 해에 세금 신고서를 제출해야 한다는 점에 유의하세요. 이렇게 하면 모든 IDR 플랜에서 첫 해에 매우 낮은 지불금(~$0-$10)을 받을 수 있습니다.

소득 조건부 상환 또는 ICR은 실제로 레거시 프로그램에 가깝습니다. 나는 이 프로그램에 등록된 의사를 거의 만나지 못했습니다. ICR 지불금은 재량 소득의 20%입니다. ICR이 다른 프로그램에 비해 갖는 한 가지 장점은 통합된 후에 Parent Plus 대출과 함께 사용될 수 있다는 것입니다. 부모 대출이 없는 한 ICR보다 더 나은 지불 옵션을 제공하는 다른 소득 기반 지불 프로그램(아래 설명) 중 하나를 찾을 수 있습니다.

참고 , 이 결제 프로그램은 OBBBA로 인해 2028년 여름에 종료됩니다. 그 때에는 다른 IDR 계획을 조사해야 합니다. ICR 계획에만 자격이 있는 상위 대출자인 경우 ICR 계획에서 한 번만 지불한 후 더 유리한 IBR 프로그램으로 전환할 수 있습니다.

자격 :부분적인 재정적 어려움이 필요하지 않으며 대출이 처음 발행된 날짜는 중요하지 않습니다.

고려해야 할 대상 :상위 차용인

소득 기반 상환(IBR)은 새롭고 향상된 ICR이었습니다. 주요 기능은 다음과 같습니다:

자격 :이전에 IBR 계획에는 부분 재정적 어려움이라는 소득 요건이 있었습니다. 이 규칙은 OBBBA가 통과되면서 단계적으로 폐지되었습니다. 차용인은 소득이나 부채에 관계없이 IBR에 등록할 수 있습니다.

기존 IBR은 2014년 7월 1일 이전에 미결제 연방 학자금 대출이 한 건 이상 있는 대출자에게 적용됩니다.

새로운 IBR은 2014년 7월 1일 이후에 연방 학자금 대출을 빌리거나 해당 날짜 이후에 새로운 대출을 받기 전에 이전의 모든 연방 대출을 완전히 상환한 대출자에게 적용됩니다.

고려해야 할 대상 :맞벌이 대출자 및 대출 탕감을 받으러 오시는 분. 그러나 기존 IBR 자격이 있는 경우 아래에 설명된 PAYE 또는 RAP 계획을 고려하여 월별 지불액을 낮추는 것이 좋습니다.

Pay As You Earn은 새롭고 향상된 IBR이었습니다. PAYE의 주요 기능은 다음과 같습니다:

참고 , 이 결제 프로그램은 OBBBA로 인해 2028년 여름에 종료됩니다. 그 때에는 다른 IDR 계획을 검토해야 합니다.

자격 :부분적인 재정적 어려움이 필요합니다. So make sure you’re enrolled in PAYE before you become an attending.

To qualify for PAYE, you must have taken out your first federal loan after September 30, 2007, and received a loan disbursement after September 30, 2011.

FFEL loans are not eligible for PAYE unless they are consolidated through a direct federal consolidation loan.

Who Should Consider :Dual-income borrowers and those going for loan forgiveness.

Learn more about partial financial hardship

Learn more about interest capitalization

The Repayment Assistance Plan (RAP) was created by OBBBA in July 2025. The plan is supposed to be available July 1, 2026. Here's the main features:

Eligibility: Any borrower with direct federal student loans.

Who Should Consider :Borrowers with student debt that exceeds their income and/or those considering loan forgiveness.

The Saving on a Valuable Education (SAVE) program was introduced in the summer of 2023 replacing the old Revised Pay As You Earn (REPAYE) Program. The program ultimately ended in December 2025, following the resolution of a long-standing lawsuit brought by the state of Missouri. That litigation, which began in the summer of 2024, placed approximately seven million SAVE borrowers into a processing forbearance. Initially, the forbearance paused both payments and interest accrual through August 2025; once interest resumed, many borrowers began evaluating alternative repayment options for their federal student loans. Eventually all those still in SAVE will be forced to select another IDR plan or be automatically moved.

