부동산 계획은 우리 대부분이 가능할 때마다 미루는 집안일입니다. 우리는 일반적으로 그것이 흥미롭지 않고 비용이 많이 든다고 생각하며, 더 나쁜 것은 우리 자신의 죽음에 직면하게 만들 수 있습니다. 그러나 이는 재무 계획의 중요한 측면이며 제대로 수행되지 않거나 전혀 수행되지 않으면 상속인에게 큰 혼란을 초래할 수 있습니다.

유산은 죽을 때 남기는 것입니다. 여기에는 귀하의 모든 돈과 모든 물건이 포함됩니다.

유언장을 공식적으로 증명하는 것을 의미하는 검인은 유산(고인의 재산)이 채권자에게 상환하고 유효한 유언장에 명시된 대로 유산의 자산을 분배하는 법적 절차입니다. 이는 비용이 많이 들고 시간이 많이 소요될 수 있으며, 종종 법률 및 관리 비용으로 유산의 상당 부분을 소비하고 몇 달 또는 몇 년 동안 지속됩니다. 대부분의 유산 계획은 이 과정을 최대한 피하는 데 맞춰져 있습니다.

부동산 계획은 다음을 보장하는 과정입니다:

간단하고 비용이 많이 드는 작업일 수도 있고, 적절하게 완료하려면 비용이 많이 드는 전문가의 도움이 필요할 수도 있습니다. 이 모든 것은 개인의 상황과 희망 사항에 따라 다릅니다.

거의 모든 사람이 최소한 약간의 부동산 계획을 세워야 합니다. 확실히, 상당한 자산($20,000 이상)을 취득했고 사망 시 그 자산이 누구에게 돌아갈지 관심이 있다면 유산 계획이 필요합니다. 마찬가지로, 자녀가 한 명이라도 있다면 최소한 유산 계획을 세워야 합니다.

상속 계획에는 여러 가지 업무가 필요하지만 가장 중요한 것은 사망 또는 무능력 상태가 되었을 때 적용되는 다양한 법적 문서를 준비하는 것입니다.

공식적으로 유언장으로 알려진 유언장은 일반적으로 대부분의 사람들에게 필요한 첫 번째 유산 계획 도구입니다. 사람들이 "무유언"(유언 없이) 사망하는 경우, 그들의 자산은 주법에 따라 일반적으로 배우자에게 분배되거나 해당되지 않는 경우 자녀에게 분배됩니다. 귀하의 자산을 친족 이외의 다른 방식으로 분배하려면 유언장이 필요합니다. 유언장의 또 다른 중요한 기능은 귀하가 사망할 경우 귀하의 자녀를 돌볼 사람을 지명하는 것입니다. 순자산이 크게 마이너스인 의대생이라도 자녀가 있다면 유언장이 필요합니다.

대부분의 의사에게 친숙한 유언장 유형이 하나 있는데, 바로 생존 유언장입니다. 이는 일반적으로 귀하가 건강 관리에 관해 스스로 결정을 내릴 수 없게 되는 경우에 대비해 귀하가 원하는 바를 나타냅니다. 또한 일반적으로 귀하가 의료 결정을 내릴 수 없을 때 귀하를 대신하여 의료 결정을 내릴 의료 대리인을 지정합니다. '소생 금지 명령'도 생존 유언장의 한 형태입니다.

나는 매일 유언장을 보지만 그것이 너무 모호하기 때문에 일반적으로 쓸모가 없다고 생각합니다. 그들은 내가 내려야 할 실제 결정에 대해 전혀 언급하지 않는 것 같습니다. 환자가 항생제를 원할까요? IV 수액? 압착기? 삽관/환기? 심폐소생술? 귀하의 가장 가까운 친척이 의료 결정을 내리는 것을 원하지 않는 한 생계 유언장이 크게 필요하다고 생각하지 않습니다. 아마도 생존 유서의 가장 중요한 측면은 귀하가 더 이상 스스로 의료 결정을 내릴 수 없는 경우에 무엇을 하고 싶은지 가족과 논의하는 것일 것입니다. “감히 저를 일주일 이상 인공호흡기 위에 놓아두지 마세요.” 등.

그럼에도 불구하고 변호사를 만나거나 온라인 유산계획 서비스를 이용할 때에도 일반적으로 이 문서가 포함되어 있습니다. 가격도 저렴하고 간편하니 꼭 해보세요. 그러나 사랑하는 사람들과 그것에 대해 이야기하십시오. 그렇지 않으면 나중에 사용할 때 그 제품이 존재하는지조차 알지 못할 수도 있습니다.

생전 유언장과 의료 위임장을 생략하더라도 귀하가 재정을 관리할 수 없을 때 신뢰할 수 있는 가족, 친구 또는 조언자를 지명하는 것이 좋습니다. 이를 지속 재정 위임장이라고 합니다. 연구에 따르면 50대에 최고조에 달하는 재정 상황을 스스로 관리할 수 있는 능력이 있는 것으로 나타났습니다. 우리 모두는 10년이나 20년 전에는 결코 하지 않았을 일을 돈으로 해낸 노인들을 알고 있습니다. 위임장 문서는 일반 문서(모든 내용 포함) 및 평생 문서(지속성)일 수도 있고, 시간과 범위가 제한될 수도 있습니다. 예를 들어, 여행을 하거나 아이들을 조부모에게 맡길 때, 우리는 때때로 아이들을 돌볼 수 있는 제한된 위임장을 제공했습니다. 귀하의 재정적 위임장과 의료 위임장이 동일인일 필요는 없다는 점을 기억하십시오.

이 문서는 사망 시 남기는 것이 좋지만 실제로 법적 문서는 아닙니다. 이는 단순히 고인이 사랑하는 사람이나 유언집행자에게 알리고 싶은 정보를 설명하는 편지입니다. 개인 메시지를 포함할 수도 있고 단순한 지침일 수도 있습니다. 여기에는 다음과 같은 정보가 포함되는 경우가 많습니다:

이 편지의 가장 중요한 점은 최신 내용을 유지하는 것입니다.