Partial Financial Hardship (PFH) is an eligibility requirement under the Pay As You Earn Repayment (PAYE) plan. In order to qualify, your monthly payment in PAYE must be lower than the standard 10-year repayment plan. If your payment in PAYE is above the standard 10-year payment, you do not qualify for a PFH,

However, if you’ve enrolled in PAYE while you qualified for a PFH you can continue in the plan even if your income grows and would make you ineligible thereafter. This is very common when income jumps as trainees become attendings.

Resident income = $60K

Student loan debt = $300K

Interest rate = 7%

Household size = 1

Standard 10 year payment = PMT(7%/12,120,300000,0,0) =$3,483

PAYE monthly payment = $60K – $23,940 =$36,060 × 10% =$3,606 / 12 =$301

The payment cap is $3,483 for this borrower. The monthly payment in PAYE is below the standard 10 year payment and eligible for a partial financial hardship.

Attending income = $450K

Student loan debt = $300K

Interest rate = 7%

household size = 1

Standard 10 year payment = PMT(7%/12,120,300000,0,0) =$3,483

PAYE monthly payment = $450K – $23,940 =$426,060 × 10% =$42,606 / 12 =$3,551

The monthly payment in PAYE has passed the standard 10 year payment due to the large increase in income as attending. Since the monthly payments are higher than the standard 10 year payment this borrower no longer qualifies for a partial financial hardship. They are no longer able to enroll into PAYE.

However, if the borrower enrolled in PAYE as a resident or before income has jumped, they are able to stay in the program as long as they don’t switch repayment plans.

Attending income = $441,900

Student loan debt = $300K

Interest rate = 7%

household size = 1

Standard 10 year payment = PMT(7%/12,120,300000,0,0) =$3,483

PAYE monthly payment = $441,900 – $23,940 =$417,960 × 10% =$41,796 / 12 =$3,483

The breakpoint is reached when your payment in PAYE equals the Standard 10 year payment.

Interest capitalization occurs when unpaid interest is added to the principal amount of your federal student loans. This increases the principal balance on the loan. The interest rate is now charged on that higher principal balance increasing the overall cost of the loan.

Principal balance = $200K

Accrued interest = $50K

Total balance = $250K

Interest rate = 7%

Annual interest charge = $200K × 7% =$14K

Principal Balance = $250K

Accrued Interest = $0

Total Balance = $250K

Interest Rate = 7%

Annual interest charge = $250K × 7% =$17.5K

After the accrued interest of $50K capitalizes the annual interest charge will increase by $3.5K

Interest capitalization can be inevitable, but should be avoided when possible. Here's when this happens:

In addition to the more well-known Public Service Loan Forgiveness (PSLF) program, several of the IDR programs have their own forgiveness programs. Remember none of these federal programs have anything to do with private or refinanced loans.

자세한 내용은 여기를 참조하세요.

How to Receive Student Loan Forgiveness

The IBR forgiveness program requires 20 to 25 years of payments, but you may make them while working for any employer or not working at all. New IBR is over 20 years and Old IBR is 25 years. There are two issues with this forgiveness program.

First, most physicians will have paid off their loans completely in less than 20/25 years because after they finish training, their payments will be equal to those under the standard 10-year repayment program. Perhaps that would not be the case for a very poorly paid physician with a very high student loan burden (3,4,5x their income), but for most, there just won't be anything left to forgive.

Second, the forgiveness is taxable, and after 20/25 years, the “tax bomb” could grow to as much or more than the original debt, at least on a nominal (non-inflation adjusted) basis.

PAYE offers forgiveness after just 20 years. However, it is still fully taxable at your ordinary income tax rate in the year you receive forgiveness. PAYE is being phased out in summer 2028, so if you are hitting forgiveness after that date you need to look at IBR or RAP as an alternative. And depending on when you started borrowing, you could end up with more years of payment and a higher monthly payment.

RAP has a generous interest subsidy but is the longest IDR forgiveness track at 30 years. RAP would likely have a lower loan balance leftover for the tax bomb versus PAYE and IBR, but is really only going to work out if you have massive loans as compared to your income. And, do you really want to carry your loans around until you reach your 60s?

Staying up to date on IDR forgiveness can be tough, especially since the timeline can span decades. Temporarily, there was a tracker on studentaid.gov, but the Department of Education took it down. Rather than relying on back of the envelope math, here's a hack that can show you an estimated payment count on your IDR plan.