이는 의향서의 일부일 수도 있고 별도의 문서일 수도 있습니다. 목록에 다음 문서를 포함시키는 것을 고려하고 해당 문서의 위치를 기록해 두십시오.

취소가능 생전 신탁은 기본적으로 세금을 피하거나 채권자로부터 자산을 보호하기 위한 것이 아니라 검인을 피하도록 설계되었습니다. 돈과 자산은 신탁에 예치되며 귀하가 사망할 때 수탁자는 검인 없이 신탁 문서에 따라 자산을 상속인에게 분배합니다. 물론 신탁 자산에는 여전히 유산세가 부과됩니다. 취소불능 신탁에 비해 취소가능 신탁의 주요 이점은 원할 경우 자산을 통제하고 사용할 수 있으며 언제든지 자산을 "취소"할 수 있다는 것입니다. 자산은 신탁의 이름으로 소유권을 다시 지정하여 신탁에 "예탁"됩니다. 취소가능 신탁은 사망 시 개인 정보 보호를 제공하며(검인은 공개 절차이기 때문에) 대규모 유산에 대해 상당한 시간과 비용을 절약할 수 있습니다. 대부분의 의사는 사망 시까지 수혜자 지정이 없는 대부분의 자산을 취소 가능 신탁에 보유해야 합니다(아마도 그 중 일부라도 신탁을 수혜자로 기재해야 함). 취소가능 신탁의 소득에 대한 세금은 일반적으로 개인 신고서로 전달됩니다.

이러한 신탁은 검인을 피할 수 있다는 점에서 취소 가능한 생전 신탁의 주요 이점을 갖습니다. 그들은 또한 유산세를 피할 수 있는 이점이 있으며, 소득세를 피하는 경우가 많습니다. 이는 취소 불가능한 생전 신탁에 자산을 맡길 때 본질적으로 해당 자산을 포기하는 것이기 때문입니다. 더 이상 그들이 생산하는 자산이나 소득을 사용할 수 없습니다. 소득에 대한 세금은 신탁이나 상속인이 납부해야 합니다(낮은 세율 등급에 속하는 경우 유리할 수 있음).

결코 필요하지 않을 것이라고 알고 있는 돈만 이와 같은 신탁에 맡겨야 합니다. 돌이킬 수 없다는 뜻이 바로 그것이다. 증여세법은 귀하가 신탁한 금액에 적용된다는 점을 명심하십시오. 증여세/부동산세를 부과하지 않고 매년 얼마나 신탁할 수 있는지 알아보려면 해당 주의 숙련된 변호사와 상담하세요. 취소불능신탁은 또한 훌륭한 자산 보호 도구라는 점을 명심하십시오. 자산은 더 이상 귀하의 것이 아니므로 채권자가 이를 압류할 수 없습니다. 취소가능 신탁에는 이러한 이점이 없습니다.

미성년 자녀가 성인이 되어 상속권 전체를 받는 것을 원하지 않거나 장애가 있는 성인 자녀가 있는 경우, 자산이 적절하게 사용되도록 일종의 낭비 신탁이 필요할 수 있습니다. 이 문서에는 엄청난 유연성이 있으며 여기에서 원하는 거의 모든 작업을 수행할 수 있습니다. 무덤에서 그들의 삶을 다스리려고 하면 할수록 더 많은 문제가 발생할 가능성이 있다는 점을 명심하십시오. 가족의 오두막, 묘지 또는 유사한 다세대 자산을 관리하려면 신탁이 필요할 수도 있습니다. 자녀의 전 배우자로부터 자산을 보호하고 싶을 수도 있습니다. 혼전 계약이 없으면 신탁이 유일한 방법일 수 있습니다.

이는 별도의 문서가 아닌 유언장의 중요한 측면입니다. 이는 귀하가 사망한 후 미성년 자녀를 돌볼 사람(후견인)과 자녀가 성인이 될 때까지 자녀에게 남겨진 자산을 관리할 사람(후견인)을 지정합니다. 이들은 동일인이 아니며 아마도 동일인이 아니어야 합니다. 이것이 어려운 결정이라는 것을 알고 있지만 가장 중요한 것은 결정을 내리는 것입니다. 나중에 언제든지 변경할 수 있습니다. 잠재적인 후견인이 아동에 대해 어떻게 느끼는지, 그리고 아동이 잠재적 후견인에 대해 어떻게 느끼는지 모두 고려하십시오. 이상적으로, 그들은 서로를 사랑하고 당신이 원하는 방식으로 아이를 키울 것입니다. 경제적 상황, 직업, 신체적, 정서적 능력, 종교, 자녀의 미래 생활에 영향을 미칠 수 있는 기타 삶의 측면을 고려하십시오. 일반적으로 커플이 아닌 한 사람만 나열합니다. 성인이 되기 전이나 후에 돈을 쓰는 방법을 제한하려면 보호인을 지명하는 유언장뿐만 아니라 신탁이 필요합니다. 마지막으로, 귀하가 지정한 사람에게 귀하의 결정을 알리고 그들이 동의하는지 확인하십시오.

문서 준비 외에 유산 계획의 또 다른 중요한 측면은 모든 퇴직 계좌, 연금, 생명 보험 수혜자 지정이 올바른지 확인하는 것입니다. 이러한 모든 자산은 신탁을 사용하지 않더라도 검인을 거치지 않고 전달됩니다. 이러한 사항을 정기적으로 검토하고 출생, 사망, 결혼 및 이혼과 같은 주요 생활 사건에 대해 업데이트하십시오. 귀하의 생명 보험 및 은퇴 계좌가 전 배우자에게 전달되는 것을 원하지 않으실 것입니다!

원하는 사람에게 "사망 시 지급"으로 거의 모든 유형의 은행 계좌를 지정할 수 있습니다. 이렇게 하면 귀하가 사망할 때 귀하가 지정한 사람이 검인 없이 귀하의 사망 증명서(일반적으로 사망 증명서)를 가지고 은행에 가서 돈을 징수합니다. 또한 주식, 채권, 뮤추얼 펀드와 같은 증권 또는 전체 중개 계좌를 "사망 시 이전"으로 등록할 수도 있습니다. 이에 대한 가장 좋은 점은 이러한 증권의 기초가 귀하의 사망일에 업데이트되므로 귀하의 상속인이 해당 증권을 즉시 판매하는 경우 자본 이득세가 부과되지 않는다는 것입니다. 캘리포니아와 미주리 두 주에서는 자동차로도 이 작업을 수행할 수 있습니다.

유산 계획의 요점은 귀하의 미성년 자녀, 귀하의 돈 및 귀하의 물건이 최소한의 번거로움, 비용 및 세금 납부와 최대 속도 및 개인 정보 보호를 통해 귀하가 원하는 사람이나 조직에 전달되도록 하는 것입니다. 위에 논의된 문서를 구현하면 일반적으로 적절한 후견인 자격과 자산의 적절한 상속이 보장됩니다. 그러나 가능한 한 검인을 피하고 세금을 적게 납부하는 것이 좋습니다. 다음에는 이 두 가지 주제에 대해 논의하겠습니다.

검인은 비용이 많이 들고 대중에게 공개되며 시간이 많이 걸릴 수 있습니다. 수만 달러의 비용이 들 수도 있고, 상속인은 1년 이상 혜택을 받지 못할 수도 있습니다. 지금 약간의 계획을 세우면 나중에 많은 번거로움을 줄일 수 있습니다. 검인은 주법이 적용되는 주별 프로세스이므로 주마다 다를 수 있습니다. 그러나 일반적으로 검인을 피하는 방법은 여러 가지가 있으며 그 중 일부는 이미 위에서 논의되었습니다. 여기에는 다음이 포함됩니다:

퇴직 계좌, 연금, 연금 및 생명 보험 상품에 적합합니다.

때로는 검인을 받는 것이 번거로움과 비용을 들여 검인을 피하는 것보다 낫지만, 일반적으로 유산 계획의 한 가지 목표는 검인을 피하는 것입니다. 이를 수행하는 방법에는 여러 가지가 있습니다. 주요 사항 중 하나는 퇴직 계좌의 수혜자를 지정하는 것입니다. 예를 들어, IRA의 수혜자가 귀하의 아들인 경우, 귀하의 사망 시 그는 검인을 거치지 않고 수익금을 받습니다(물론 이들에게는 상속세 및 상속세가 부과되며, 전통적인 IRA인 경우 최종적으로 소득세가 부과됩니다).

기억하시겠지만, 401(k) 또는 IRA를 개설할 때 수혜자를 지정하라는 요청을 받았습니다. 배우자 이외의 사람을 선택하는 경우 배우자의 서면 승인이 필요합니다. 이혼했거나 수혜자와 멀어지거나 마음이 바뀌었다면 돌아가서 수혜자를 계좌로 변경하는 것을 잊지 마십시오. 쓰라린 이혼 후 전 배우자가 고인이 고의로 그들에게 남기지 않았을 은퇴 계좌를 갖게 되는 경우가 종종 있습니다.

공동 재산 주(애리조나, 캘리포니아, 아이다호, 루이지애나, 뉴멕시코, 네바다, 텍사스, 워싱턴, 위스콘신, 때로는 알래스카)에 거주하는 경우 은퇴 계좌 자금의 절반 이상을 배우자 이외의 사람에게 양도할 수 없다는 점에 유의하십시오. 계좌의 절반은 배우자의 소유로 간주되기 때문입니다.

생명 보험금은 검인 기간 외에 수혜자에게 전달됩니다. 이는 일반적으로 귀하가 사망한 후 상속인이 돈을 받을 수 있는 가장 빠른 방법 중 하나입니다. 보험회사는 사망진단서를 받은 후 일주일 이내에 돈을 지급할 수도 있지만, 사망 후 2개월이 채 안 되는 경우가 거의 대부분입니다.

일부 주에서는 은행 계좌, 투자 계좌, 심지어 자동차에도 적합합니다.

신탁이 자산을 소유하게 하면 더 이상 검인을 거치지 않습니다. 이는 집, 자동차, 보트, 비행기, 전동 장난감, 은행 계좌, 심지어 투자 계좌를 위한 훌륭한 솔루션입니다.

사후 취소가능 신탁과 동일하게 작동하지만 사망 전에는 몇 가지 추가적인 제한 사항과 이점이 있습니다.

공동 소유와 같은 일부 형태의 공동 소유권은 검인을 피합니다. 예를 들어, 부동산 소유권이 적절하게 지정되면 해당 부동산을 소유한 사람은 검인을 거치지 않고도 전체 부동산을 자신의 이름으로 쉽게 이전할 수 있습니다.

이것을 유산 계획 도구로 사용하는 데는 주의가 필요합니다. 예를 들어, 귀하의 자녀를 공동 소유자로 귀하의 은행 계좌에 추가하는 데에는 몇 가지 문제가 있습니다:

자산의 소유권을 지정하는 방식에 따라 차이가 있을 수 있으므로 부동산, 자동차 등의 자산에 소유권을 부여할 때 프로세스에 상속 계획이 영향을 미친다는 점을 인식하세요.

공동 재산 주에서는 공동 재산이 검인을 거치는 경우도 있고 그렇지 않은 경우도 있습니다. 해당 주(애리조나, 네바다, 텍사스, 위스콘신)에서는 자산이 검인을 거치지 않도록 '생존자 권리 있음'이라는 문구를 추가할 수 있습니다.

투자나 집과 같은 자산과 같이 가치가 높은 자산의 공동 소유에 관해서는 추가적인 소득세 문제가 있습니다. 귀하가 사망하면 상속인은 일반적으로 귀하가 사망한 날의 자산 가치를 기준으로 한 단계 상승합니다. 그러나 상속인이 공동소유자인 경우에는 기본적으로 승격을 얻지 못합니다. 이는 해당 자산이 결국 매각될 때 잠재적으로 매우 크지만 완전히 불필요한 소득세 청구서를 초래할 수 있습니다. 따라서 일반적으로 은행 계좌 및 자동차의 상속인과 공동 소유권을 갖는 것은 괜찮을 수 있지만 투자 또는 주택에 대한 공동 소유권을 갖는 것은 거의 좋은 생각이 아닙니다.