Public Service Loan Forgiveness is the granddaddy of the federal forgiveness programs and the only one most doctors should be looking at. Not only does it offer tax-free forgiveness, but it also offers it after just 10 years of payments. If you make a bunch of tiny IBR, PAYE, or RAP payments during your training, you may only have to make 3-7 years of “full” payments as an attending before having the rest forgiven. There is a catch, however. You have to be directly employed full-time by a non-profit (501(c)(3)) while making all of those payments in an eligible payment program—or they don't count. You also have to make sure you can prove you made all of those payments since the federal student loan servicing companies have a nasty habit of not being able to count payments accurately.

자세한 내용은 여기를 참조하세요.

Public Service Loan Forgiveness

Dave Ramsey's Bad Advice About PSLF

Many residents are tempted to put their student loans into deferment or forbearance during residency and/or fellowship. This is almost always a mistake. Nothing makes me cry more than to run into a doctor who should only be 2-3 years away from receiving PSLF who had their loans in forbearance during a lengthy training period. I hate breaking the news to them that they've basically thrown away a benefit worth hundreds of thousands of after-tax dollars. It's like working for a year or two as a doctor without being paid at all. Deferment is slightly better than forbearance for some people, but they are both very similar for most high-income professionals with loans—you make no payments but the debt continues to grow, sometimes very quickly.

Deferments are granted in six-month increments by your loan servicer and subsidized loans don't accrue interest. Unsubsidized loans both accrue and capitalize interest. There are several reasons you can get a deferment, but the main one most residents would use is economic hardship, which is limited to just three years. Other reasons include active-duty military, unemployment, and going back to school.

With forbearance, interest accrues on both subsidized and unsubsidized loans. Just think of it as a 12-month pause on payments. For most medical students, it is no less attractive than deferment and it is easier to get. There are two types of forbearance.

I tell you about these two programs and give you these links because people wonder about them, not because I think people should actually use them. If you are seriously considering deferment or forbearance, you would almost surely be better off with an IDR plan. Not only would your payments count toward possible forgiveness down the road, but they may be as low as $0 a month anyway. In RAP, if your payments don't cover all the interest, all of that interest is forgiven by the government and is NOT added back on to the loan amount.

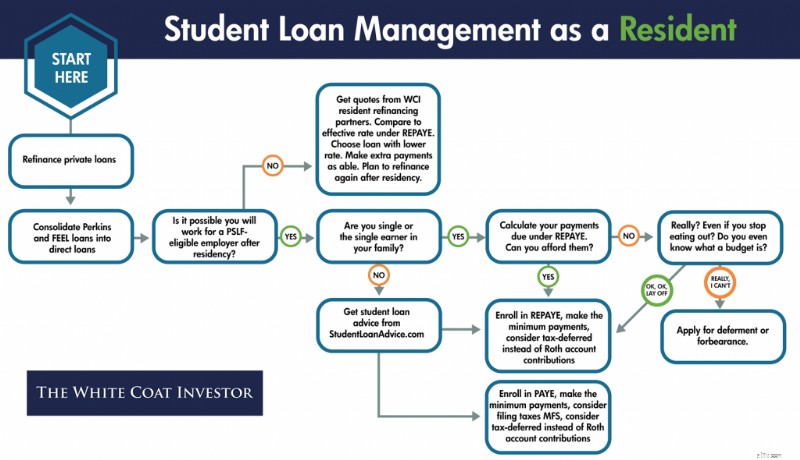

Let's summarize what to do with your student loans if you are a resident. The sooner you know if you are going for PSLF, the easier your decisions become. If you are single, or the sole earner in a married couple, it can also be very easy. But many people would benefit from getting formal advice from a specialist in student loan management. If you are married to another earner and one or both of you is going for PSLF, consider shelling out $400-$700 one-time fee as an intern to get advice. It could save you tens, or even hundreds of thousands of dollars. It is relatively easy for them to identify the red flags that indicate you're doing things wrong and they can help you run the numbers to make the difficult student loan management decisions that involve choosing an IDR program, choosing how to file your taxes, and even choosing whether to use a traditional or Roth IRA or 401(k).