때로는 유산의 가치가 특정 금액보다 낮을 경우 상속인이 상속받는 재산이 유언장에 명시되어 있다는 진술서를 작성하게 함으로써 검인을 피할 수 있습니다. 대부분의 의사 재산은 사망 시 이 한도를 초과합니다.

검인을 피하는 것 외에도 유산 계획은 증여세, 상속세 및 “사망세”라고도 불리는 유산세를 피하는 데 중점을 둡니다. 고인, 유산, 상속인이 납부하는 소득세를 최소화하는 것도 공통 목표입니다.

불행하게도 유산세법은 움직이는 표적이 될 수 있습니다. 그들은 지난 10년 동안 6번이나 변경되어 유산 계획 변호사에게는 좋은 수입을 보장하고 모든 사람에게는 많은 혼란을 안겨주었습니다. 2024년 현재 개인의 경우 유산세가 적용되기 전 연방 면제 금액은 1,361만 달러입니다. [최신 수치를 확인하려면 연간 수치 페이지를 방문하세요.] . 사망 시 귀하의 유산 총 가치가 해당 금액보다 낮으면 연방 유산세를 납부하지 않아도 됩니다. [2024] 결혼한 경우 면제 금액은 두 배인 2,722만 달러로 늘어납니다. , 그리고 이 금액은 실제로 이동 가능합니다. 즉, 사망한 첫 번째 배우자의 모든 자산은 세금 납부 없이 두 번째 배우자에게 전달되며, 두 번째 배우자는 거의 2,800만 달러에 달하는 연방 유산을 면세로 전달할 수 있습니다. 면제 금액도 현행법에 따라 인플레이션에 연동되므로 20년마다 두 배로 늘어나야 합니다. 그러나 현행법에 따르면 의회가 이를 연장하지 않는 한 면제는 실제로 2026년 1월 1일에 절반으로 줄어들게 됩니다.

주에서는 또한 유산세 게임에 참여하기를 좋아하며, 더 나쁜 것은 일부 주에서는 연방 면제 금액을 사용하지 않는다는 것입니다. 여기에는 컬럼비아 특별구, 로드아일랜드, 코네티컷, 일리노이, 하와이, 버몬트, 오레곤, 메인, 워싱턴, 미네소타, 뉴욕, 메릴랜드, 매사추세츠가 포함됩니다. 예를 들어, 뉴욕에 거주하는 경우 2022년 주 세금 면제액은 611만 달러이며 최고 세율은 16%입니다. 각 주의 유산세 면제 및 세율은 여기에서 찾아보실 수 있습니다.

아이오와, 켄터키, 메릴랜드, 네브래스카, 뉴저지, 펜실베니아는 유산세보다는 상속세를 선호합니다. 이는 재산 자체가 아닌 상속을 받은 사람에게 세금이 부과된다는 의미입니다. 배우자는 일반적으로 면제되며, 일부 주에서는 직계비속도 면제됩니다. 해당 주에 상속세가 있는지 여기에서 확인할 수 있습니다.

유산계획을 세울 때 소득세도 영향을 받습니다. 귀하가 사망하기 전에 납부했는지, 사망한 해에 유산으로 납부했는지, 사망 후 상속인이 납부했는지 여부에 관계없이 모든 소득세를 고려해야 합니다. 또한 소득세 계획이 유산세에 미치는 영향을 고려해야 하며 그 반대의 경우도 마찬가지입니다.

가장 중요한 소득세 계획은 사망 시 기준 상향 조정을 중심으로 진행됩니다. 상속인은 귀하의 기반(즉, 귀하가 투자에 대해 지불한 금액)을 상속받지 않습니다. 귀하가 사망한 날 자산 가치가 한 단계 상승합니다. 따라서 귀하가 $100,000에 부동산을 구입했고 귀하가 사망할 때 그 자산의 가치가 $100만 달러였으며 상속인이 즉시 이를 판매한 경우에는 소득세가 부과되지 않습니다. 사망 시 기준을 상향 조정하지 않으면 $900,000에 대한 세금을 납부해야 합니다! 일반적으로 노인, 특히 건강이 좋지 않은 사람이 기초가 낮은 물건을 팔아 소득세를 납부하는 것은 좋지 않습니다. 그 자산을 자녀에게 맡기는 것이 훨씬 더 나은 경우가 많습니다. 비록 그것이 그들이 그때까지 살기 위해 돈을 빌려야 한다는 것을 의미하더라도 말입니다. 사망 전에 자산을 매각해야 하는 경우 베이시스가 높은 자산을 우선적으로 매각해야 합니다.

소득세에 미치는 또 다른 중요한 영향은 배우자 중 한 명이 사망한 후 나머지 배우자가 한 사람으로서 일반적으로 더 높은 세율로 세금을 신고하게 된다는 사실입니다. 따라서 두 배우자가 모두 살아 있는 동안 일부 소득세를 미리 납부하는 것이 합리적일 수 있습니다.

대부분의 유산세 계획은 연방 및 주 유산세 면제를 최대한 활용하는 데 중점을 두고 있습니다. 이상적으로 좋은 계획을 세우면 유산세를 완전히 없앨 수 있지만, 유산이 매우 큰 경우에도 납부액을 최소화하는 데 도움이 될 수 있습니다.