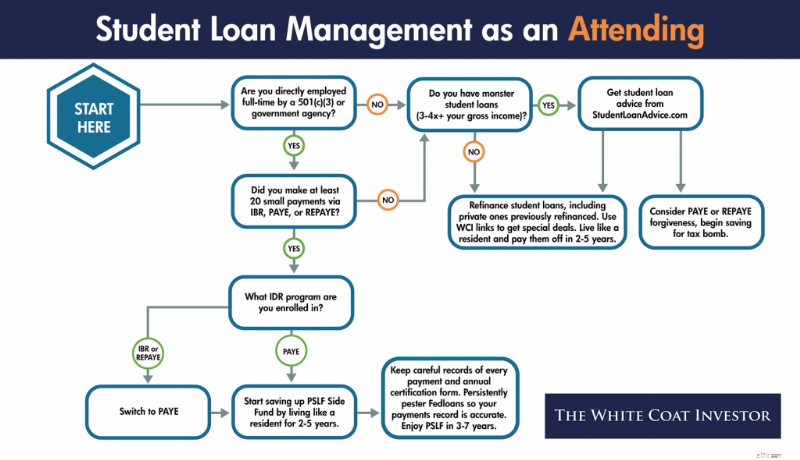

In contrast to residency, where student loan management can be very complicated, involving your taxes and even your retirement account contributions, management as an attending is generally very simple.

Your private loans, which you probably should have refinanced in residency, can be refinanced again and again as long as you can get a lower rate (and you usually can as a new attending). Obviously, refinancing doesn't actually make them go away, but it helps make more of your monthly payments go toward principal instead of interest. The way you make them go away is by living like a resident and dumping a huge sum on them every month. Even half a million in student loans doesn't last long against a five-figure monthly payment assault.

Regarding your direct federal loans, you need to finalize your decision of whether to go for PSLF or not. This is usually relatively easy. If you can answer BOTH of the following questions positively, you should go for PSLF:

If you cannot answer both of those questions positively, refinance your student loans and live like a resident for 2-5 years until they are gone.

자세한 내용은 여기를 참조하세요.

10 Reasons to Pay Off Your Student Loans Quickly

How Fast Can You Get Out of Debt?

The X Factor

What Does Live Like a Resident Really Mean?

Here are the best deals on student loan refinancing I've managed to negotiate with the top student loan refinancing lenders:

The secret to refinancing your student loans is to do it early and often. If you ask your fellow White Coat Investors for their regrets, many say they wish they had done it earlier because it was much easier than they thought. While it may appear intimidating at first, most of the companies will give you an accurate estimate of the rate you will eventually receive in 2 minutes online. You'll need to gather and submit some paperwork, but it's mostly all the same for all of the companies. So once you gather it and submit it to one, it is very easy to submit it to 2 or 3 more (or even all of them). Then just take the one that offers the lowest rate.

The rates offered to you will depend on your credit score, your debt-to-income ratio, and your desired loan terms. Unlike the federal government, which loaned you money just for getting into school, these private companies actually want to make a profit. They only want to loan money to people they think will be able to pay the money back.

The best way to get the lowest rate is to accept a 5-year term and a variable rate. If you are willing to live like a resident for 2-5 years after residency and pay off your loans quickly, these terms should be acceptable to you. While there is some legitimate fear of rising rates with a variable rate loan, the truth is that rates have to rise dramatically and/or early in the term in order for you to come out behind with a variable rate loan. If you can afford the worst-case scenario, I would at least consider a variable rate loan, and run the math under various interest rate scenarios.

Think of a fixed-rate loan as a variable rate loan plus an interest rate insurance policy. Since you should only buy insurance against financial catastrophes, someone planning to throw $10K a month at their loans every month for 2 years should not pay extra for a fixed rate. Just having a little more of your payment go to interest instead of principal for a few months is not a catastrophe. Even if rates rise early and dramatically, it will likely only delay paying the loan off by a month or two for someone truly committed to getting rid of them.

Some doctors fear refinancing because they are worried about what will happen to them if their income drops, if they die, or if they become disabled. This is a good reason to avoid putting a co-signer on your loans, but if you read the fine print you will see that most private companies have some accommodations for these situations. Often they will give you up to a year without payments in difficult situations (although the interest will continue to build). Loans are also often forgiven at death and sometimes even for disability. Be sure to read the fine print before signing on the bottom line so you know what to expect if any of these unlikely situations happen to you. Even if the company does NOT offer a death or disability plan, realize that purchasing enough term life insurance or disability insurance to cover the loans or its payments is likely cheaper than paying the extra interest in the government programs!