대부분의 문서와 마찬가지로 귀하의 재산 가치가 유산세 면제 금액보다 낮을 경우, 유산세가 전혀 부과되지 않습니다. 돈을 쓰고 기부함으로써 부동산 가치를 낮추는 데 도움이 될 수 있습니다. 언제든지 자선 단체에 금액을 기부할 수 있으며, 그렇게 하면 소득세 혜택을 받을 수도 있습니다. 그러나 [2024] 개인별로 $18,000만 기부할 수 있습니다. 증여세법이 시행되기 전에 매년 다른 사람에게 나누어 줄 수 있습니다. 그 이상을 기부할 수 있지만 연간 $18,000를 초과하는 금액은 증여세 신고서를 제출해야 하며 유산세 면제를 받기 시작합니다. 일단 그것이 사라지면, 증여세를 납부하기 시작하는데, 이는 본질적으로 유산세를 미리 납부하는 것과 같습니다. 자녀에게 $18,000, 자녀의 배우자에게 $18,000를 줄 수 있으며, 귀하의 배우자도 똑같이 줄 수 있다는 점을 명심하세요. 따라서 증여세로 인한 번거로움 없이 두 분은 결혼한 자녀에게 매년 $68,000를 기부하실 수 있습니다.

자산의 가치가 높아질 가능성이 높으면 그렇게 되기 전에 먼저 기부하는 것이 좋습니다. 그렇게 하면 그 감사액 모두가 귀하의 재산으로 귀속되지 않고 재산세가 부과되지 않습니다. 이는 단순히 상속인에게 자산을 제공하는 방식으로 직접 수행할 수도 있고 취소 불가능한 신탁, FLP(Family Limited Partnership) 또는 FLLC(Family Limited Liability Company)를 사용하여 간접적으로 수행할 수도 있습니다.

또한 IRS는 귀하의 유산 규모를 평가할 때 세전 달러와 세후 달러를 동일하다고 간주하므로 Roth 전환을 통해 유산 규모를 줄일 수도 있습니다.

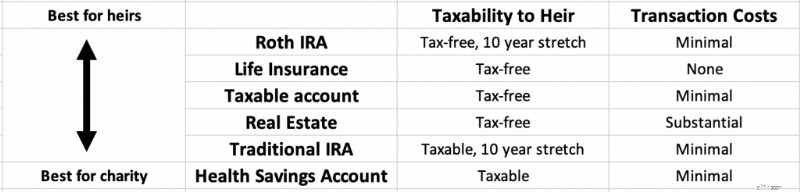

일반적으로 아래 목록의 상단에 있는 자산은 상속인에게 남기는 것이 가장 좋으며, 목록의 하단에 있는 자산은 자선단체에 남기는 것이 가장 좋습니다. 자선 단체에 아무것도 남길 계획이 없다면, 상속인이 받는 것을 최대화하려면 밑에서부터 위로 지출하는 것이 가장 좋습니다.

Roth 계정의 세금 혜택은 귀하의 사망 후 상속인에 의해 10년 더 연장될 수 있으며 일반적으로 상당한 자산 보호도 받습니다.

생명 보험 사망 후 몇 주 이내에 면세 현금으로 상속인에게 전달됩니다.

과세 대상 투자 사망 시 기준 상향 혜택을 받을 수 있으므로 사망 후 상속인이 면세 현금으로 신속하게 전환할 수 있습니다. 단, 판매와 관련된 비용이 발생할 수 있습니다.

기존 IRA 및 401(k) 상속인이 10년 동안 연장할 수 있으며 Roth IRA와 마찬가지로 자산 보호를 받을 수 있습니다. 이 금액은 여전히 세전 금액이며 모든 인출은 상속인에게 전액 과세 소득이 됩니다.

세전 자산인 경우 자선단체에 기부되면 자선단체가 전액을 가져가며 누구도 그 돈에 대해 세금을 내지 않습니다. 건강 저축 계좌(HSA)도 상속인이 늘릴 수 없으므로 세전 자금으로 자선 단체에 기부하는 것이 가장 좋습니다.

생명보험금에는 소득세가 부과되지 않습니다. 귀하가 사망 시 귀하의 아내, 자녀 또는 개에게 생명보험금 100만 달러를 남겨둔다면, 그들 중 누구도 그 중 1센트도 소득세로 납부하지 않을 것입니다. 따라서 생명 보험, 심지어 종신 보험과 같은 종신 생명 보험도 때로는 좋은 유산 계획 도구가 될 수 있습니다(그러나 좋은 투자 계획은 거의 아닙니다). 수익금은 유산세를 납부하거나 매각이 어려운 가족 소유 기업이나 농장에 유동성을 제공하는 데 사용될 수 있습니다. 그러나 사망자/재산이 보험 소유자인 경우 수익금에는 여전히 유산세가 부과됩니다.

이를 방지하는 유일한 방법은 누군가 또는 다른 사람이 정책을 소유하게 하는 것입니다. 자녀가 보험을 소유하게 하고 매년 보험료를 선물할 수도 있지만, 취소할 수 없는 신탁을 소유하게 하는 것이 훨씬 더 일반적입니다. 본질적으로 이 전략에는 증여세 금액(2023년 기준 1인당 연간 $18,000)보다 약간 적은 연간 보험료로 생명 보험 상품을 구매하는 것이 포함됩니다. 보험료 금액은 매년 취소불능 생전신탁에 적립되어 생명보험 구입에 사용됩니다. 사망 시 수익금은 소득세와 재산세가 면제되어 상속인에게 전달됩니다. 생명 보험 현금 가치/사망 혜택 증가에 대해서는 세금이 부과되지 않으므로 부를 전달하는 매우 세금 효율적인 방법입니다.

그러나 세금 절감 혜택이 생명 보험 "투자"의 추가 비용과 상대적으로 낮은 수익보다 큰지 판단하려면 심각한 수치 분석이 필요할 수 있습니다. 어차피 부동산에 유산세가 부과되지 않는 것은 아마도 좋은 생각이 아닐 것입니다. 보험 판매원은 기회가 있을 때마다 이러한 혜택을 강조할 것임을 기억하십시오. 정기 생명 보험은 여전히 거의 모든 사람들에게 최고의 보험입니다. 유산세 문제가 발생할 것으로 예상되는 경우 고려해야 할 사항이라는 점을 명심하세요. 구매를 기다리면 해당 연령에 보험에 가입하지 못할 위험이 높아지지만, 당시 보험에 가입할 수 없는 것으로 판명된 경우 사용할 수 있는 다른 유산 계획 도구가 있습니다.