A lot of people get confused about loan consolidation, and in fact, use the term consolidating when they mean refinancing.

Consolidating generally means taking a bunch of loans and making one loan out of them. While that may increase the convenience of management, it does not actually reduce the interest rate. In fact, it may increase it. With federal loans, the weighted average of your loans is taken and rounded UP to the nearest 1/8th of a percentage point. You can consolidate your loans with the federal government, but to refinance them you must go to a private company and lose the benefits of federal loans such as the income-driven repayment programs and the forgiveness programs.

So why would anyone consolidate their loans if it increases your interest paid? Aside from the benefit of only having one loan to manage, the main reason is that you can turn some loans that were NOT eligible for IDR plans and PSLF into loans that are. The classic examples are Federal Family Education Loans (FFEL) and Perkins loans. By themselves, they are not eligible for those programs, but if consolidated into a direct loan, they become eligible. If you fall in this situation and want to use the IDR or PSLF programs, consolidate here.

Another reason to consolidate your loans is when you’re fresh out of med school and enrolling in IDR. Consolidation would allow you to opt-out of your grace period and begin making payments 3-4 months earlier. However, it can be a huge mistake for those who’ve been in training for a couple of years or attendings. Payment history is completely wiped out when you complete a direct federal consolidation—meaning those 3 years you’ve done to PSLF would be gone and you’d be starting over. I can’t tell you how many emails I’ve received from docs who’ve done this and were just a few years out from PSLF. Only to have the rug pulled out from them.

Things are a little more complicated for attendings who wish to go for Public Service Loan Forgiveness. These are generally academicians, or at least people who are willing to be academicians for a few years at the beginning of their careers. However, working for the military or the Veterans Administration or other government agencies can also count. There are also a few non-profits out there who directly employ their docs who should qualify for PSLF. Often these jobs pay less than a private practice job, so you need to take into account that sometimes you would be better off with a better paying job and paying off your loans, then going for forgiveness.

The big downside of going for PSLF is that you cannot refinance your loans. Only direct federal loans can be forgiven. So in the event that legislative or regulatory risk rears its ugly head, changing the program, or that you simply change your career goals such that you no longer qualify for it, you will end up paying more interest than you otherwise would have. But for those who stand to get tens of thousands forgiven, I think it is worth running those risks.

In order to maximize how much is forgiven under PSLF, you want to make as many tiny loan payments as possible. That means getting started as soon as possible, and that may be even earlier than you think. The more time you spend in training, the more you stand to have forgiven. If you spend 5 years in a surgery residency, then do a one-year burn fellowship and a one-year trauma fellowship, you may only make three years of “full” attending-size payments, leaving the vast majority of your debt to be forgiven, tax-free.

When going for PSLF, you must continue to make payments in an eligible program. For up to a year after leaving residency, those might still be relatively small payments, further increasing the amount eligible to be forgiven. But eventually, as an attending, you'll be making “real” four-figure payments toward your loans. At this point, IBR or PAYE might be the best program to be in because of the cap on the payments at the standard 10-year repayment program amount. That means if you were using RAP during residency and/or fellowship, you might want to switch to PAYE/IBR. Mortgage-sized student loan payments will start quickly as you juggle several competing financial priorities:

However, it is probably worth it. Of course, if you were in a situation in residency where you weren't going to qualify for a significant RAP subsidy anyway (usually due to a high-earning spouse), you should just use PAYE (or IBR if ineligible for PAYE) instead of RAP all the way through. But remember, under RAP, you could file under Married Filing Separately to avoid having to use the income of your high-earning spouse.

Another major complaint of those going for PSLF is that the student loan servicing companies such as MOHELA provide terrible service. Make sure you stay on top of everything. Not only do you need to be an expert at the requirements of the PSLF program (which of your loans qualify, which repayment programs have payments that qualify toward the 120 required monthly payments, and working full-time for a 501(c)(3)), but you must keep track of all the paperwork, including evidence of every single payment AND a copy of your annual certification forms. The certification is now done electronically (highly recommend over the paper form) and tracked through the studentaid.gov dashboard. Remember, you could end up going to court with the government in order to receive your promised forgiveness. Make sure you have the evidence you need.

In addition, you cannot just assume you will receive forgiveness. Not only could the program change and you not be grandfathered in, but your employment plans may simply change. Going for PSLF does NOT excuse you from living like a resident for 2-5 years out of residency. However, instead of sending those big 4-5 figure payments to your federal loan servicer, you need to send them to yourself. To your investment accounts, to be specific, creating a “PSLF Side Fund.” This way, even if PSLF doesn't happen for you, you're not behind the eight ball.

Hopefully by living like a resident you've been able to max out your retirement accounts AND save this side fund up in a taxable account, and you can simply liquidate the taxable account and use the proceeds to pay off the loans. But even if most of that savings ends up in retirement accounts and you can't (or don't want) to immediately eliminate the loans at that point, at least your net worth will be where it should be.

Let's summarize what to do with your student loans as an attending. Private loans should be refinanced whenever possible and paid off quickly by living like a resident. Federal loans should also be refinanced and paid off quickly unless you are directly employed by a 501(c)(3) AND made a lot of tiny payments during your training.

Remember that SAVE has been eliminated

If you die or are disabled, what happens with your private loans will be dictated by the terms on their promissory notes. Worst case scenario, if you die they are assessed against your estate. Your parents or siblings etc are never responsible for your loans, but your heirs could be indirectly.

In the event of death, your federal loans are discharged. With Parent Plus loans, the loans are discharged if the student OR the borrower dies.

In the event of permanent disability, federal loans are also forgiven. In a temporary disability, however, you may be limited to use of the IDR programs, deferment, or forbearance.

Student loans generally survive bankruptcy, meaning you cannot wipe them out simply by declaring bankruptcy. However, if you can prove undue hardship, you may be able to have them discharged. Defining undue hardship is going to be up to the judge, but I can assure you that if you qualify for it, you're going to be in a terrible place financially either way.

Depending on what happens to your loans at death and disability, consider carrying a little extra term life and disability insurance coverage to make up for it.

In the event of school closure you may be able to have your loans discharged. This tends to come up more in for-profit institutions, but it’s very rare.

In the event of the school falsely certifying your eligibility to receive a loan, you may be eligible for loan discharge. But this is very complex and unusual.

Some people with low-interest rate student loans wonder if they should really pay their loans off rather than invest. While it is intuitively attractive to borrow at a low rate and earn at a higher rate, this decision often ignores two factors.

The first is that most people simply don't invest the difference. Behaviorally, it is more difficult to maintain focus on building wealth once you have decided to make minimum payments and end up spending the money instead of investing.

The second is that an investment that provides a rate of return higher than the guaranteed return available by paying off your loans usually involves significant risk of loss. However, if you would like to carry your loans a little longer in order to invest inside retirement accounts, I think that's okay. But I would still plan to have them paid off within five years of finishing training. The financial muscles you develop paying off your loans quickly are the same ones you will use to build wealth toward financial independence afterward. I do not recall ever meeting a physician who regretted paying off their student loan quickly. In fact, most express a feeling of massive relief such as this email I received a few days ago from a two doctor couple who paid off over $700,000 in student loans in 16 months:

This student debt problem is so huge and overwhelming. I had many poor nights of sleep during training fretting about, “How do we pay off this 3/4 million dollar debt?” I feel now an immense stress has been lifted. We can now go forward and make some real decisions about how we want to live out the rest of our lives.

You can slay the student loan dragon. Sit down and get started today. Figure out where you stand; list out your loans by amount owed, payment, and interest rate and add up the total. Then start working on a plan to handle them. You can do it, the entire White Coat Investor Community is rooting for you!

자세한 내용은 여기를 참조하세요.

Pay Off Debt or Invest?

What's Your Investment-to-Debt Ratio?

Student loans and the many programs and options are challenging to navigate. If you need help, look to StudentLoanAdvice.com, a WCI company that helps the average client save $160,000 in loans! Check it out today!

어떻게 생각하시나요? What other information belongs in the ultimate guide to managing physician student loans? Have you paid off your loans? What other advice do you have about them for your fellow White Coat Investors?