유산 계획을 준비할 때 수행해야 할 몇 가지 구체적인 단계가 있습니다.

재정 계획과 마찬가지로 첫 번째 단계는 자신의 현재 위치와 가장 원하는 것이 무엇인지 파악하는 것입니다.

귀하의 순자산은 아마도 개인 금융에서 알아야 할 가장 중요한 숫자일 것입니다. 그러나 유산 계획에 있어서는 귀하에게 유산세 문제가 있는지 여부를 결정하는 요소입니다. 귀하의 순자산이 연방 및 해당 주 유산세 면제 금액보다 적으면 유산세가 부과되지 않습니다.

귀하의 순자산은 귀하가 소유한 모든 것에서 귀하가 빚진 모든 것을 뺀 금액입니다. 은행 계좌, 집, 은퇴 계좌, 중개 계좌, 업무 또는 기타 사업체의 가치, 임대 부동산 등 모든 자산을 합산하세요. 대부분의 경우 합리적인 추정이 적합합니다. 기술적으로 정확하려면 차량, 장난감, 가구, 의류, 가정용품도 합산해야 하지만, 실용적인 관점에서 보면 대부분의 사람들은 큰 물건만 포함합니다. 그런 다음 모든 부채 또는 부채를 합산하십시오. 여기에는 주택담보대출, 학자금 대출, 신용카드, 자동차 대출 및 기타 귀하가 갚아야 할 모든 것이 포함됩니다. 자산에서 부채를 빼면 순자산이 됩니다.

순자산을 계산할 때 모든 자산과 부채 목록을 작성하십시오. 이 문서는 귀하와 귀하의 변호사가 적절한 유산 계획을 세우는 데 도움이 될 것입니다. 포함:

인생에서는 물건이나 돈보다 사람이 더 중요합니다. 특히 당신에게 의존하는 미성년 자녀가 있는 경우에는 더욱 그렇습니다. 귀하가 갑작스럽게 사망할 경우를 대비하여 귀하의 계획을 나열하십시오. 포함:

부동산법은 주마다 다르므로 해당 주에 변호사가 필요합니다. 매우 기본적인 유산 계획은 온라인 변호사/서비스를 사용하여 스스로 할 수 있는 프로젝트일 수 있지만, 이 사이트를 읽는 대부분의 전문가는 결국 실제 변호사와 마주 앉아 이 작업을 수행하기를 원할 것입니다. 이 변호사는 귀하가 프로세스를 이해하고, 문서 초안을 작성하고, 질문에 답변하고, 필요에 따라 정기적으로 계획을 업데이트하는 데 도움을 줍니다. 또한 귀하의 사망 후 상속인을 위한 수탁자 및 자원 역할을 할 수도 있습니다.

수십 개의 온라인 법률 서비스가 있습니다. 가장 잘 알려진 것은 Legal Zoom이지만 Rocket Lawyer, LegalShield 및 Zen Business도 있습니다. Some specialize in business formation such as LLCs and corporations, but most will at least do a basic will and perhaps even a trust. They can probably handle a basic “I love you” will that names a guardian and conservator for your children, but by the time you start thinking about trusts, it's probably time to find a local attorney.

Attorneys generally charge by the hour, perhaps $250-$350 per hour. So the cost of your estate planning depends on the complexity of your estate. If your situation is really complex, it will cost you thousands or even tens of thousands to form trusts, family-limited partnerships, and more. But a simple will or power of attorney may cost less than $200. The initial meeting is often free, so feel free to shop around a bit. It can help you keep costs down if you did your research, knew exactly what you want before you arrive, and collected all relevant information and documents. Plus, it'll help if you can make important decisions rapidly and are willing to participate fully in the process. No, the fees are not going to be tax-deductible, even if you own a business. They used to be deductible as an itemized deduction prior to the Tax Cuts and Jobs Act and may again be deductible when those provisions sunset after 2025.

Your goal is to find someone that is competent, experienced, and a good fit. You probably don't want your friend or cousin unless they specialize in estate planning. You can check to make sure they're in good standing with the bar and that estate planning is what they spend the majority of their time doing. Like with a financial advisor or a doctor, there is some value to a few gray hairs. Someone who has already done this hundreds of times is usually going to be more efficient and make fewer mistakes. You also want someone that you can relate to and enjoy working with. Ideally, they have worked with a lot of people in your particular situation. WCI keeps a shortlist of recommended attorneys for your estate planning and asset protection needs.

You have your documents and the ideas of what you want, and you have hired an attorney. Now, it is time to establish your directives and time to start producing documents.

The will lists a guardian and conservator for minor children. It may also list who is to receive various assets, including real property like your home that is not covered by beneficiary designations. These may be very simple “I love you” wills if you are recently married with young children to incredibly complex legal instruments when there are blended families with married adult children and minor children involved.

In some states, a “holographic will” is actually valid and requires very little formalities. However, to make sure the will is valid and not contested, it is best to sign it in a formal way, including each of these steps.

A will typically names the executor of the will. Sometimes it is simply a trusted family member, especially if there is an attorney in the family. It can also be your estate planning attorney if you prefer to minimize family drama. This person will be responsible for wrapping up your affairs, including selling property and filing tax returns, as well as carrying out the instructions in your will. Named executors are simply acting in your stead, of course, and have no responsibility for or ownership of your debts or assets.

An important part of estate planning is also to go over every account or policy that can name beneficiaries and make sure the appropriate people or entities are named. You may wish to name a trust as the beneficiary. You can also usually name contingent beneficiaries if the beneficiary dies before you or refuses the gift. Beneficiaries are easily and routinely named for retirement accounts, annuities, and life insurance policies. But you also need to think about Health Savings Accounts, 529s, and ABLE accounts. Taxable investing accounts and bank accounts can also be set up to go to a beneficiary at the time of your death with a “Payable on Death” or “Transfer on Death” designation. In some states, you can even do this with houses and cars. This is faster, cheaper, and more private than simply naming beneficiaries for each of these in your will and having the executor take it through probate.

If you want some control over your healthcare decisions after you get too sick to make your own decisions, you probably want to get a living will and name a healthcare proxy. This can even be a formal healthcare power of attorney. You may want to provide a specific HIPAA waiver for your proxy. Perhaps you want to fill out your state's formal Do Not Resuscitate (DNR) form. Whether it's in the will or not, provide as much direction as you wish to your proxy including what you would want in a given situation. I find that most people are fine with an attempted resuscitation or a short period of life support; they just don't want to “be a vegetable” who is “living on a machine the rest of their life.” Consider including specific instructions about CPR, dialysis, intubation/ventilation, pressors, nutrition support (tube feeds), ECMO, and surgery.

A revocable or living trust is very useful if you wish to pass on assets faster, with less expense, with more privacy, and with more control to your heirs. Most white coat investors will want to put one in place as part of their estate planning process and this is likely a large part of the work and cost of the attorney.

A trust is a separate legal entity—like an individual, a corporation, or a limited liability company—and lives on after your death according to its provisions. To pass an asset on to heirs through a trust, the asset must be titled in the name of the trust. With a revocable or “living” trust, you can simply remove the asset from the trust at any time while you're alive. Thus, it passes assets outside of probate but provides no asset protection. With an irrevocable trust, you are giving away the asset. You lose a lot of control that way, but you gain two things:

An irrevocable trust does have to file a tax return, however, and it is subject to a more aggressive set of tax brackets. This is why a lot of people put whole life insurance policies inside irrevocable trusts since they do not generate taxable income.

A testamentary trust is created at the time of your death. While this avoids the hassle and expense of maintaining a trust during your life, the assets must go through probate before going into the trust.

Charitable trusts can also be created at this point in the estate planning process. These can save a lot of taxes, but generally do require significant charitable intent to work out well.

Remember to actually retitle assets in the name of the trust, or you will spend all that money on a trust for nothing.

This discusses your funeral, burial, and other final wishes. You may also wish to include messages for family or friends. Obviously, you don't need an attorney to do this part, but be sure to include it with your other papers and tell people it exists, or they might not look at it until it is too late. This may be a good place to include the master password for your password manager and directions for what to do with social media accounts, email accounts, Google Drive, and other assets in the cloud.

This is also a good time to give some thought as to what you will do with your businesses. These might be a practice, side gig, or full-on free-standing business with multiple employees. Just like people need estate planning, so does your business. What will happen if you die? What do you want to happen? Make sure the business has a plan in place. Forming a business as a Family Limited Partnership (FLP) or Family Limited Liability Company (FLLC) can save a lot of taxes and provide asset protection, and it can facilitate a smooth, private transition at the time of your death.

As your trusts and other documents and plans are being created, this is a good time to consider the estate tax, income tax, and asset protection implications of your plans.

Estate tax is tax that is paid on any amount over the estate tax exemption. It is often called the “death tax.” The idea behind it is to try to prevent a class society from forming as rich people pass wealth to their kids' generation after generation. The federal estate tax brackets rapidly rise to 40%, meaning 40% of what you leave behind goes to the government and 60% to your heirs. Any money left to charity is not subject to that tax. However, the tax does not begin until your estate is larger than the estate tax exemption. On a federal tax level, that exemption is $13.61 million ($27.22 million married) in 2023, but some states have their own estate tax with a significantly lower exemption amount. Under current law, the married exemption is “portable,” meaning that just because you were married, you get the $27 million exemption at the time of your death. Essentially, if you die, your spouse can inherit everything from you without using up any exemption AND they get to use your exemption when they die.

Unlike the estate tax, which is paid by the estate (essentially the deceased), some states (Iowa, Kentucky, Maryland, Nebraska, New Jersey, and Pennsylvania) have an inheritance tax instead of an estate tax or in addition to an estate tax. This tax is assessed to the person inheriting assets. It is entirely possible for an asset to be subject to an estate tax in one state where the person died AND be subject to an inheritance tax in another state where the inheritor lived!

The gift tax is rarely paid and is best thought of as part of the estate tax. Basically, if you give anyone more than $18,000 [2024] in a year, the amount above $18,000 is subtracted from the estate tax exemption amount. Once that exemption amount is completely gone, gift taxes must be paid. Until it is gone, you are merely required to file a gift tax return, not pay any actual tax. The gift tax prevents people from giving everything away on their death bed so that it isn't subject to estate taxes.

The main way to avoid estate taxes is to minimize the size of the taxable estate above the exemption amount. There are many ways to do this including:

The last two methods use up less of the estate tax exemption than you might think, because the value of the gift is reduced. That's due to the fact that the inheritor will not receive them for some time or because the asset is illiquid.

It is also a good idea to think about how you are going to reduce income taxes for yourself and your heirs. If you plan to split your estate between heirs and charity (or even just heirs in very different tax brackets), carefully decide which assets go where, as per the chart earlier in this post. You also want to take full advantage of the step-up in basis at death. It is often better to borrow against low basis assets rather than sell them and realize even long-term capital gains in the last years of life.

When forming businesses or doing estate planning, there are numerous asset protection implications. It can make sense to combine asset protection and estate planning into one process. Retirement accounts, whole life insurance, irrevocable trusts, family limited partnerships, and family limited liability companies can all have strong asset protection benefits. When forming trusts, be sure to consider the implications of the trust on your children and other heirs. Written properly, you can ensure the assets of the trust only benefit your heir and not their spouse or ex-spouse.

Now that your estate plan is in place, you need to do a few things to maintain it.

Estate plans should be reviewed for an update in three circumstances:

Sometimes, simple addendums can be added to documents or you may need to completely redraft the documents and entities you previously formed.

Beneficiaries may also need to be changed, and additional assets may need to be placed into the name of the trust.

You should have multiple copies of your estate planning documents. You should keep an easily accessible copy of everything at home in one place. Clearly label it so it can be found and tell those who need to know about it where it is. An electronic copy is also a good idea, and you may even want an additional physical copy elsewhere. Your attorney will also likely keep a copy of it. You may also want to provide a copy to the executor of the will, the conservator of your children, the trustee of your trusts, and even major heirs.

As a general rule, your estate planning documents are not a great place to keep secrets. It is far easier for your heirs to plan their own financial lives when they know what is coming. You may also wish to keep a file of your living will, healthcare proxy, and/or healthcare power of attorney at your local hospital and physician's office. Remember if no one can find your documents, it is as though they do not exist. What a shame to put all of that time, effort, and money into the process for nothing. Dying intestate (i.e. without a will) means you have chosen your state's designated estate plan instead of your own.

The first thing that may be needed after you die is that letter of intent that outlines your funeral wishes. The rest of the process probably won't even start until after that occurs. Once the dust settles from that, the executor of your will goes to work, and the probate process begins.

Probate law is state-specific, but you usually need an estate of a certain size before it must go through a full probate. Remember, your entire net worth does not contribute to the size of your estate for probate purposes, only the size of the estate that goes through probate. In my state of Utah, an estate must go through probate if:

So if you have your home, cars, boats, bank accounts, and taxable investing accounts owned by a revocable trust and have beneficiaries named for all retirement accounts and life insurance policies, you could potentially avoid this process altogether.

First, the last will and testament is authenticated and the executor/administrator/personal representative is appointed. Then this person must do the following tasks:

While state-specific, this bond is often required and is likely to cost at least a few hundred dollars and possibly thousands. If someone comes to the court and says the executor is not fulfilling their duties, the court can investigate and, if applicable, force them to do so because of this bond.

Hopefully, you've made this easy on your executor.

Appraisals may be required for some assets, but most of the time, this is just getting bank and brokerage statements. If you're still living at home at the time of your death, the executor may hire an estate sale company to determine a value for all the stuff left in your house.

A great benefit of living a debt-free life, at least by the end, is your executor has one less task to do. Remember your debts have to be paid off before anyone gets an inheritance, at least an inheritance of the assets that go through probate. Bypassing assets outside of probate, you can potentially stiff a creditor while still providing an inheritance.

An income tax return must still be filed in the year of your death (if you left a spouse, they can still file Married Filing Jointly one more time). The executor will also be responsible to make sure an income tax return for the estate is filed. An estate is technically a different entity than the person who died and needs its own tax number and its own special return (IRS Form 1041). It must file its own return if any beneficiary is a non-resident or if the estate made $600 or more. An estate tax return (IRS Form 706) must be filed if the estate is over the exemption amount OR if any of the exemption is being transferred to the spouse. The executor may also need to ensure state income and estate tax returns are filed.

Finally, the executor is responsible for actually distributing the estate. It would be a very bad idea to make any distributions before all creditors and taxes have been paid, and thus, you can see why it takes a long time for heirs to get their inheritance when it has to go through probate.

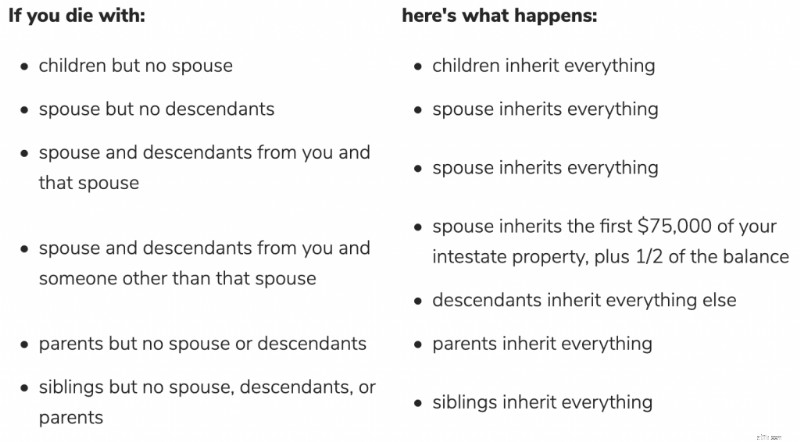

If you do not have a will appointing an executor, the state will appoint one. The usual first choice is your spouse or domestic partner, then your children, then any other available family. The executor must follow the state's intestate succession laws. These laws generally pass assets preferentially to a surviving spouse and children, not unmarried partners, friends, or charities. These laws can be complex if your family situation is complex, but it's very simple in a simple situation. For example, if you were only married once and only had children with that person, all of your assets go to your spouse if the spouse is alive and to the kids if the spouse is not alive. Otherwise, it gets very interesting. Per Nolo, this is what happens in my home state of Utah:

Intestate laws in other states are generally similar, but they all vary somewhat, especially as treating domestic partners. If you do not like your state laws, that is a very good reason to get a will in place ASAP.

The trustee of your trust(s) has a fiduciary responsibility to carry out the instructions in the trust, whatever they may be. There are almost limitless options for passing assets to your heirs via a trust. There can be restrictions based on age, knowledge, religion, marital situation, educational achievements, or almost anything else you can think of. Some trust fund kids have it easier than others!

I hope this is helpful in outlining the general strategies of estate planning. There are lots of other tricks and tips involving trusts that I'll discuss in future posts. Remember that having a will, naming beneficiaries properly, and titling assets properly is cheap and probably all that most of us will ever need. If you need more than that, a few thousand dollars spent on an estate planning attorney will be well worth your time and effort. Also remember that the laws governing this process are state-specific and frequently change, so personalized, up-to-date advice is warranted in this important area. Anytime you get wind that Congress or your state legislature has changed the laws regarding probate or regarding estate taxes, you ought to consider whether to visit with your estate planning attorney again.

Have more questions about estate planning or protecting your assets? WCI 심사를 받은 전문가를 고용하여 문제를 해결하는 데 도움을 받으세요.

What have you done as far as estate planning? Do you have a will? A trust? Have you at least checked to make sure your designated beneficiaries were right?

[This updated post was originally published in 2011.]